Perseverance and Hard Workd Pays Off

JHDP VALUATION BY USING DCF wacc METHOD (1. Find out FCF 2. Find out NPV)

- Introduction

- This article aims to find the annual FCF using IRR, then to find out the NPV using the WACC as the discount rate.

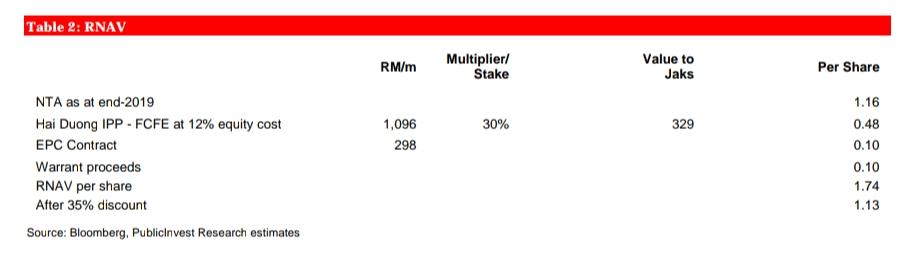

- A total of 5 research report were gone through (refer Table 1 & Table 2). Almost all power plants were valued using DCF, SOP method. The research report issued by PBB on 28-02-2020 is the only exception which employed RNAV method to value JHDP. The TP derived is RM1.13. The PBB’s report (28-02-2020) valued the plant at RM1096mil, whereas the total investment is RM8bil. RNAV will take out liabilities of RM6bil borrowing. Equity capital injection is RM2bil.

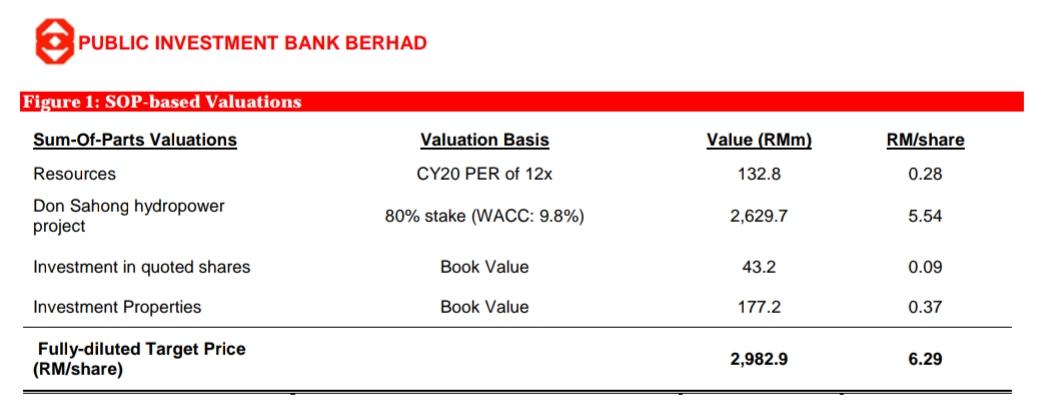

- In this article, I will employ DCF, SOP method to calculate the Fair Value for JHDP, instead of RNAV. (Note : In my opinion, PBB should standardize its valuation method on power plant business, unlike current scenario : JAKS – RNAV, MFCB – DCF, SOP ). I will model after PBB’s research report (Table 1, item 2) on MFCB Don Sahong power plant where DCF wacc 9.8% was used.

-

The step of calculation is

- Calculate CF using the IRR rate

- When CF is obtained, calculate the NPV using wacc as the discount rate.

|

Table 1: Valuation Method used by IBs to evaluate Power Plant |

||||||

|

No |

Power Plant |

IB |

Method |

Report Date |

Target Price |

Research Report Link |

|

1 |

MFCB Don Sahong |

MBB |

SOP DCF |

26-02-2020 |

6.10 |

http://www.bursamarketplace.com/mkt/tools/research/ch=research&pg=research&ac=953454&bb=970244 |

|

2 |

MFCB Don Sahong |

PBB |

SOP DCF wacc |

03-04-2020 |

6.29 |

http://www.bursamarketplace.com/mkt/tools/research/ch=research&pg=research&ac=984869&bb=1002184 |

|

3 |

JHDP |

PBB |

RNAV |

28-02-2020 |

1.13 |

http://www.bursamarketplace.com/mkt/tools/research/ch=research&pg=research&ac=956553&bb=973383 |

|

4 |

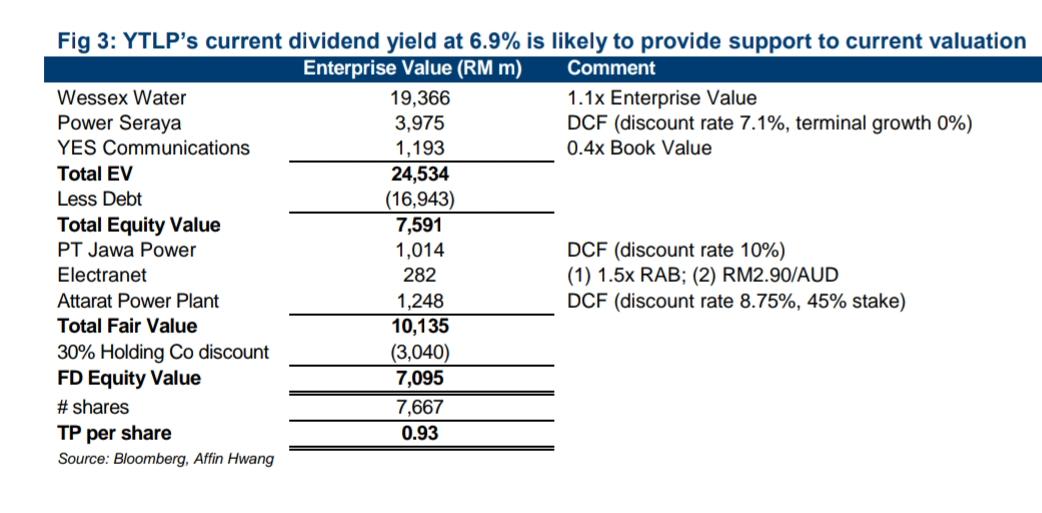

YTL Power |

Affin Hwang |

SOP DCF |

20-02-2020 |

0.93 |

http://www.bursamarketplace.com/mkt/tools/research/ch=research&pg=research&ac=946636&bb=963327 |

|

5 |

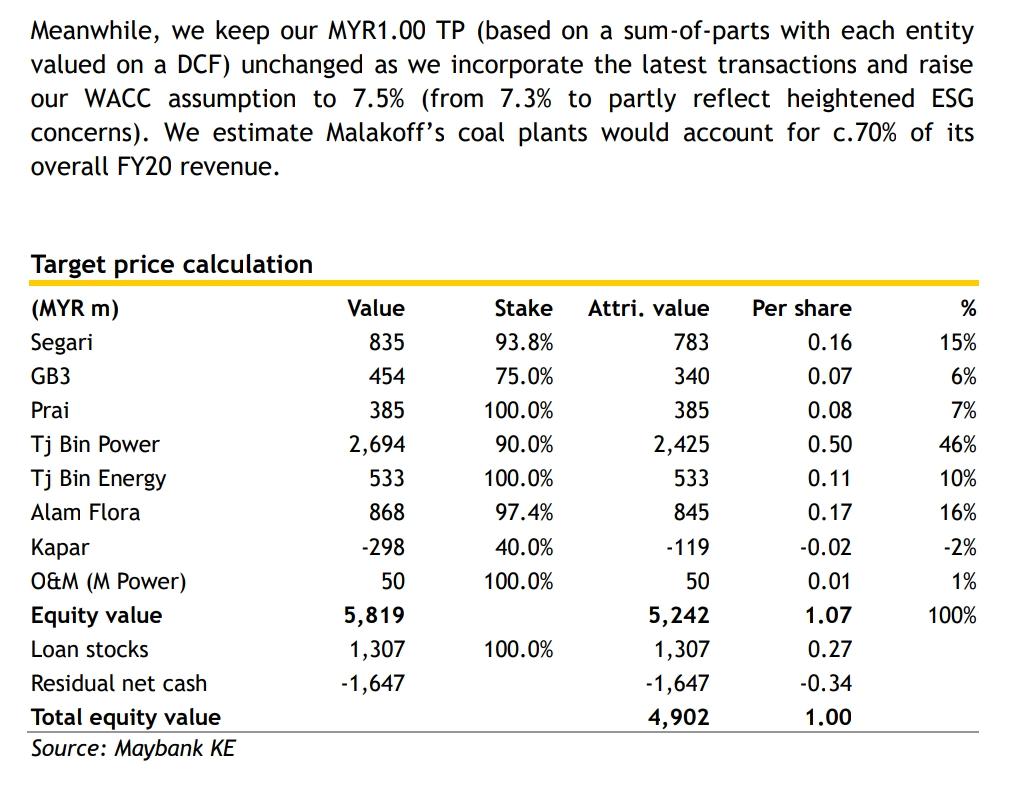

Malakoff |

MBB |

SOP DCF wacc |

05-02-2020 |

1.00 |

http://www.bursamarketplace.com/mkt/tools/research/ch=research&pg=research&ac=942933&bb=959608 |

|

Table 2: Summary of Power Plant Valuation |

|

|

1 |

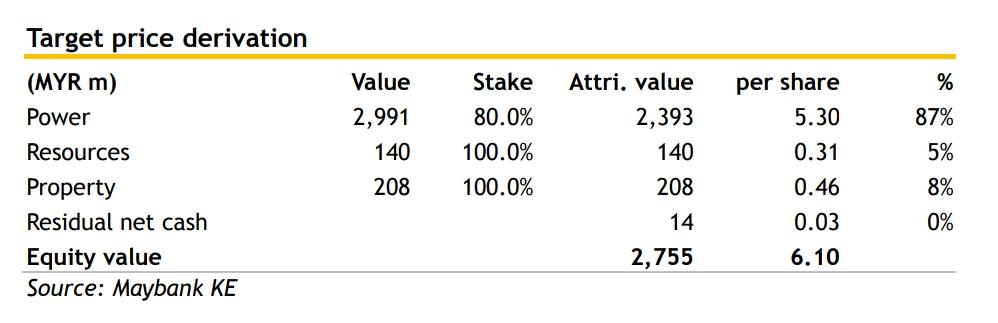

MFCB, SOP method, TP 6.10 By MBB (26-02-2020)

|

|

2 |

MFCB, DCF (wacc), SOP method, TP 6.29 By PBB (03-04-2020)

|

|

3 |

JHDP, RNAV method, TP 1.13 PBB (228-02-2020)

|

|

4 |

YTLP, DCF, SOP method, TP 0.93 By Affin Hwang (20-02-2020)

|

|

5 |

Malakoff, DCF (wacc), SOP method, TP 1.00 By MBB (05-02-2020)

|

- To Determine JAKS 30% Stake using DCF wacc 9%

PBB report (MFCB) dated 03-04-2020 is modeled after to derive JHDP’S valuation using DCF method. This aims to find out the different valuation between RNAV (PBB 28-02-2020) and DCF, SOP.

For simplicity, USD is pegged at 4.20 vs RM.

|

No |

MFCB valuation model PBB research report 03-04-2020 |

JHDP VALUATION DERIVED USING DCF METHOD |

|

1 |

To calculate Cash Flow using DCF method (IRR 17% & 12% respectively) Formula : DCF = CF1/(1+r)^1 + CF2/(1+r)^2 + ...+CFn/(1+r)^n

|

|

|

IRR RATE = 17% (note D),25year BOT ,total investment = USD 401m,USD 1 : RM 4.20

0 = -401+ CF/(1+0.17)^1 + CF/(1+0.17)^2 + ...+CF/(1+0.17)^25

CF(1.17^24+1.17^23+…+1)/(1.17^25) = 401

CF = 401 x (1.17^25) / (1.17^24+1.17^23+…+1) =401 x 50.6578255 / 292.1048559 = USD 69.54m = RM 292.07m

|

IRR RATE = 12% ,25year BOT , total invest = USD 1870m,USD 1 : RM 4.20

0 = -1870+ CF/(1+0.12)^1 + CF/(1+0.12)^2 + ...+CF/(1+0.12)^25

CF(1.12^24+1.12^23+…+1)/(1.12^25) = 1870

CF = 1870 x (1.12^25) / (1.12^24+1.12^23+…+1) =1870 x 17.00006441 / 133.3338701 = USD 238.42m = RM 1001.36m

|

|

|

From CF obtained above, to calculate DCF’s NPV

|

||

|

2 |

WACC(refer PBB report and verified in note A) = 9.8%,25year BOT, CF(IRR 17% ) = RM292.07m

DCF = RM 292.07m /(1+0.098)^1 + RM 292.07m /(1+0.098)^2 + ...+ RM 292.07m/(1+0.098)^25

DCF = RM 292.07m x (1.098^24+1.098^23+…+1)/ (1.098^25)

DCF = RM 292.07m x 95.43689977 / 10.35281618

DCF = RM 2,692.43m (Don Sahong)

MFCB 80% = RM 2,153.94m Per share = RM4.55

|

WACC (refer note A)= 9.0%,25year BOT, CF(IRR 12% ) = RM1001.36m

DCF = RM 1,001.36m /(1+0.09)^1 + RM 1,001.36m /(1+0.09)^2 + ...+ RM 1,001.36m/(1+0.09)^25

DCF = RM 1,001.36m x (1.09^24+1.09^23+…+1)/ (1.09^25)

DCF = RM 1,001.36m x 84.7009 / 8.62308

DCF = RM 9,835.93 (HAI DUONG)

JAKS 30% = RM 2,950.77m

Per share = RM4.53

|

C: Conclusions and Comments

- For MFCB, by using IRR 17%, FCF obtained is rm292.07m. Subsequently using WACC 9.8% (as provided in PBB report), the DCF’s NPV is obtained. MFCB 80% stake = rm2153.94m. Fair Value for MFCB = RM4.55 (based on number of share 473mil).This figure is lower than what was written in PBB report (rm2629.7m FV = RM5.54) and MBB report (rm2393m, FV=RM5.30). This means my calculation is more conservative, not exaggerated.

- By modeling after MFCB, JHDP is calculated using IRR 12% to obtain FCF, thereafter using WACC 9% (refer note A) to calculate NPV. The valuation for JHDP 30% stake = rm2950.77m. The fair value per share = rm4.53. This figure is conservative and on the lower side (my calculation for MFCB proves that my valuation is more conservative).

- The above calculation proves the IRR rate of 12% is effective and verifiable.

Note A : HOW TO CALCULATE WACC

|

WACC = (E/V x Re) + ((D/V x Rd) x (1 – T)) |

|

|

MFCB

E = don sahong IPP EQUITY D = don sahong IPP DEBT V = total value of capital (equity plus debt) E/V = percentage of capital that is equity D/V = percentage of capital that is debt Re = cost of equity (required rate of return) Rd = cost of debt (yield to maturity on existing debt) T = tax rate

E/V = 0.625 D/V =0.375 Re = net profit/ mfcb’s total equity= 0.13 Rd = 0.06 T = 0.24

WACC = (0.625x 0.13) + (0.375x 0.06) x (1 –0.24)

WACC = 0.081+0.017 = 0.098 (This figure is in-line with PBB’s report)

|

JHDP

E = HAI DUONG IPP EQUITY D = HAI DUONG IPP DEBT V = total value of capital (equity plus debt) E/V = percentage of capital that is equity D/V = percentage of capital that is debt Re = cost of equity (required rate of return) Rd = cost of debt (yield to maturity on existing debt) T = tax rate JAKS’s total equity= RM920.4m Net profit (refer note B)

E/V = 0.25 D/V =0.75 Re = net profit/ JAKS’s total equity= 0.224 Rd = 0.06 T = 0.24

WACC = (0.25 x 0.224) + (0.75x 0.06) x (1 –0.24)

WACC = 0.056+0.034 = 0.09

|

Note B : How to calculate net profit

|

MFCB |

JHDP |

|

FCF = Net income + (non-cash expenses)- increasing in working capital - capital expenditure |

|

|

mfcb’s total equity= RM1711.88m

net profit= (CF - depreciation) =292.08m - (401m x 4.20 / 25year) =RM224.71m

|

Non cash expenses = total investment amortized over 25 years. Increasing in working capital =0 Capital expenditure = 0

RM 1,001.36 = Net income+ ( RM 7.85b / 25 years) - 0 -0

Net income = RM 1,001.36m - RM 314m

Net income from IPP = RM 687.36m

Jaks 30% profit = RM 206.21m

|

Note C: Definiton

Sum Of The Parts (SOTP)

Sum Of The Parts (SOTP) valuation is an approach to valuing a firm by separately assessing the value of each business segment or subsidiary and adding them up to get the total value of the firm. It can be used in conjunction with various valuation techniques such as Discounted Cash Flow (DCF) modeling and comparable company analysis.

RNAV

This method is conducted after each property projects’ market value has been determined. The RNAV method is more complex as it requires using the net asset value (NAV), deducting the liabilities to find the Revalued Net Asset Value of the real estate developer.

Weighted Average Cost of Capital – WACC?

The weighted average cost of capital (WACC) is a calculation of a firm's cost of capital in which each category of capital is proportionately weighted. All sources of capital, including common stock, preferred stock, bonds, and any other long-term debt, are included in a WACC calculation.

Note D : IRR 17% reference

The source of IRR Rate 17% for MFCB Don Sahong Plant

https://www.theedgemarkets.com/article/trade-wise-laos-hydropower-project-energise-mega-first%E2%80%99s-earnings-growth?from=singlemessage

P/S This article is co-authored by ehome009 and Shan Kee Tiow. I also wish to express my appreciation and gratitude to Mr DK66 for his valuable inputs and advise to perfectise the contents.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Perseverance and Hard Workd Pays Off

Discussions

11 people like this. Showing 12 of 12 comments

To calculate Cash Flow using DCF method (IRR 17% & 12% respectively)

Formula : DCF = CF1/(1+r)^1 + CF2/(1+r)^2 + ...+CFn/(1+r)^n

..................

ehome009, thanks for sharimg.

Is the above method used by MBB & PBB to determine MFCB's FCF?

Is that something standard?

Wouldnt it be more accurate using the expected outflow & inflow of cash as per the predicted timelines of the project? Meaning the 'timing' of these cash flows can differ greatly between MFCB and JHDP right?

2020-05-20 23:10

DCF = RM 9,835.93 (HAI DUONG)

JAKS 30% = RM 2,950.77m

............

The above DCF value is total asset value right?

If that is the case, wouldnt you need to offset the Debt (NPV) to get the Equity portion value first - before multiplying 30% stakes of JAKS on the Equity to obtain the share price?

2020-05-20 23:26

First, some IB report are posting in our report , all IB report about power plant company like Malakoff and ytl etc. When you to read all this IB report, you will discovered DCF and WACC. Why they must use DCF with WACC? The reason is inflation and power plant is a long run project for 25year. After 10 year, same money but value must less than today, so purpose of DCF method is consider Value preservation. The other reason is revaluation, when power plant run 5 year from cod, BOT just left 20 year life so calculate DCF just can count 20 year only, decrease value as the life of the power plant decreases.

2020-05-21 08:56

Probability

Wouldnt it be more accurate using the expected outflow & inflow of cash as per the predicted timelines of the project?

Don sahong IPP and Hai duong IPP can predicted well than Malaysia power plant, because of PPA. Laos and Vietnam government will guarantee purchase 80%- 100% power and give a stable coal price, Malaysia don’t have this guarantee.

Stable revenue and stable cost, so their most important work is confirmed power generation in predicted. This model is more easily predicted than other business, so they can predict IRR rate 12%.

2020-05-21 09:12

DCF valuations method not a total asset value, it is a power plant business value of NPV. Why use NPV? hai duong power plant’s present value worth RM4.53, so we can compare it’s value to share price.

FCF = Net income + (non-cash expenses)- increasing in working capital - capital expenditure

Probability, this is a FCF Method calculation of accounting, it is a mathematical. We want calculate net income , so we just adjust the method.

Net income = FCF - (non-cash expenses)+ increasing in working capital + capital expenditure

Why set 0 to increasing in working capital and capital expenditure? The reason is we don’t know how much of them, but we can confirm these two item will increase profit . 0 will not make higher profit was predicted, it will be safety in our calculation.

2020-05-21 09:32

If that is the case, wouldnt you need to offset the Debt (NPV) to get the Equity portion value first - before multiplying 30% stakes of JAKS on the Equity to obtain the share price?

It need for WACC, we want to find it for calculate DCF with WACC.

WACC = (E/V x Re) + ((D/V x Rd) x (1 – T))

E = IPP EQUITY

D = IPP DEBT

V = total value of capital (equity plus debt)

E/V = percentage of capital that is equity

D/V = percentage of capital that is debt

Re = cost of equity (required rate of return)

Rd = cost of debt (yield to maturity on existing debt)

T = tax rate

2020-05-21 09:35

Equity and Debt Components of WACC Formula

It's a common misconception that equity capital has no concrete cost that the company must pay after it has listed its shares on the exchange. In reality, there is a cost of equity.

The shareholders' expected rate of return is considered a cost from the company's perspective. That's because if the company fails to deliver this expected return, shareholders will simply sell off their shares, which will lead to a decrease in share price and the company’s overall valuation. The cost of equity is essentially the amount that a company must spend in order to maintain a share price that will keep its investors satisfied and invested.

2020-05-21 15:54

Thanks for the superb analysis. I believe the write has been all in Jaks. Let’s hope for the best

2020-05-24 09:59

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

The Alpha Trader

3

Rakuten Trade Research Reports

4

南洋行家论股

7

BFM Podcast

8

TA Sector Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

hng33

Very well written, clear with counter check and proven calculation.

2020-05-20 22:37