Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

1. Introduction

Jaks is closed to completing the Hai Duong power plant. So far, two major pieces of information attracted my attention : (1) expected net profit of at least RM200 mil p.a. for its 30% stake, and (2) Internal Rate of Return of 12% (IRR).

Can these two pieces of information be reconciled ? To find out, I built an IRR model to test things out. To my surprise, they fit each other very well, without even needing me to massage the figures.

2. Internal Rate of Return

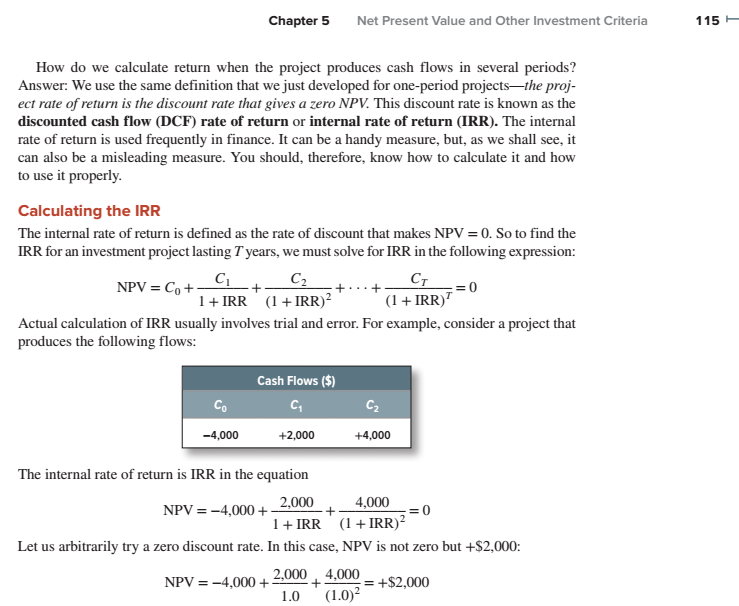

For those not familiar with IRR, please refer to the following :

![]()

Net Present Value is the sum of the discounted free cash flow of a project over its expected lifespan. In the equation, Co will be the negative cashflow to be incurred by Hai Duong during the construction period. Based on construction cost of RM7.5 bil (USD1.87 bil and exchange rate of 4) and construction period of 3 years, Co will be RM2.493 bil per annum (for 3 years). C1 will be the free cash flow of Hai Duong in first year of operation (positive) while C2 will be the free cash flow for year 2 (positive), and so on (until year 25).

IRR is the discount rate that will lead NPV to become ZERO (Note : Co is a negative number while C1 to 25 is positive, so at certain discount rate, it is possible to cause the equation to end up with value of Zero).

For more information, please buy this Kindle Book and flip to page 115.

3. Principal Assumptions

Based on publicly available information and input and exchange of ideas from many i3 forum members, we know of the following (roughly) :

(Capex)

Total capex for the power plant is USD1.87 bil. Based on USD : RM exchange rate of 4 to 1, that is equivalent to RM7.5 bil.

(Loan)

Assuming debt funding of 75%, total loan is RM5.6 bil.

Based on assumed interest rate of 5% (average) and repayment period of 15 years, the debt profile will look like this :

Key observations :

(a) based on 15 years repayment period, annual repayment is RM374 mil.

(b) in year 1, Hai Duang's interest payment is RM281 mil. However, as debt get progressively pared down, interest expenses also gradually decline. By year 15, it would have dropped to RM19 mil only.

The declining interest expense will of course have a positive impact on profitability.

(In real life, debt is likely to be repayed in tranches. But for discussion sake, we just stick to this simplistic straight line assumption and finetune later if necessary. My hunch is that the difference will not be material).

(Depreciation Charges)

Based on depreciation period of 22 years (25 years concession, 3 years construction, 22 years operation), annual depreciation charges is RM340 mil.

(Tax)

I was made to understand that the IPP is tax free for first 4 years, 5% for subsequent 9 years and 10% thereafter.

(Profit After Tax)

Many investors are expecting net profit of at least RM200 mil for Jaks' 30% stake in Hai Duong (ignore the anaylsts, they will start upgrading when Jaks share price goes to RM2.00).

Working backwards, Hai Duong's annual net profit would be RM667 mil (100% stake).

The PAT figure is not something plucked from the air. It is a consensus formed by investors after studying profitability figures of already completed Vietnam IPPs as well as projects in other countries such as MFCB and YTL Power in Laos and Jordan respectively.

I played with the IRR model by using PAT beginning from RM667 mil (translating into RM200 mil for 30% stake). It turns out that this level of profit will only generate IRR of approximately 8%. I gradually increase the profitability. Eventually at about RM1,060 mil, IRR becomes 12%. This translates into net profit of RM318 mil for Jaks' 30% stake.

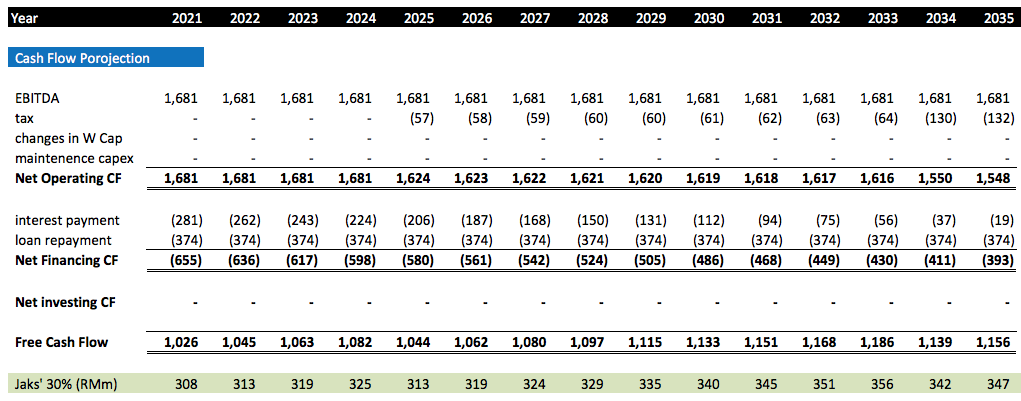

4. Cashflow Projection (and Profit as well)

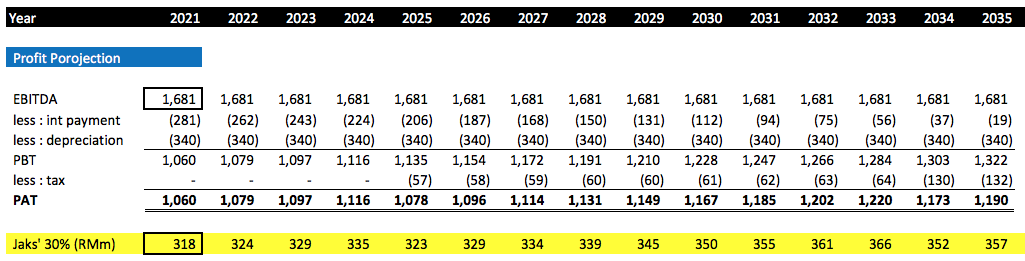

To derive the cashflow projection over next 22 years, we need to first figure out the EBITDA for year 1.

As mentioned in previous section, PAT and tax rate for year 1 is assumed to be RM1,060 mil and zero respectively. Hence, PBT is same as PAT (RM1,060 mil).

Meanwhile, interest expense and depreciation charges for year 1 is RM281 mil and RM340 mil respectivelty.

As such, EBITDA for year 1 = RM1,060 mil + RM281 mil + RM340 mil = RM1,681 mil (Reminder : this represents 100% equity interest)

How about year 2 onwards ? Well, since Hai Duong is an IPP backed by concession, EBITDA throughout the entire period should be more or less the same (in real life, inflation will have an impact, causing EBITDA to trend downwards at let's say, 3% per annum).

After factoring in all the above, the profit and cashflow projection will be as follows :

As shown in table above, Hai Duong's profit will be approximatelty RM1,060 mil per annum (translating into RM318 mil for Jaks' 30% stake). I am not interested in dwelling too much on the figures. The purpose of this article is to study the cashflow and IRR. As long as profit is approximately RM200 mil to RM300 mil for Jaks, I am happy already. So lets' just move on.

According to the table above, free cash flow is approximately RM1,000 mil per annum. This is not surprising. If profit is RM1,060 mil, the items that differentiate it from cashflow is depreciation charges and loan repayment. Since both figures are more or less the same (depreciaton charges is RM340 mil while loan repayment is RM374 mil), free cash flow will more or less be the same as net profit. (quick check !!)

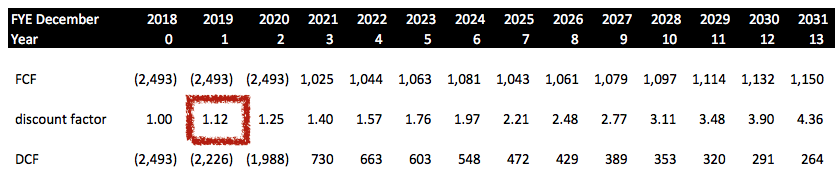

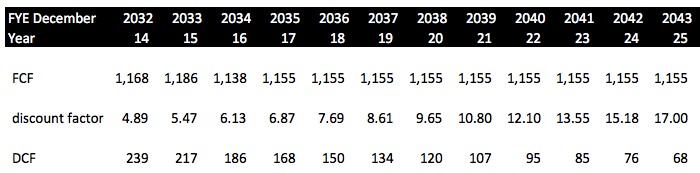

5. IRR

The IRR model is as follows :

![]()

As shown above, after investing RM7.5 bil over 3 years, to generate IRR of 12%, Hai Duong's free cash flow per annum must be approximately RM1 bil per annum.

This will translate into net profit of approximately RM1 bil per annum (as explained above, depreciation and loan repayment related figures offset each other). Based on 30% stake, Jaks' portion will be approximately RM300 mil per annum (to be precise, RM318 mil in FY2021).

6. Concluding Remarks

My financial modeling shows that Jaks' 30% stake can potentially deliver net profit of RM318 mil per annum when both units are operational in FY2021. This level of net profit is truly impressive. But is it too good to be true ?

Not necessarily.

There are two possible reasons why the profitability of Hai Duong can be so strong.

First of all, Jaks initiated the Hai Duong project back in 2008. Vietnam was badly affected by the Global Financial Crisis then (I can remember Gamuda was heavily sold down because it has property projects in Vietnam). To attract investors, Vietnam could have offered relatively attractive terms to balance out the perceived risk.

Secondly, the Ringgit has depreciated substantially in recent few years. When Jaks firmed up the concession agreement (in 2011 ?), the USD Ringgit exchange rate was 3.2. It has now declined to 4.2, a drop of 31%.

If you take RM318 mil and divide by 4.2, you will get USD75 mil. Based on exchange rate of 3.2 then, the profit attributable to Jaks' 30% is RM240 mil only (being USD75 mil x 3.2), a much lower level. The Vietnamese government was not as dumb and wasteful as it looked when come to awarding concession projects.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

18 people like this. Showing 50 of 56 comments

Dear Icon8888,

During the planning stage, the utilization hours used for planning purpose was 6,500.

After the plant is completed, the correct utilization hours used should be 7,238 (same as Vinh Tan 1 power plant). Hence IRR should be 15% instead of 12%.

7,238 utilization hours is confirmed by the management of Jaks to me after checking with CPECC engineers.

Please take note.

Thank you.

2020-05-01 14:37

On depreciation, there is no clear indication that reducing balance method of amortisation should be used. Straight line method is still most widely adopted

"The most appropriate method of amortisation of the intangible asset is usually the straight-line method, unless another method better reflects the pattern of consumption of the asset’s future economic benefits. However, in some circumstances, where the expected pattern of consumption of the expected economic benefi ts is based on usage, it may be appropriate to use an alternative method of amortisation." - IFRIC 12

In any case, the new international accounting standard will not allow power plant asset to be recognised as "concession asset" anymore. The asset shall be recorded as Loan receivables and repayment will more or less reflect a straight line pattern.

2020-05-01 14:44

Icon8888 is right to include interest expense as Project IRR is working on Net cash flow based on the planned debt equity structure.

2020-05-01 14:48

Is that the reason why Vinh Tan 1 can only generate profit after 18 years?

https://www.vir.com.vn/vinh-tan-1-gearing-up-for-operation-61958.html

When will the Vinh Tan 1 thermal power plant start generating profits?

Operating under the BOT format, the project boasts around $1.75 billion in total investment capital, 80 per cent of which is sourced from a consortium of several international banks. If the project runs smoothly without any hitches, Vinh Tan 1 Power Co., Ltd. will be able to pay off all debts and start generating profits 18 years after the plant starts commercial operation.

Posted by popo92 > May 1, 2020 2:25 PM | Report Abuse

icon8888 sifu, your assumptions on depreciation is very wrong. Depreciation costs are usually higher at first and decreasing year by year. suggest you may look for some info on IFRIC 12. Basically when factor in Depreciation & amortisation you will get a completely different figure, but i am not sure we can able to see them one day since jaks only have 30% minority stake in this power plant. Track record of integrity is not on the right side for jaks management.

2020-05-01 14:49

Thanks for your input, unfortunately I am not able to either agree to it or refute it as I have not seen this before

If you can provide me with the relevant theoretical reasoning (an article or pages of the textbook), then I will be able to make a better decision whether to revise the model

probability

11405 posts

Posted by probability > May 1, 2020 2:29 PM | Report Abuse

I think you should exclude the Interest deduction on your FCF used to show the IRR of 12%.

Project IRR is assuming the whole asset is funded without Debt - 100% equity.

....

Will go through in detail and find out why its not matching my derivation of about 140M profit/annum with 2 units operating.

2020-05-01 14:51

icon8888, the loan tenure should be 18 years which is maximum allowed by the vietnam government. This is why vinh tan 1 cited 18 years to fully pay off all debts.

2020-05-01 14:52

@DK66, i have seen many articles on the vietnam power plant IRR, they always exclude the Interest when calculating the project IRR which most say only 12%.

anyway, i am not from financial background to assert this.

http://infrastructure-projectfinance.blogspot.com/2013/11/project-irr-vs-equity-irr.html

Project IRR vs Equity IRR

The project IRR takes as its inflows the full amount(s) of money that are needed in the project. The outflows are the cash generated by the project. The IRR is the internal rate of return of these cash flows. The calculation assumes that no debt is used for the project.

Equity IRR assumes that you use debt for the project, so the inflows are the cash flows required minus any debt that was raised for the project. The outflows are cash flows from the project minus any interest and debt repayments. Hence, equity IRR is essentially the “leveraged” version of project IRR.

Generally Equity IRR is more than project IRR and the equity IRR will be lower than the project IRR whenever the cost of debt exceeds the project IRR.

Posted by DK66 > May 1, 2020 2:48 PM | Report Abuse

Icon8888 is right to include interest expense as Project IRR is working on Net cash flow based on the planned debt equity structure.

2020-05-01 14:54

Does a project have to fully repay borrowings before it can generate profit ?

I find the statement weird

————

probability : If the project runs smoothly without any hitches, Vinh Tan 1 Power Co., Ltd. will be able to pay off all debts and start generating profits 18 years after the plant starts commercial operation.

2020-05-01 14:55

DK66 sifu, this IFRIC 12 is actually introduced on 2008, but it doesn't adopted since lately years. So far i have not seen any BOT concession is still using straight-line method. Thank you for pointing out power plant asset cannot be recognised as concession asset under new international accounting standard. i didn't acknowledge that, could you send me any useful links for me to read? thank you

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

On depreciation, there is no clear indication that reducing balance method of amortisation should be used. Straight line method is still most widely adopted

"The most appropriate method of amortisation of the intangible asset is usually the straight-line method, unless another method better reflects the pattern of consumption of the asset’s future economic benefits. However, in some circumstances, where the expected pattern of consumption of the expected economic benefi ts is based on usage, it may be appropriate to use an alternative method of amortisation." - IFRIC 12

In any case, the new international accounting standard will not allow power plant asset to be recognised as "concession asset" anymore. The asset shall be recorded as Loan receivables and repayment will more or less reflect a straight line pattern.

2020-05-01 14:59

@DK66, its the Dividend distribution you are saying here right?

They can take that out from their huge depreciation / capital payment i suppose..

what certainty is there that it will be a continuous stream of dividend every quarter?

Mong Duong 2 did not even declare dividend last quarter.

If thats the case for JAKS - will that result as a zero income on a particular quarter where they did not receive cash distribution from Hai Duong power plant?

Posted by DK66 > May 1, 2020 2:57 PM | Report Abuse

Mong duong II and vinh Tan 1 reported profit immediately upon COD

2020-05-01 15:03

somebody mentioned recently (I forgot who) that upon COD, Hai Duong will “gradually scale up dependent on usage”

If I am not wrong, under Take or Pay concept, there is no “gradual scaling up dependent on usage”. From day 1, it is payment based on full capacity already Because they have made full capacity available to its client (Vietnam government)

That is why It is called capacity payment

2020-05-01 15:05

Project IRR always work on net cash flow basis in so far as the investment capital of the company is concerned. However, the equity portion of the capital shall not attract interest component as it represents shareholders' equity injection.

Project IRR return represents net return from the project and shall be used to weigh against risks for decision making. As borrowing costs represents part of the cost of investment, it is dangerous not to have considered the interest cost before making final investment decision.

2020-05-01 15:06

popo92, you may like to read this

Jaks Resources – Peer Comparison With Mong Duong II

https://klse.i3investor.com/blogs/Jaks%20resources/2019-04-29-story204451-Jaks_Resources_Peer_Comparison_With_Mong_Duong_II.jsp

-------------------------------

popo92 DK66 sifu, this IFRIC 12 is actually introduced on 2008, but it doesn't adopted since lately years. So far i have not seen any BOT concession is still using straight-line method. Thank you for pointing out power plant asset cannot be recognised as concession asset under new international accounting standard. i didn't acknowledge that, could you send me any useful links for me to read? thank you

2020-05-01 15:12

http://ecapslock.com/project-irr-vs-equity-irr/

Project IRR vs Equity IRR

..........................

By CA Amit Bansal | 19/11/201844 Comments

Internal Rate of Return (IRR) and Net Present Value (NPV) are the two methods which are widely accepted method throughout the industries for evaluation of any Long Term Projects.

Calculation of IRR is little tricky. In this post we will understand what is IRR, difference between project IRR and Equity IRR and whether Project IRR can be lesser than Equity IRR or not?

Internal Rate of Return (IRR)

.............................

Internal Rate of Return (IRR) is a rate on which NPV of the project equals to zero i.e. value arriving by discounting all the cash flows of the project with IRR rate will be zero.

Project IRR (PIRR) and Equity IRR (EIRR)

........................................

The project is generally financed in some proportion of Debt and Equity.

The project IRR gives the rate of return from the whole project. It is calculated presuming that there is no debt portion in the project financing. It calculates the rate of return considering the cash flows from the project only (i.e. except financing cost). Project IRR will remain same irrespective of capital mix of the project.

2020-05-01 15:13

Probabilty, I shall prove my point later. I m in the middle of my next article "Jaks Resources - The Most Reliable Earnings Guidance for JHDP"

2020-05-01 15:14

No issues DK66, look forward on that for my knowledge.

Below some reference related to LNG Thermal power plant using Project IRR less than 12% :

https://www.meti.go.jp/meti_lib/report/H29FY/000594.pdf

Posted by DK66 > May 1, 2020 3:14 PM | Report Abuse

Probabilty, I shall prove my point later. I m in the middle of my next article "Jaks Resources - The Most Reliable Earnings Guidance for JHDP"

2020-05-01 15:21

Meanwhile, icon8888 may like to take out the borrowing costs and determine the return. I m sure the return will look miserable and not feasible for investment.

2020-05-01 15:28

the return will be like what the management said to Public Bank IB of ~120M (profit) for 30% stake then

since the capital and interest payment is secured by EVN, its like a having a Bond level return perhaps...

just speculating

Posted by DK66 > May 1, 2020 3:28 PM | Report Abuse

Meanwhile, icon8888 may like to take out the borrowing costs and determine the return. I m sure the return will look miserable and not feasible for investment.

2020-05-01 15:34

Page 21 (summary 9)

https://www.meti.go.jp/meti_lib/report/H29FY/000594.pdf

You notice that the Presumptions used in calculation the IRR include allowance for borrowing costs.

2020-05-01 15:36

They are using the borrowing cost for establishing EIRR of 10% with PIRR of 7.1% compared against WACC of 6.4%.

PIRR is for comparing against WACC. If you include interest cost in PIRR than its meaningless to compare against WACC right?

Posted by DK66 > May 1, 2020 3:36 PM | Report Abuse

Page 21 (summary 9)

https://www.meti.go.jp/meti_lib/report/H29FY/000594.pdf

You notice that the Presumptions used in calculation the IRR include allowance for borrowing costs.

2020-05-01 15:47

https://www.vir.com.vn/vinh-tan-1-gearing-up-for-operation-61958.html

[ If the project runs smoothly without any hitches, Vinh Tan 1 Power Co., Ltd. will be able to pay off all debts and start generating profits 18 years after the plant starts commercial operation.]

my understanding is Vinh Tan 1 can generating profit for 18 years ( pay off all debt by 7 years ). not after 18 years. my goodness.

2020-05-01 15:56

not going to be such high figures if the assumption is IRR of 12% on equity , not on project cost...................

2020-05-01 15:59

The fact is they are including the interest cost for calculation to establish the desired IRR to compare against the hurdle rate of 10%

2020-05-01 16:22

I blow water only. Don't take this seriously. Just view from a melon eater.

To build the plant need capital mah. So say Year 1-3, -2.5b X 30%. But JAKS has been reported profits.

So, cost likely to be deducted after COD.

8 years break even about right lah, Andy said so.

https://www.theedgemarkets.com/article/jaks-eyes-break-even-vietnam-project-eight-years

Icon's calculation seems to be right if he is talking about Cashflow. But don't expect Net Income can be 300m because JAKS need to deduct back construction cost mah.

2020-05-01 16:22

Appreciate your work on the modeling.

I was wondering whether there will be maintenance capex incur throughout the period?

2020-05-01 17:19

@Icon8888

Great article.

Just to note: The exchange rate for USD/MYR may be too optimistic.

If I recalled correctly, in the last 60 years, MYR ever touch RM4 and above was less than 6 years.

2020-05-01 17:21

lol, really? useless la.... the fact is below 0.5 is a good buy, above 1.00 is not a good buy

2020-05-01 22:36

Still dare to post this kind of article during bear market....someone must be brain damage, lol

2020-05-01 22:40

sifu dk66, you think 200mil net profit a year to Jaks pocket is possible by 2021?

2020-05-02 00:48

Armada An Quantum Leap Stock In 2019/2020

Wah ! Waited till neck long for icon8888 s article.

Thank you !

2020-05-02 09:29

Klau mcm ni u r talking abt return jz from capacity payment alone right?

Probability the return will be like what the management said to Public Bank IB of ~120M (profit) for 30% stake then

since the capital and interest payment is secured by EVN, its like a having a Bond level return perhaps...

just speculating

2020-05-02 09:34

chl1989, you find my answer here

Jaks Resources - The Most Reliable Earnings Guidance for JHDPhttps://klse.i3investor.com/blogs/Jaks%20resources/2020-05-01-story-h1506848575-Jaks_Resources_The_Most_Reliable_Earnings_Guidance_for_JHDP.jsp

--------------------------

chl1989 sifu dk66, you think 200mil net profit a year to Jaks pocket is possible by 2021?

02/05/2020 12:48 AM

2020-05-02 10:58

One big thing make me not to invest into Jaks is the management. Management style is well known on doing some strange method to chase out the famous investor. Will they will do the same to the small investor? Maybe yes, or maybe not. When the answer is yes, it will cause a big damage on us. Just becareful.

2020-05-02 18:47

AGM is coming. The Directors will seek for re-election during the AGM. If not happy with them may be we should ensure them not elected.

2020-05-02 22:07

The Jaks right issues no details yet? their assumption is 1:5 with free detachable warrant...

2020-05-23 00:32

wah seh Icon8888, your financial model looks very complicated. It's as if you use difficult-to-understand kongfu and ALP simply uses a gun to bring you down with a "peow".

2020-05-24 22:03

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-03 16:35:00

EMA 5

5 Mins

SELL

2024-07-03 16:30:00

EMA 5

30 Mins

SELL

2024-07-03 16:25:00

EMA 5

5 Mins

BUY

2024-07-03 16:05:00

EMA 5

5 Mins

SELL

2024-07-03 16:00:00

EMA 5

Hourly

SELL

Apps

Top Articles

1

AmInvest Research Reports

2

TA Sector Research

3

4

save malaysia!

5

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

DK66

Icon8888, Well done. A very detailed analysis using IRR.

However, I wish to point out that the 25 years concession begins after COD, not including construction period.

------------------

(Depreciation Charges)

Based on depreciation period of 22 years (25 years concession, 3 years construction, 22 years operation), annual depreciation charges is RM340 mil.

2020-05-01 14:31