Icon8888 Gossips About Stocks

(Icon) Luxchem (2) - Two Consecutive Quarters of Super Profit

1. Introduction

I first wrote about Luxchem on 4 January 2015.

http://klse.i3investor.com/blogs/icon8888/67652.jsp

Just to recap, Luxchem is involved in manufacturing and trading of Unsaturated Polyester Resin("UPR"), synthetic rubber and other industrial chemicals.

The group's customers use its products to manufacture a wide variety of plastic products such as waterproof materials, bath tub, automotive components, table top, boats, etc.

|

Open

1.08

|

Previous Close

1.03

|

|

|

Day High

1.12

|

Day Low

1.08

|

|

|

52 Week High

04/14/15 - 1.31

|

52 Week Low

10/16/14 - 0.67

|

|

|

Market Cap

289.8M

|

Average Volume 10 Days

127.9K

|

|

|

EPS TTM

0.09

|

Shares Outstanding

263.5M

|

|

|

EX-Date

09/11/15

|

P/E TM

12.0x

|

|

|

Dividend

0.05

|

Dividend Yield

4.09

|

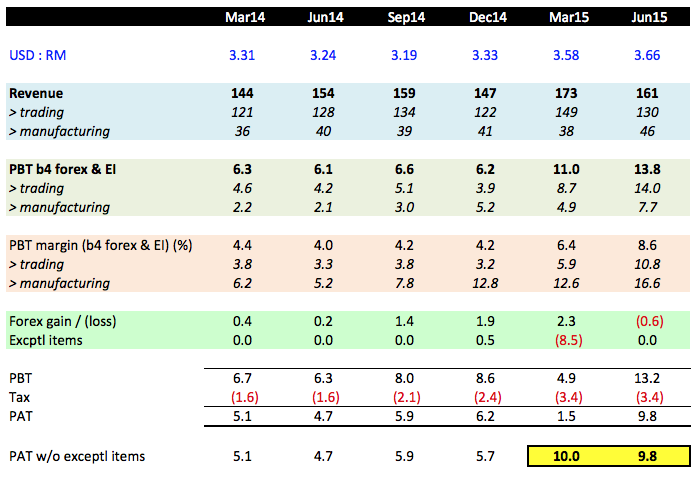

2. March 2015 Earnings Disappointing And Yet Exciting

At the beginning of 2015, I was very concerned about Malaysia's economic outlook and was only interested in export oriented companies. Since the bulk of Luxchem's products are sold in Malaysia, I was lukewarm about the stock in my January 2015 article.

However, contrary to my view, Luxchem share price rallied over the subsequent few months. Due to lack of analyst coverage and publicly available information, I was not sure what was the reason. But I am sure whoever chasing up the share price must have done his homework and discovered that Luxchem will do well in low oil price environment.

The rally didn't last long. Share price succumbed to consistent selling, retracing from RM1.30 all the way to around RM1.10.

We soon found out why the insiders were busy selling down. On 8 May 2015, Luxchem announced a very weak set of result. Net profit declined by closed to 75% from RM6.2 mil to RM1.5 mil. This shocked many investors and triggered another round of selling, causing share price to declined to RM1.00.

However, upon closer inspection, I found out that Luxchem has actually done very well in the March 2015 quarter. Its net profit was actually as high as RM10 mil, 61% higher than the RM6.2 mil in previous quarter. The reason its result was so weak was because of ESOS related expenses.

According to the company's explanation, during that quarter, they granted 32 mil ESOS to employees. The ESOS options were essentially Warrants, as it gives the holders the right to subscribe for new shares at a pre determined price. Based on Trinomial Option pricing model, each ESOS option has fair value of RM0.26. With 32 mil options given out, the total amount was RM8.5 mil.

It was this exceptional item that dragged down its Q1 2015 earnings.

In that quarter, the group actually saw improvement in operational parameters across the board. Not only turnover increased substantially, profit margin also experienced significant expansion, resulted in robust bottomline growth (please refer to table below).

I was excited about its performance but decided not to write about it. The main reason was because I was afraid that the strong result was due to stockpiling by customers ahead of GST and that future quarters might not be able to repeat the same performance.

3. Robust June 2015 Earnings

Yesterday, Luxchem reported excellent results for the quarter ended June 2015.

Despite slight dip in turnover, net profit came in at RM9.8 mil, tanslating into quarterly EPS of 3.75 sen. The strong earnings was achieved without any exceptional gain. As a matter of fact, there was a small forex loss of RM0.6 mil.

As usual, lack of information in the quarterly report made it difficult to explain how the sterling performnce was achieved. My guess is that they are related to lower raw material cost (low oil price) as well as strong US Dollars (which benefited the export segment).

If the group can sustain the recent two quarter's strong performance, we are potentially looking at net profit of RM40 mil for the full year, which translates into EPS of 15.2 sen based on 263 mil shares. At current price of RM1.10, prospective PER is 7.3 times.

4. Other Information

Luxchem has strong balance sheets. With net assets of RM171 mil, cash of RM87 mil and borrowings of RM61 mil, net cash is RM26 mil.

Together with the June 2015 results, the company declared dividend of 2 sen per share. In the past, they declare DPS of 6 to 8 sen per annum. This translates into dividend yield of at least 5.5%.

The group exports approximately 25% of its products.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

2 people like this. Showing 6 of 6 comments

Yes. I commented about the RM8.50 million on ESOS but later I totally forgotten about her. I would at least take a second look on her. I admire your sharpness.

2015-07-31 18:15

But I still couldn't understand the accounting book entries about this ESOS option. Would it involve cash/bank transactions? If it is a loss or expense (debit entry), where would have the corresponding credit entry gone to???

2015-07-31 18:24

Kenanga Research,

Nearly half of its earnings are derived from the defensive rubber glove industry, based on rubber and latex segments. As it is a one-stop centre, all the rubber glove makers are customers of LUXCHEM, which is able to supply a full range of additives and chemicals.

On the other hand, we see potential

of capacity expansion for its manufacturing segment by adding

additional reactor as and when demand arises while the capex for

expansion is relatively low as it invested only RM2.5m for the new

reactor. Moreover, profit margin for the manufacturing division is higher at 6%-10% at PAT level as opposed to 3%-6% for the trading segment, which could help to improve bottom-line. Based on current capacity, we project FY15E/FY16E earnings to grow at 30%/38% annually.

2016-01-09 22:03

Post a Comment

Featured Posts

Open a Moomoo Account Today and Win an Apple iPad Air*!

MQ Trading Signals

Time

Signal

Duration

Type

2024-05-03 16:50:00

ADX

5 Mins

BUY

2024-05-03 16:50:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-05-03 16:45:00

EMA 5

5 Mins

BUY

2024-05-03 16:30:00

EMA 5

30 Mins

BUY

2024-05-03 16:30:00

MACD/RSI

30 Mins

BUY

Apps

Top Articles

1

Nuclearinvestment

2

3

博傻理论

4

Good Articles to Share

5

6

THE INVESTMENT APPROACH OF CALVIN TAN

MKHOP (5139) What Is Its Current Forward P/E and Intrinsic Value, Calvin Tan

7

AmInvest Research Reports

STRATEGY - Local Institutional Support Drive Upward Momentum

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

giftformother

Thank you for this article and also thank you for Imaspro[I bought at 1.46 last week]

2015-07-31 15:22