Icon8888 Gossips About Stocks

(Icon) TAS Offshore - Export Oriented Oil & Gas Play

Executive Summary

(a) When I first started writing about TAS Offshore, my intention is to write about an oil and gas play (Oil price is kind of recovering. Maybe one day will spike again ?).

However, as I dug deeper, I discovered that this company is actually an export play. The group sold almost 95% of its vessels to overseas customers.

(b) According to the Company's website, approximately 53% sale is to oil and gas customers while the remaining 47% is to non oil and gas sectors (note : not sure how updated these figures are).

The recent decline in oil price reduces demand for oil and gas related suppot vessels. However, the Ringgit has weakened substantially. This gives the company advantage when come to pricing.

Is the weak oil price a blessing in disguise for the group ?

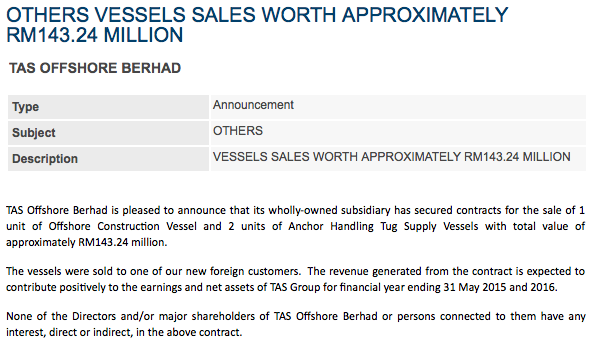

As if to confirm the above theory, the company announced on 27 January 2015 that they have secured a RM143 mil contract to construct new vessels for overseas customer.

Tas Offshore Bhd (TOB) Snapshot

|

Open

0.76

|

Previous Close

0.77

|

|

|

Day High

0.77

|

Day Low

0.76

|

|

|

52 Week High

07/16/14 - 1.65

|

52 Week Low

12/16/14 - 0.63

|

|

|

Market Cap

135.4M

|

Average Volume 10 Days

754.2K

|

|

|

EPS TTM

0.13

|

Shares Outstanding

175.8M

|

|

|

EX-Date

05/12/14

|

P/E TM

6.0x

|

|

|

Dividend

0.02

|

Dividend Yield

2.60%

|

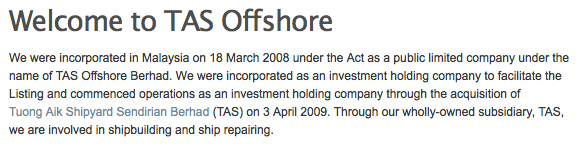

TAS Offshore Berhad, an investment holding company, engages in the shipbuilding and ship repairing activities in Malaysia.

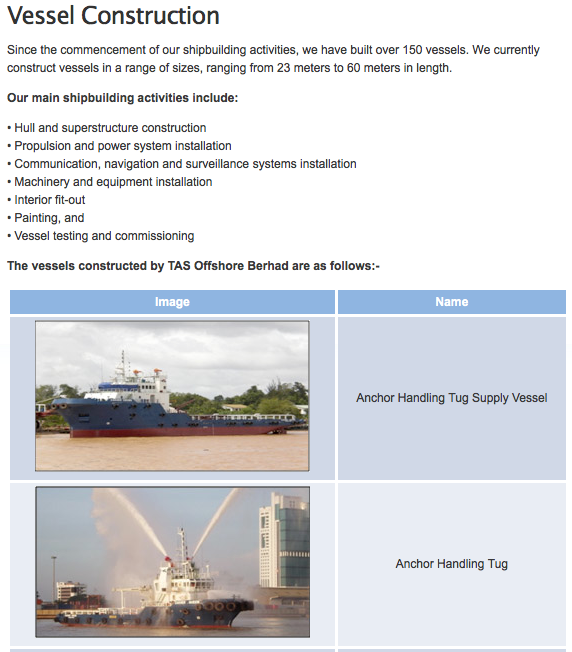

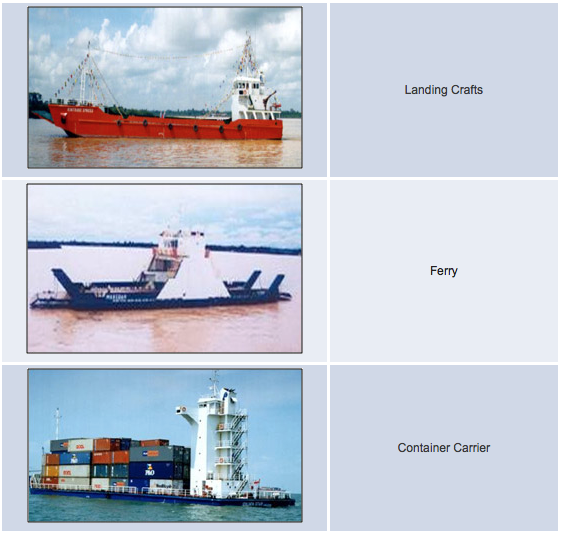

The company constructs a range of vessels, including tugboats, harbour tugs, anchor handling tugs, anchor handling tug supply vessels, landing craft, utility/support vessels, barges, ferries, and workboats, as well as pusher tugs and container carriers.

Its ship repair services comprise routine marine engine, machinery, and equipment inspection and maintenance, etc.

The company also operates in the United Arab Emirates, Indonesia, Singapore, Saint Vincent Island, Papua New Guinea, and Panama. TAS Offshore Berhad was incorporated in 2008 and is headquartered in Sibu, Malaysia.

-----------------------------------------------------------------------------------------------------------------------------

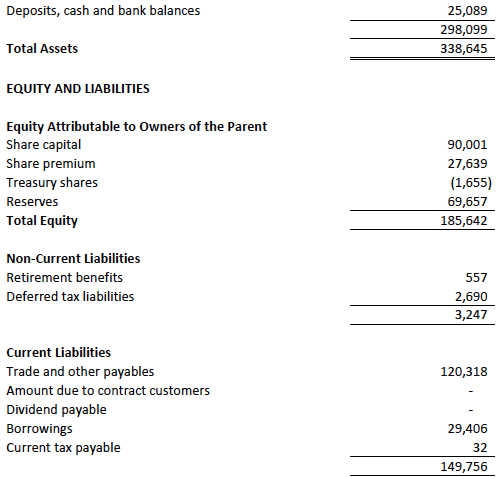

The group has strong balance sheets. With net assets of RM186 mil, loans of RM29 mil and cash of RM25 mil, net gearing is 2% only.

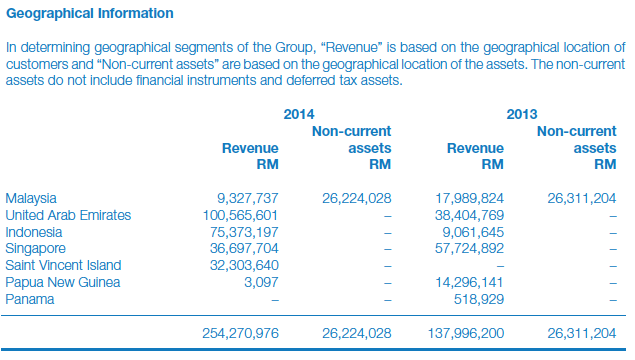

For the financial year ended 31 May 2014, only 3.7% of the group's revenue was from Malaysia. The remaining was from overseas.

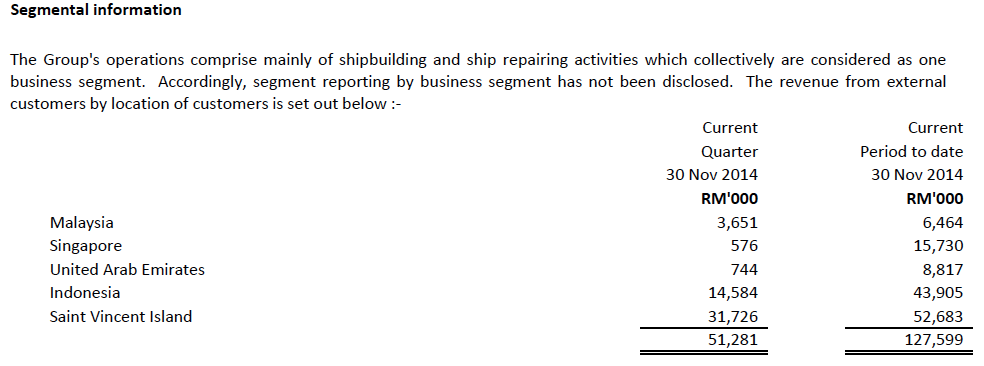

For the 6 months ended 30 November 2014, only 5% of revenue is from Malaysia while the remaining 95% from overseas.

Annual Result:

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | PE | DPS (Cent) | DY | NAPS | ROE (%) |

|---|---|---|---|---|---|---|---|---|

| TTM | 303,184 | 22,589 | 12.85 | 6.00 | 2.00 | 2.60 | 1.0313 | 12.46 |

| 2014-05-31 | 254,271 | 28,785 | 16.37 | 8.25 | 2.00 | 1.48 | 0.9705 | 16.87 |

| 2013-05-31 | 137,996 | 13,455 | 7.65 | 6.54 | 2.00 | 4.00 | 0.8458 | 9.04 |

| 2012-05-31 | 101,573 | 11,332 | 6.40 | 5.63 | 1.50 | 4.17 | 0.7850 | 8.15 |

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit before Tax ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS |

|---|---|---|---|---|---|---|---|

| 2015-05-31 | 2014-11-30 | 51,281 | 4,223 | 4,151 | 2.36 | - | 1.0313 |

| 2015-05-31 | 2014-08-31 | 76,318 | 6,507 | 5,451 | 3.10 | - | 0.9997 |

| 2014-05-31 | 2014-05-31 | 61,295 | 2,342 | 2,532 | 1.44 | - | 0.9705 |

| 2014-05-31 | 2014-02-28 | 114,290 | 12,280 | 10,455 | 5.95 | 2.00 | 0.9764 |

| 2014-05-31 | 2013-11-30 | 49,042 | 9,463 | 7,265 | 4.13 | - | 0.9167 |

| 2014-05-31 | 2013-08-31 | 29,644 | 10,218 | 8,532 | 4.85 | - | 0.8968 |

| 2013-05-31 | 2013-05-31 | 48,385 | 3,279 | 3,080 | 1.75 | 2.00 | - |

| 2013-05-31 | 2013-02-28 | 41,120 | 6,114 | 5,250 | 2.98 | - | 0.8292 |

| 2013-05-31 | 2012-11-30 | 30,719 | 3,593 | 2,420 | 1.38 | - | 0.8001 |

| 2013-05-31 | 2012-08-31 | 17,772 | 3,720 | 2,705 | 1.54 | - | 0.8002 |

As shown in tables above, the group has done well in past few years.

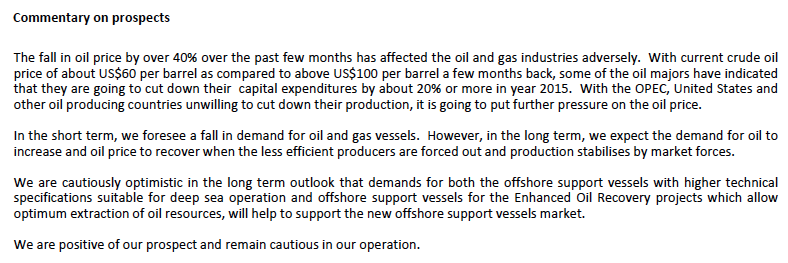

Management's comments on the group's prospects as set out in November 2014 quarterly report :-

On 27 January 2015, the company announced that they have secured RM143 mil contract from an overseas customer for new vessels :-

The new contract of RM143 mil represents 56% of FY2014 revenue of RM254 mil. Together with other already secured contracts, the group should have sufficient work to keep it busy over next one to two years while waiting for industry demand to pick up again.

The following is an article dated 29 January 2015 regarding TAS Offshore :-

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

2 people like this. Showing 6 of 6 comments

Probability the writing help me to think

That insight and command of details cannot be obtained without putting thoughts down in words

2015-02-25 21:40

Calvin, they made sampan

Not your mighty bulk carriers

Unlike rich Singaporeans like u, we Malaysian can only afford sampans

2015-02-25 21:57

i did a quick review

Based on preliminary analysis, it seemed that the negative figures were mostly due to changes in working capital. For example, in FY2014, there was an increase in amount due from customers totalling RM53 mil and increase in receivables totalling RM44.4 mil. These are normal trade related items. There are neither positive nor negative from economics point of view. The important point is that collection is managed effectively and there is no huge amount of bad debts (a quick check of financial statements showed that this is not a major issue).

Just to double check, I inspected Nov 2014 quarterly report. Net assets is RM186 mil, inventories is RM87 mil, debtors are RM184 mil, payables are RM120 mil. When put together, these figures looked balanced and normal. Nothing to be alarmed at.

In my opinion, negative cash-flow that you need to pay attention is those that comes with a lot of capex (a famous case is London Biscuits). It is an indication of trouble either due to (1) irrational spending ("Rolls Royce" items); or (2) bad corporate governance; or (3) lack of competitive advantage and require continual spending to sustain performance.

I hope I answer your question. Please feel free to disagree if you find further valid points to show that negative FCF is indeed a problem for this group.

2015-02-26 11:23

Thanks for the write-up. But OSV is already in oversupply condition with Daily Charter Rate declining. And the current low CO price will also discourage O&G Capex.

2015-02-27 15:57

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-04-29 16:40:00

EMA 5

5 Mins

BUY

2024-04-29 15:40:00

EMA 5

10 Mins

SELL

2024-04-29 15:35:00

EMA 5

5 Mins

SELL

2024-04-29 15:05:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-04-29 15:00:00

EMA 5

10 Mins

BUY

Apps

Top Articles

1

2

AmInvest Research Reports

3

4

5

6

7

8

TA Sector Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Probability

Wah...Icon...you are very good asset for i3!

2015-02-25 21:13