Icon8888 Gossips About Stocks

(Icon) Comcorp (1) - Super Export Play Trading at 3.7x PER. Potential Upside of 170%.

Executive Summary

(a) Comintel Corp (Comcorp) is principally involved in contract manufacturing services, specializing in Radio Frequency engineering products.

(b) Its manufacturing division accounted for 96% of group revenue. According to annual report, entire 100% of its revenue is denominated in US Dollar.

(c) Yesterday, Comcorp announced its October 2015 quarterly result. EPS came in at 3.47 sen. Based on latest share price of 52 sen and annualised EPS of 14 sen, PER is only 3.7 times.

(d) Earnings explosion was due to profit margin expansion caused by strong US Dollars. In my opinion, USD will remain strong over an extended period of time. The group's strong earning should be sustainable.

(e) By applying a PER of 10 times, fair value should be RM1.40, a further upside of 170%.

1. Background Information

Comcorp is listed on the Main Market of Bursa Malaysia. It has 4 major divisions. However, the manufacturing division dominates both revenue (96%) and net profit (100%).

Comcorp is a contract manufacturer, just like VS Industry. It specializes in manufacturing of Radio Frequency engineering products.

It is a pure exporter with 100% of its manufacturing revenue denominated in US Dollars (please refer below).

2. Historical Profitability

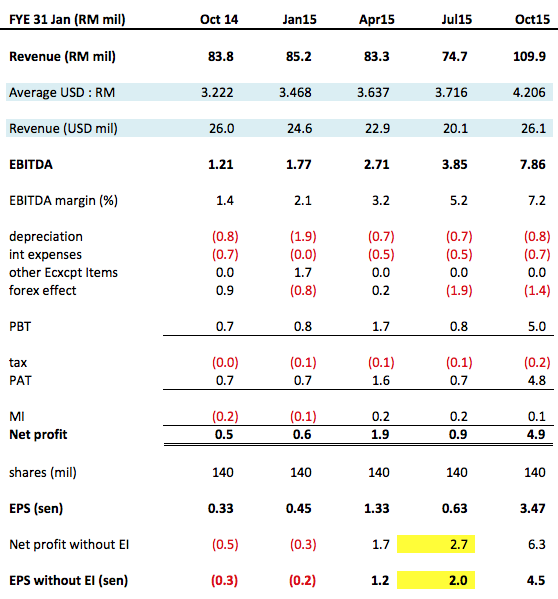

The table below sets out Comcorp's past few quarters P&L :

Key observations :-

(a) The group has not been performing well in the past. For example, in October 2014 quarter, the Group reported net profit of RM0.5 mil only. In that quarter, USD : RM exchange rate was 3.222.

(b) However, things improved dramatically in calender year 2015. In April 2015 quarter, net profit ballooned to RM1.9 mil despite flattish revenue. During that quarter, USD : RM exchange rate was 3.637.

(c) In the latest October 2015 quarter, net profit literally exploded. Backed by strong USD : RM exchange rate of 4.206, the group reported an astounding net profit of RM4.9 mil.

Y-o-y, revenue in US Dollar term has not grown at all (USD26.1 mil in October 2015 quarter vs USD26 mil in October 2014 quarter). However, the strengtheing of USD from 3.222 to 4.206 caused net profit to grow from RM0.5 mil to RM4.9 mil.

These are pure operating profit, not caused by Forex gain or any other exceptional items. As a matter of fact, the group incurred forex loss of RM1.4 mil in latest quarter.

The company is positive about its prospects going forward :-

3. Balance Sheets

The group has net assets of RM105 mil, loans of RM96.2 mil and cash of RM42.4 mil. Net gearing is 0.51 times.

I am totally not concerned about the Group's gearing. Some of the loans were drawn down to finance its new green energy division and they are backed by TNB offtake. Others are for working capital purposes.

The group's earnings are strong and capex requirement is low. They shouldn't have problem servicing their financial obligations.

4. Concluding Remarks

(a) The group has other divisons such as green energy, ICT and defense maintenance. However, they accounted for very small portion of the group's revenue and profitability.

The Group is essentially a contract manufacturer, same as VS Industry.

(b) This stock is UNDERVALUED BEYOND DOUBT. If you do not have the courage and the wisdom to take position at current price of 52 sen, you probably shouldn't be in the market.

BUY !!!!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

3 people like this. Showing 50 of 265 comments

Sold with 6 figure profit. Thanks Comcorp and especially to you Icon8888

2015-12-21 13:10

congrats for the spot on write up on Comcorp. looking forward to another gem soon. tks

2015-12-21 16:21

timing already prove wat icon8888 y is right. were those ppl argue with him?

2015-12-22 13:23

Dear all pls read how calvintaneng tembak and cannot answer my question...he really famous to mislead ppl

http://klse.i3investor.com/servlets/forum/800003035.jsp

2015-12-23 23:14

The co is expected to do better nex qtr .this rfid ind has bright future and wud enjoy double digit growth . A fair earnings multiple of 12 times is not far fetch. With 14cts eps very soon the price may hit 1.68 congrats icon 88.speculate within 1.5 moths time.Medium sized funds are now looking into it

2015-12-24 19:02

Posted by alphajack > Dec 23, 2015 11:58 AM | Report Abuse

1.20-1.30 by CNY

according to logic. the above mentioned person should have been KLC already due to his endless mistake calls.

KLC= kualouchan.

2016-01-29 19:56

optimus, Desa, paperplane, 3 of you bankrupt already ka? why so angry? me and Icon counting money until hands soft already, wakakakakaka

2016-02-15 20:20

see, Icon so happy, wish you all kong hi fat choi so more, you know why? because he counting money until hands soft

2016-02-15 20:21

Me and Icon now don't talk so much already, because we so busy counting money, wakakakaka

2016-02-15 20:22

better save our energy counting money lah, quarrel with this 3 kids only when we are bored

2016-02-15 20:33

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-23 16:10:00

EMA 5

10 Mins

SELL

2024-07-23 15:55:00

ADX

5 Mins

SELL

2024-07-23 15:50:00

ADX

10 Mins

SELL

2024-07-23 15:45:00

ADX

5 Mins

BUY

2024-07-23 15:40:00

ADX

10 Mins

BUY

Apps

Top Articles

1

BFM Podcast

2

Koon Yew Yin's Blog

3

CGS-CIMB Research

Genting Plantations - Proposed Land Acquisition in Indonesia

5

save malaysia!

6

南洋 - 凭单专栏/温世麟

7

Koon Yew Yin's Blog

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Ryan88

300k to sapu anythings below 0.80 tmr

2015-12-20 18:03