iVSA Stock Review

Holistic View of MKH with Fundamental Analysis & iVolume Spread Analysis (iVSAChart) - 25/02/16

Does Mid-Size Developer MKH possess the growing potential?

MKH Berhad, an investment holding company, primarily provides building management services. Its other activities include property development and investment; operation of a recreational club; building and civil works contracting and provision of project management services; money lending, hire purchase, and leasing finance; provision of management and secretarial services; and insurance agency operations.

The company also engages in trading of building materials and household related products, and food and meat related products; livestock farming and oil palm cultivation; food processing and trading; furniture manufacturing; and hotel business. It has operations in Malaysia, the Peoples Republic of China, and Indonesia. The company was formerly known as Metro Kajang Holdings Berhad and changed its name to MKH Berhad on April 1, 2011. MKH Berhad was incorporated in 1979 and is based in Kajang, Malaysia.

MKH becomes company with a billion Ringgit turnover in their latest financial year (FY) results in 2015, thanks to their continuous growing revenue during post Lehman Brother crisis years (FY2010 onwards). Other aspects of the company’s latest financial results are illustrated in the table below.

Below are the company’s latest financial year figures.

|

Company |

MKH Bhd (FY 2015) (RM’000) |

|

Revenue (RM’000) |

1,041,902 |

|

Net Earnings (RM’000) |

86,330 |

|

Net Profit Margin (%) |

8.286 |

|

Total Debt to Equity Ratio |

0.727 |

|

Current Ratio |

1.554 |

|

Cash Ratio |

0.313 |

|

Dividend Yield (%) |

3.029 |

|

PE Ratio |

10.79 |

MKH Bhd has achieved a spectacular non-stop revenue growth since FY2010 till FY2015, from RM 291 million till today’s RM 1.041 billion, which translates to 3.58 times growth within a short 5 years. In terms of net profit, although the company has increase profit 2.89 times within these 5 years (from RM 29 million to RM 86 million), however the company’s peak profit was achieved back in FY2013 at RM 103 million which then followed by a decrease to RM 86 million in FY 2015.

This drop in profit is mainly due to weaker crude palm oil (CPO) and palm kernel selling prices, higher unrealised foreign exchange losses and lower gain in fair value from investment properties. Net profit margin wise the company is performing within acceptable range at 8.286%. The net profit margin could be higher as it was affected by the company’s palm oil division, which contributes about 20% of the company’s total revenue.

In terms of the company’s balance sheet, the total debt to equity ratio at 0.727 is still acceptable as it shows that the company’s equity value is still higher than its total debt. Current ratio wise scoring at 1.554 is a good sign which means that current asset of the company is of 1.5 times the value of its current liabilities. However in terms of cash ratio, 0.313 does not give an “A” score as it signifies that the company only holds the amount of cash that can only pay off 31.3% of its current liability. Usually financially strong companies carry at least 50% and above which gives a cash ratio of 0.5.

Dividend wise MKH Berhad gives a 3% dividend yield which is slightly above average and just enough to keep dividend seeking investors happy.

In conclusion, MKH Berhad’s most spectacular achievement is their consistent revenue growth for the past 5 years and having debt to equity ratio less than 1. These aspects are important for property developers as high competition and high gearing is part of the business nature. The main concern for MKH is to sustain their net profit growth whereby currently it is badly affected by their palm oil division. In view that 80% the company’s revenue comes from property development and the company still have a substantial list of ongoing projects, this company still have the potential to grow in a long run.

(Feb 25, 2016 share price: RM 2.220)

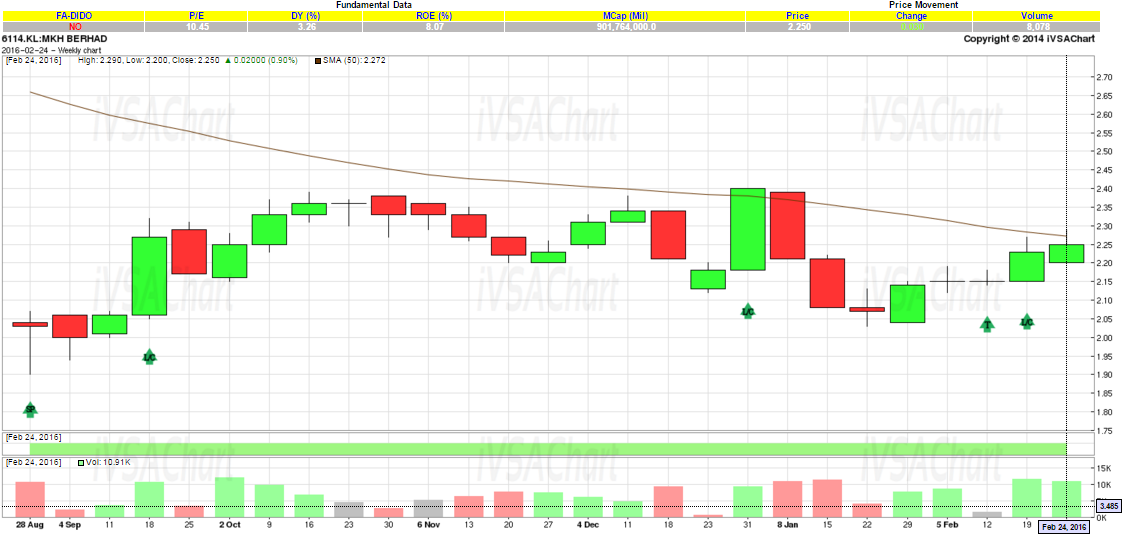

iVolume Spread Analysis (iVSA) & comments based on iVSAChart software – MKH

MKH is building a nice support base @ RM2.10-RM2.05. At the same time, we had 2 sign of strengths giving its potential for upside. Upside resistance @ RM2.40 where higher prices are rejected. Breaking above RM2.40 will resume MKH to the upside.

Buy on accumulation for MKH.

Any Enquiry?

- WhatsApp: +6011 2125 8389/ +6018 286 9809

- Email: sales@ivsachart.com

- Follow us on Facebook: https://www.facebook.com/priceandvolumeinklse/ and website www.ivsachart.com

More articles on iVSA Stock Review

Holistic View of Leon Huat with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 15, 2016

Holistic View of Tomypak with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 15, 2016

Holistic View of ECS IT with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 01, 2016

Holistic View of Magni-Tech with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Dec 01, 2016

Holistic View of Teo Seng with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Nov 14, 2016

Holistic View of QL Resources with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Nov 03, 2016

Holistic View of Top Glove with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Oct 24, 2016

Holistic View of Scientex with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Oct 24, 2016

Holistic View of KESM with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Created by Joe Cool | Oct 17, 2016

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

南洋行家论股

3

The Alpha Trader

4

BreakingOut

5

Koon Yew Yin's Blog

6

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

7

南洋行家论股

8

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....