Road to Success

(RICHE HO) - Research Sharing on Econpile Holdings Berhad

RicheHo

Publish date: Thu, 26 May 2016, 09:53 PM

Full report link: https://www.dropbox.com/s/jkn6r1hb3xp4vdo/Econpile%2026%2005%202016.pdf?dl=0

If you like my research, please give me a like at my FB page: https://www.facebook.com/rhresearch/

For more information about my reports, please email me at richeho_92@hotmail.com

Econpile Holdings Berhad (“ECONPILE”)

Background

ECONPILE was founded by Mr. The Cheng Eng in year 1987. It is a piling and foundation specialist in Malaysia providing piling solutions and foundation works, which includes earth retaining systems, earthworks, substructure and basement construction works.

ECONPILE has a full range of piling (bored piling, driven piles and jack-in piles) and foundation works. It serves the property development and infrastructure sectors, having been involved in the construction of bridges, elevated highways, electrified-double tracking projects and power plants.

To date, ECONPILE has successfully undertaken numerous piling and foundation projects nationwide, including the Klang Valley, Penang, Johor, Pahang, Sabah and Sarawak.

ECONPILE offers a wide range of services including:

- Foundation and Geotechnical Works

- Civil Engineering Works

- Structure Works

- Design and build packages

Piling Industry

Piling and foundation is the essential component of substructure work that upholds the load of the entire building built upon it. It plays a vital role in supporting the construction process as well as ensuring the safety and sustainability of the building.

All construction and property development projects create demand for piling and foundation services. So, the performance of piling and foundation services market players are correlated with the performance of the construction and property development industry.

ECONPILE generates its revenue from both residential and commercial projects.

Entry Barrier

The barrier of entry to the piling and foundation services in Malaysia is relatively high as huge capital investment is required to purchase drilling rigs and other related machinery in order to undertake large-scale projects.

In view of the nature of piling and foundation works, it requires special skillsets and heavy investment in specialised equipment and machinery. Some main contractors may not necessary possess those skillset and necessary equipment and machinery.

Besides, it is not easy for a contractor to obtain Grade “7” license from CIDB.

Market Shares

According to the Independent Market Research report which prepared by Proteg Associates , the piling and foundation services market in Malaysia was valued at an estimated MYR2.96b in year 2013 and it is expected to grow at CAGR of 9.1% for the years 2013 to 2018.

Based on ECONPILE’s revenue of MYR386m in FY13, it has 13% share of the piling and foundation services market in FY13.

So, ECONPILE is considered one of the major player in the piling and foundation services market in Malaysia.

Business Nature

Contract expenses:

- Subcontractor costs – 50%

- Raw materials cost – 30-35%

- Staff costs – 4-5%

- Others – 10-15%

Gross profit margin – 20-25%

Business Overview

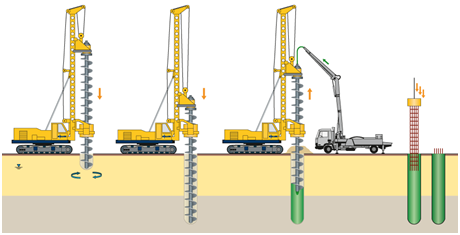

There are various methods in deep foundation work known as piling systems. Driven piling system, jack-in piling system and bored piling system are the three most commonly used piling systems in construction industry.

As for ECONPILE, bored piling solution is its major revenue contribution. From FY11 to FY13, bored pile and foundation services had contributed 90.3%, 96.9% and 95.0% of the group revenue respectively.

Bored pile is a type of pile that is concreted at a permanent location at the holes bored in the ground. It is able to support higher loads in many types of soil condition and thus provide suitable foundation for high rise buildings.

*Illustration

ECONPILE owned a full-fledged workshop in Bukit Beruntung, Rawang, Selangor Darul Ehsan. The operation is supported by a large workforce consisting mechanics, welders, drivers and administration personnel. The facility is equipped with overhead gantry cranes and ancillary lifting equipment.

With the workshop, ECONPILE have the in-house capability to undertake refurbishment, fabrication, modification repair or maintenance works on its fleet of machinery, tools and equipment.

Risk Factors

1. Reliance on approvals, licenses and permits

In Malaysia, it is compulsory for all contractors to register with the CIDB before undertaking to carry out and complete any construction work. The majority of thses licences are subject to annual renewals.

There are total of 7 registration grades, ranking from Grade “1” to “7”, whereby Grade “7” is the highest registration grade. ECONPILE is currently a Grade “7” contractor and with this, it has the capacity to tender for construction works without limit to the valuers.

If unfortunately ECONPILE fails to comply with the rules and guidelines issued by CIDB, its license might be rovoked or not renewed. It will definitely have an adverse effect on its business operations.

However, ECONPILE had been registered with CIDB as Grade “7” contractor since year 1997 and since then it has not encountered any issue in renewing its licence.

2. Project risk

Customers may delay or cancel their projects. Delays may arise from changes in customer requirements or delay in approval by the relevant authorities. Project delays may affect ECONPILE’s profit margins and may delay the recognition of revenues. Besides, additional costs may also be incurred as a result of these delays.

In the event of possible delays in completion of construction projects due to fault of contractor, the architect will make necessary recommendations to customer to deduct the liquidated and ascertained damages (“LAD”) from the contractor’s progress payment, which will in turn reduce the total revenue of the contractor generated from the project.

As such, the timeliness in completing piling and foundation projects is vital in upholdings ECONPILE’s financial performance and reputation in construction industry.

Having said so, so far ECONPILE has not experienced any cancellation of awarded projects and it has not experienced any delay in projects as well.

3. Fluctuations in price of raw materials

ECONPILE purchases a range of raw materials which include cement, pre-mixed and ready-mixed materials, steel bars, etc from its suppliers.

Raw materials are price sensitive, and there can be no assurance that ECONPILE will be able to obtain sufficient quantities of raw materials for its projects when the materials are scare in the market. Price fluctuations in the raw materials are beyond its control and it could result in increased costs.

Its raw materials used for piling and foundation services mainly comprse of cement, concrete and steel.

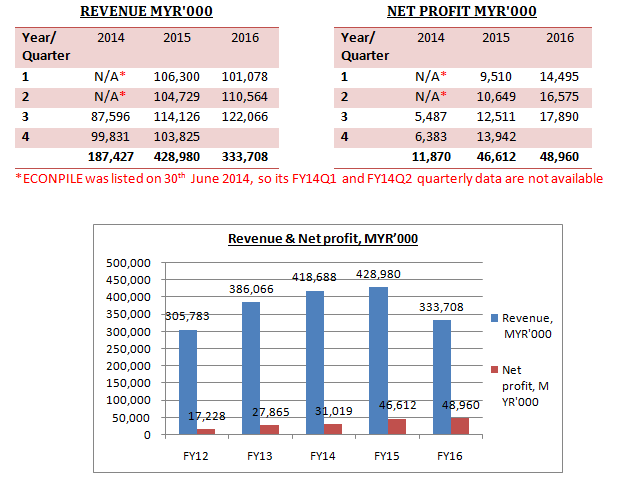

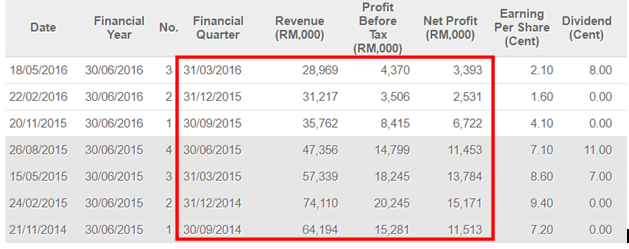

Financial Highlights

ECONPILE’s financial result had been improved for 4 years consecutively since FY12. Its revenue had increased from MYR306m in FY12 to MYR429m in FY15, which equivalent to a compound annual growth rate (“CAGR”) of 11.94%, while its net profit had also increased from MYR17m in FY12 to MYR47m in FY16, which equivalent to CAGR of 39.34%.

In FY16, it definitely will be another excellent year for ECONPILE as its accumulated first three quarter net profit had exceeded its FY15 whole year net profit! It was mainly contributed from the increase in revenue, which resulted from certain major projects reaching its advanced billing milestones.

Besides, its growing result was also contributed by improvement in net profit margin. ECONPILE had enhanced its operations efficiency due to upgrading of machinery and continuous improvement in resource utilization.

Since listed on Main Market in year 2014, ECONPILE was growing slowly and steadily from quarter to quarter despite the challenging external factor in the market.

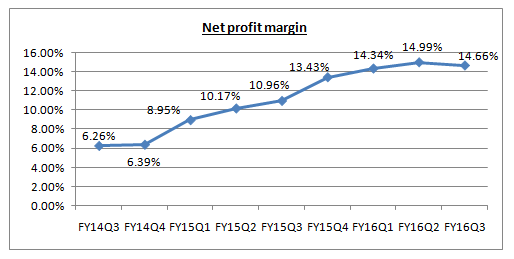

ECONPILE’s net profit margin had increased from 6.26% in FY14Q3 to 14.66% in FY16Q3. In other words, ECONPILE had improved its operations efficiency by more than 50% in two years!

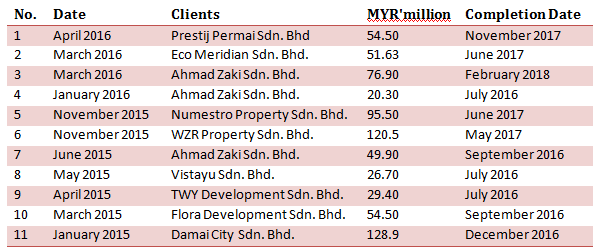

Book Orders

Total secured orders in year 2015 & 2016 – MYR708.73m

As to date, ECONPILE had secured MYR419.33m in FY16 (Jul 15 – Jun 16). If based on its order’s expected completion date in Bursa announcement, all of the orders are still in the progress.

There are 3 orders which are near to its completion date and there are 3 more orders which are going to be completed by end of this year.

ECONPILE doesn’t disclose its current outstanding book orders in Annual Report and also Quarterly Report. So, its current orders cannot be track.

However, based on its revenue of MYR429m in FY15, I believe ECONPILE’s current book orders are sustainable for around 1 year.

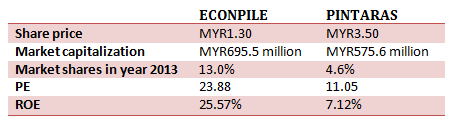

Peers Analysis

Pintaras Jaya Berhad (“PINTARAS”)

Pintaras Jaya Berhad (“PINTARAS”)

PINTARAS is the only listed company in Malaysia which doing the same thing as ECONPILE.

It is a leading foundations and piling specialist based in Shah Alam, Selangor, with twenty-five years of experience in Malaysia’s construction industry. Besides, it also has metal container manufacturing business which contributed 15% of the group’s revenue.

As extracted from http://www.malaysiastock.biz/, PINTARAS financial result is dropping and getting worse from quarter to quarter.

Overall, in term of valuation and financial performance, ECONPILE was greater than PINTARAS, in no doubt.

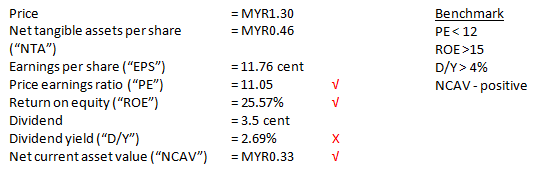

Ratio Analysis

The management of ECONPILE had promised to declare minimum dividends of 20% of its net profit every year.

Based on dividends of 2.5 cent in FY15 and 3.5 cent FY16, ECONPILE had a dividend payout ratio of 29% and 38% in FY15 and FY16 respectively. It proved that ECONPILE management do keep its words.

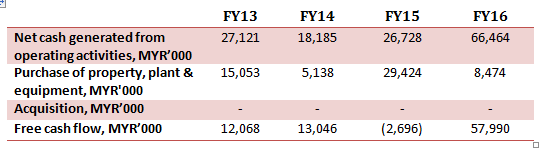

ECONPILE had been generating attractive free cash flow every year except FY15.

In FY15, ECONPILE had invested huge capital expenditure (“CAPEX”) in drilling rigs, crawler cranes, and other equipment. ECONPILE was expanding its range of machinery and replenishing aging and inefficient fleet as part of its ongoing strategy to improve operational efficiency.

As a result, ECONPILE’s profit margin had increased in FY16 (as shown as Financial Highlight above) and subsequently generated more cash flow from its operation.

Share Price Performance

Assume you bought 100 lots of ECONPILE shares with an IPO price of MYR0.54 on Jun 2014.

|

FY15 |

FY16 |

|

|

No. of shares |

10,000 |

10,000 |

|

Dividend, cent |

2.5 |

1.0 |

|

Total div., MYR |

250 |

100 |

As at 26th May 2016, ECONPILE closed at MYR1.30.

- Initial investment = MYR5,400

- Dividend income = MYR350

- Capital appreciation = MYR 7,600

In total, you will have a return of MYR7,950 in two years time, which equivalent to a return on investment of 147.22%. It is also equivalent to CAGR of 57.23% over the past two years.

Conclusion

For the first three months of this year, the Malaysian economy grew at 4.2%. It is still within the range of the expected rate, which is between 4 and 4.5%.

It noted under the Eleventh Malaysia Plan (11MP), the construction industry will contribute up to 5.5% of GDP to the economy by year 2020 and has two times multiplier effects with more than 120 industries depending on construction sector for their growth.

Demand for specialist construction works such as piling remains robust in FY16. This industry benefit from key infrastructure projects this year and big property developments.

Since its establishment, ECONPILE had transformed itself from a small piling company to a bored piling and substructure specilalist. Its market shares in piling industry is more than 10%. It had secured more than MYR400m book orders in FY16 and look forward for more.

With its current order replenish rate, ECONPILE is expected to continue grow slowly and steadily. It is definitely a good value company to invest for long term.

Just for sharing.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Road to Success

(RICHE HO ) Y.S.P. Southeast Asia - Boring Counter with Strong Track Record

Created by RicheHo | Mar 18, 2017

(RICHE HO) Latitude Tree Holdings Berhad - Earnings Recovery in FY17

Created by RicheHo | Feb 19, 2017

(RICHE HO) Ajiya Berhad - Green IBS Provider, Benefited from PR1MA project

Created by RicheHo | Feb 16, 2017

(RICHE HO) Benalec Holdings Berhad - Strong Earnings from Tanjung Piai & Pengerang MIP

Created by RicheHo | Jan 08, 2017

Discussions

5 people like this. Showing 4 of 4 comments

Good write up, Riche Ho, and on June 2nd Econpile received a RM208mil contract. So, we should continuously update the amount of contracts secured here.

2016-06-03 06:58

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-12-23 10:30:00

VOLUME BREAKOUT

30 Mins

BUY

2024-12-23 10:00:00

VOLUME BREAKOUT

Hourly

BUY

2024-12-23 10:00:00

TURTLE SYSTEM 20

Hourly

BUY

2024-12-23 09:30:00

TURTLE SYSTEM 20

30 Mins

BUY

2024-12-23 09:00:00

EMA 5

Hourly

BUY

Apps

Top Articles

1

Stock Market Enthusiast

Top 3 AI/Data Center Newsflow for the 3rd Week of December - #TENAGA, #YTL, #YTLPOWER

2

save malaysia!

3

save malaysia!

5

6

save malaysia!

7

Good Articles to Share

China property flare-ups resurface as crisis enters fifth year

8

Good Articles to Share

US fighter shot down in 'apparent case of friendly fire' over Red Sea

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

chl1989

bro Riche ho, what is your target price? It seems like it is quite fully valued at this price. Very good company in terms of ROE/ROIC, healthy balance sheet & cash flow and high growth, but no longer cheap.

2016-05-30 03:01