kcchongnz blog

Isn’t this the most undervalued stock in Bursa?: Insas Berhad by Kcchongnz

Insas Berhad (Insas) operates in the five segments:

1. Financial Services: Stock broking, provision of corporate finance & advisory services and structured finance

2. Investment holding and trading.

3. Technology & IT related services

4. Retail trading and car rental

5. property investment and development

Let us look at its latest financial statement ended 30 September 2023. The balance sheet of Insas is shown Table 1 in the Appendix. For ease of reference, I have summarized its assets and liabilities into a few categories in amount as well as in per share basis of Insas.

What do we see?

The deep undervaluation of Insas

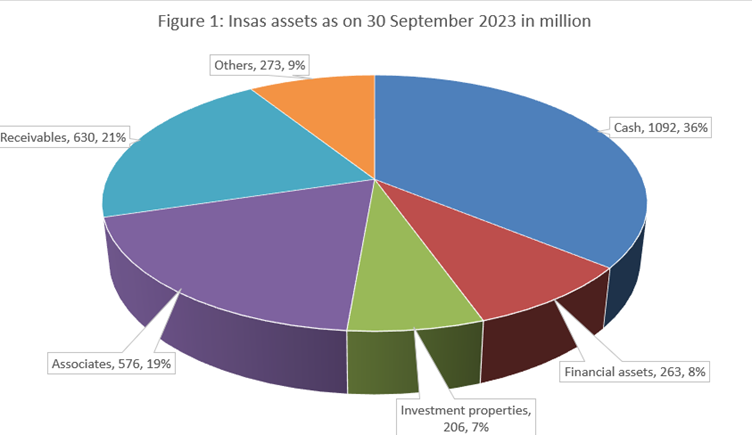

Figure 1 below shows the assets distributions of Insas as on 30 September 2023.

Table 1 in the Appendix shows that Insas has a net asset of RM2,361 m, or RM3.56 per share. At the price of 99.5 sen, it is only 28% of its NAB, or a discount of 72% as shown. Using Benjamin Graham’s deep value metrics, the net current asset value of Insas, NCAV is RM3.44 and net-net of RM2.94. The share price of Insas is trading at a discount of 71% and 66% to its NCAV and Net-net respectively.

Note that most of Insas’s assets are not some intangible assets or low-quality assets such as PP&E, Receivables, Inventories etc., but most assets are made up of cash and cash equivalent, and other financial assets which are marked-to-market and can be readily converted to equivalent cash value.

Furthermore, the values of the associated companies, especially the listed securities in Inari and Ho Hup, Omesti etc., were recorded as book value of RM576m, or just 87 sen per share, whereas the market value of its 14.4% Inari holding alone at the price of RM3.15 on 14 January 2024 is worth RM1,692 million, or RM2.55 per Insas share. That is a difference of RM1.68 per share more than its total holding in Associate companies. Neglecting other minor associated companies, this could mean the net asset backing per share of Insas is worth about RM5.24, and its Graham net-net, a conservative asset valuation, is worth RM4.62 per share, way above its market price of 99.5 sen.

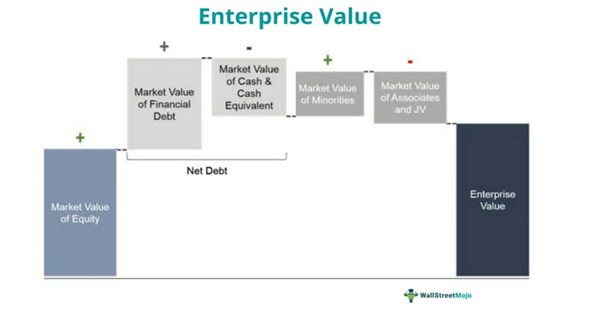

Negative Enterprise Value stock

Think of enterprise value as the theoretical takeover price. In the event of a buyout, an acquirer would have to take on the company's debt, pay off its minority interest, but would dispose off all liquid assets and pocket its cash. EV differs significantly from market capitalization in several ways, and many consider it to be a more accurate representation of a firm's value. The value of a firm's debt, for example, would need to be paid by the buyer when taking over a company, thus EV provides a more accurate takeover valuation because it includes debt and non-operating cash in its value calculation.

EV = Market Cap + Total Debts + Minority Interest – Cash and cash equivalent – Other Investments

What is negative Enterprise Value?

Let’s work out the enterprise value of Insas.

At 99.5 sen a share and a total outstanding shares of 663 m, the market cap of Insas is RM660m.

Market cap = 0.995 * 663 = 660 m

Table 1 in the Appendix shows that Insas total debts of RM386 m as extracted from its balance sheet on 30 September 2023 which includes all borrowings and lease liabilities.

It has a total of cash and cash equivalent of RM1,092 m.

Other investments in financial assets at fair value of RM263 m.

There are these other investments in Associates companies of listed companies in Inari, Ho Hup, Omesti etc., and other non-listed company of total RM576 m in its non-current assets. In this case, we will just consider the market value of Inari of RM1692 m as the liquid asset in this category.

Hence, Enterprise value of Insas,

EV = Market Cap + Total Debts + Minority Interest – Cash and cash equivalent – Other Investments

EV = 660 + 386 + 157 – 1,092 – 263 – 1,692 = -1,844 m

The enterprise value of Insas is hence a negative value of RM1,844 m.

A negative enterprise value stock means that its cash and cash equivalent and other liquid investments is higher than its market cap plus total debts and minority interests. It presents an arbitrage opportunity for investors.

Arbitrage opportunity in Insas

In this arbitrage opportunity, theoretically someone can borrow RM587 m from banks to buy up all the Insas shares in the open market at RM0.885, and after gaining control of the company, strip off the liquid assets and investments, payoff company loans and minority interest, and pay off all personal bank loans borrowed for this purpose, and pocket cash left over, and still own the remainder business for free.

This is how arbitrage of Insas can be theoretically done by an investor as shown in Table 2 below,

| Price | 0.995 |

| Number of shares | 663 |

| Market cap | 660 |

| Table 2: Arbitrage opportunity | RM million |

| Borrow and buy all shares | 660 |

| Pay for shares | -660 |

| Sell all Inari shares | 1692 |

| Liquidate all other financial assets | 263 |

| Rip off all Cash in banks | 1048 |

| Total cash available | 3003 |

| Pay Preference shareholders | -129 |

| Pay off MI | -157 |

| Pay all company debts | -258 |

| Total debts paid | -543 |

| Pay personal loan | -660 |

| Total to pay | -660 |

| Pocket money | 1800 |

The positive signs show cash in and negative signs, cash out for the investor.

The above shows that without coming out any money from his own pocket, but from borrowing from bank, the investor can pocket a whopping RM1,800 m after carrying out the above actions, and still own the remainder business and assets of the company.

The problems

It is easier said than done for most of the arbitrages as there are numerous problems in a hostile takeover attempt. For example, in Insas’s case, the major shareholders is controlling it through the high majority stake in the company, through its warrants, and other ways such as “poison pills”, etc.

The negative Enterprise Value type approach is also far from free from downside risks. This may be because judging a company’s true current cash position, as opposed to its last reported cash position, is fraught with difficulty and there is also no guarantee that the company management will act in the best interest of shareholders in its use of these cash proceeds.

The other issue is how long investors have to wait for the unlocking of the value, in Insas’s case, it has been a long time since the stock has been undervalued.

The other major problem is a deeply undervalued stock could be due to its deteriorating business with continued losses and cash burns. In Insas’s case, it may not be the problem as Insas’s core businesses have been making money at operating level (haven’t considered the increase in net income level due to its investments in Inari) and earning positive cash flows over the years. Its equity value has been increasing nicely over the years too, even after distributing reasonably good dividends.

I could only speculate on the persistent undervaluation of Insas as follows.

Less Focus on Minority Shareholders

A higher portion of ownership of shares is by insiders, resulting in negligence towards the common investor. Insas has been distributing meagre dividend to shareholders in the past. However, in recent years, dividends have increased and based on its share price, the dividend yield is quite decent.

Lack of interest from institutional investors

if institutions like unit trust funds, EPF, and closed-end fund don’t own enough percentage of stocks to influence decision making or ability to generate the right amount of votes on disagreement in business management, it results in a lack of interest in institutional investors, and such stocks become value traps for retail investors.

Various Small Factors

Many parameters affect investment decisions on an institutional level to invest in certain companies like stock price, market cap, revenue, etc. Some institutions prefer to invest in a company after it shows a certain level of growth in the market.

So, when the time the management shows its prowess in growing the business, or invest in other good businesses, or when the institutional investors get interested in Insas due to its extreme undervaluation, there will be an upward revision of its valuation.

Conclusions

The compelling investing thesis for Insas lies in its assets, which the net asset is way above its current market price, and those assets mostly having market values.

That basically forms my investing thesis for Insas, because of its quality asset backing, there is limited downside, but plenty of upside potential.

“Take care of the downsides; the upsides will take care of itself.”

I see very little risk investing in this company at this price of 99.5 sen.

You are invited to visit my Facebook page below,

https://www.facebook.com/kcchongnz/

KC Chong

Appendix

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on kcchongnz blog

Insas Warrants WC and Its Valuation kcchongnz

Created by kcchongnz | Jan 22, 2024

Which to buy, Insas or Insas WC?

2024 New Year Reflection Investing in the Stock Market: Timing the Market

Created by kcchongnz | Jan 01, 2024

2023 Christmas reflection on pitfalls of investing in the Malaysian stock market kcchongnz

Created by kcchongnz | Dec 25, 2023

Introduction: The Complete Dividend Investing Guide That Works by K C Chong

Created by kcchongnz | Oct 02, 2022

Discussions

8 people like this. Showing 36 of 36 comments

KCChongNZ thanks for your educational articles.

I have been reading them for the past 7 years. You have been a guiding light in my investment journey.

Please do continue to publish your research articles.

2024-01-15 23:56

kcchongnz,

Welcome back. You are one of best analysts besides icon8888. I missed icon8888 too. Don't know how he is doing?

2024-01-16 00:40

Thanks for your friendly gestures, my friends. I am particularly moved by the comment of connie7i3. You are welcomed to visit my FB page, kcchongnz, too.

2024-01-16 03:45

Good morning KCChong,

Just for information:

Under trade receivables include:

Moneylending subsidiary company : Insas Credit & Leasing Sdn Bhd

Paragraph 8.23(2)(e) Appendix 8D(1) - Aggregate amount of outstanding loans as at 31 December 2023

Category of loan receivables Secured Unsecured Total

RM'000 RM'000 RM'000

(a) Corporations 182,943 84,250 267,193

(b) Individuals 16,979 - 16,979

(c) Corporations within Insas Berhad Group - - -

(d) Related parties - - -

Total 199,922 84,250 284,172

Omesti is not an associate company, it is one of the many financial assets at fair value thro' profit and loss

ASSOCIATE COMPANIES (CONT’D)

(f) The summarised financial information in respect of the Group’s major associate companies are as

follows:-

Inari Amertron Company Group

Ho Hup Construction Berhad Group

Melium Holding Sdn Berhad Group

Divfex Berhad

Other associate companies

Total

RM’000 RM’000 RM’000 RM’000 RM’000 RM’000

Financial positions as at 30 June 2023

Assets and liabilities

Non-current assets 528,103 536,203 58,853 12,249 200,905 1,336,313

Current assets 2,438,649 994,312 60,262 66,447 307,968 3,867,638

Non-current liabilities (32,672) (391,067) (35,073) (7,122) (34,046) (499,980)

Current liabilities (331,450) (734,688) (50,060) (40,987) (254,115) (1,411,300)

Net assets 2,602,630 404,760 33,982 30,587 220,712 3,292,671

Carrying amount of proportion of the

Group’s ownership 374,407 18,617 14,646 8,259 96,529 512,458

Goodwill on acquisition 65,251

Total: 577,709

Note: MI is mainly non-controlling interest of M&A

Stock [M&A]: M & A EQUITY HOLDINGS BERHAD

Announcement Date 05-Jul-2023

Reference No CS2-05072023-00007

Substantial Shareholder's Particular:

Name INSAS BERHAD

Details of Changes:

Currency -

Date of Change Type Number of Shares

30-Jun-2023 Acquired 10,502,200

Registered Name M & A Nominee (Asing) Sdn Bhd for Montego Assets Limited

Nature of Interest Indirect Interest

Nature of Interest Indirect Interest

Shares Ordinary Shares

Reason Acquisition of shares in the open market.

Total no of securities after change

Direct (units) 206,627,756

Direct (%) 50.49

Indirect (units) 0

Indirect (%) 10.34

Total (units) 1,215,718,665

Total (%) 60.83

Date of Notice 05-Jul-2023

Still need to buy all the WC beside Insas shares. Or you can wait untill WC expired then you make an attempt takeover.

WARRANTS HOLDINGS

as at 29 September 2023

WARRANTS 2021/2026

No. of outstanding warrants : 331,510,380

Exercise price per warrant : RM0.90

Expiry date of warrants : 28 February 2026

Remark: Insas controlling shareholders Dato' Sri Thong and PAC officially hold 32.96%, 0.04% short of triggering 33% threshold of MGO

2024-01-16 06:26

Hi KC

Nice to see u here.

Your article is great n really explain precisely what value investors to look for & capitalise on.

Base insas negative enterprise value of Rm 1,844M or Rm 2.79 per share, an investor can takeover Insas for free & pocket Rm 2.79 per share loh!

Rationally this really ridiculous but it is a fact & real loh!

On top of that KC only monetize Inari & insas other liquid assets but exclude insas other listed subsidiary namely M&A, Insas sizeable real estate properties, profitable unlisted business ,Associate listed Ho Hup and Insas all other assets loh!

The above deep quality undervaluation shows that insas is really conservatively well manage thus debunked the notion of poor mkt perception loh!

Big shark should take this good opportunity to buy up insas by taking a sizeable stake of Insas & be a profitable business partner of Tan Sri Thong loh!

Actually Thong can be a good business partner & shows very good governership for example Inari has very good perceive governance compare to Insas loh!

I m sure Thong can easily adapt to this higher standard base on the current management formula as per Inari model!

The ideal position for the new opportunistic big investor is 20% stake of insas loh!

Assuming taking up 20% stake at average price of Rm 1.50 will only cost him Rm198m compare to Insas overall shareholders revise capitalization of more than Rm 3.3B or equivalent to Rm 660m @20% stake loh!

For small investors u should start buying insas now & side with the future opportunistic large investors loh!

As for Sifu Sslee, Raider suggest that he should forget about giving an exemption to Thong, if a GO trigger bcos of him buying or exercising his warrant as the cost of GO is only Rm 1M which is peanuts to him compare to Insas negative enterprise value of Rm 1.84B loh!

I think eventually Insas will eventually move above Rm 3.00 to Rm 4.00 loh!

2024-01-16 08:44

Bullish

Hi KC, is KPS considered undervalued as well?

I don't follow this stock and have no positive comments about the management. It supposed to have a big pile of cash after disposing its water assets inn 2015 but if fell quickly to net debt. Wonder if the money was properly used.

It appears to be cheap with single digit PE, but that was due to large one time gain in investment and foreign exchange gain. Taking that off, which should be, it is very expensive. Just my opinion.

2024-01-16 09:18

insas FOREVER UNDERVALUED, IN FACT undervalue more than 10 years.....lol. what does it tell you then/

2024-01-16 09:43

Insas seems undervalued by net cash/NTA valuation but also need to ask these questions:

1. What is the future prospect? Can next year earnings grow substantially (my standard at least 10%)?

2. How about the free cash flow? Will it grow in the future? + Has it grown higher historically.

3. What is the management planning to do with the extra cash ... return to shareholder? Or invest in new growth busienss? Or invest in efficiency enhancement of existing business?

2024-01-16 10:14

Yes & No loh!

10 yrs ago insas Nta is roughly Rm 1.90 & its EPS is around 13.9 sen with share price 80 sen.

Today Nta is Rm 3.56 & eps is 18 sen with share price Rm 1.20.

Surely a dumb fellow using warren buffet formula will had notice insas wealth has grown by rm 1.66 per share or about 16 sen pa over the 10 yrs loh!

And added back div about roughly 1.5 sen div pa avg your total cash generation from insas is about 17.5 sen pa mah!

If your IRR is 10% pa.....surely base earnings Insas should easily worth Rm 1.75 per share loh!

Remember in 2015, Inari only worth less than Rm 1 billion loh but today it is worth more than Rm 12B mah!

Also we have not factor in the hidden reserve of Inari mark to mkt gain for insas holding of about rm 1.6b which is additional gain of rm 2.42 per share for insas loh!

Thus Insas shareholder funds plus Inari hidden reserve mark to mkt gain will contribute potential wealth of Rm 6.00 per share to insas loh!

Surely insas will worth much more than Rm 1.20 loh!

Posted by paperplane > 54 minutes ago | Report Abuse

insas FOREVER UNDERVALUED, IN FACT undervalue more than 10 years.....lol. what does it tell you then/

2024-01-16 10:58

Is Insas KCChongnz only promoted counter? How about Pintaras Jaya, Coastal Contract and many others?

2024-01-16 11:04

Kingkkk,

This type of intelligent question is applicable when u want to buy Nestle at rm 120.00 per share, n its eps is rm 2.80 & nta is only Rm 3.00.

U r trying to justify why u willing to pay so much more loh ?

In insas case u r paying only Rm 1.20 per share to buy a wealth of Rm 6.00 per share mah!

This an obvious no brainer....the answer is obvious loh!

Posted by KingKKK > 48 minutes ago | Report Abuse

Insas seems undervalued by net cash/NTA valuation but also need to ask these questions:

1. What is the future prospect? Can next year earnings grow substantially (my standard at least 10%)?

2. How about the free cash flow? Will it grow in the future? + Has it grown higher historically.

3. What is the management planning to do with the extra cash ... return to shareholder? Or invest in new growth busienss? Or invest in efficiency enhancement of existing business?

2024-01-16 11:09

if you don't book your profit, someone else will ;)

SCIB - limit down

imaspro - multople limit down

ynh

rapid

etc etc

2024-01-16 15:35

to make BIG money in stocks is not easy.

WHY? bcos

msia is a poor country.

KLCI only increased abt 25% from the high of 1297 pts of 1997 to now < 1500

all in 27 yrs or 3 decades!

BUT

there r 5 to 8 stocks that will super bullrun p.a.

can u catch them all at that cycle?

2024-01-17 18:03

Lets put it this way loh!

Today we have almost 5 stocks today that had shown large limit down for the past 5 days loh!

That are :

1. Rapid Rm 3.96 v highest rm 29.54

2 YNH Rm 1.22 v highest Rm 5,20

3. SCIB Rm 0.535 v Rm 1,20

4. Mercury Rm 0.455 v Rm 0.9

5. Imaspro Rm 1.23 v Rm 6.00

A simple financial check will indicates all these are not supported by strong fundamental financial matrix of namely NTA, PE, DIV, ROE, Growth despite had been goreng up sky high loh!

It finanally collapse loh!

If u compare all these 5 stocks...fundamental perform poorly v INSAS loh!

The the reasons why INSAS share has big upside and sustained at current high level, whereas the 5 loser stocks, Raider mentioned fell like 10 pins loh!

The current mkt run up are mainly supported by strong fundamental like Insas, Kseng & OSK that surge strongly beside having good earnings & good strong balance sheets, it has very good sustainable fundamental loh!

Investors are advise to be wary of high speculative stocks & peg their investment that can be supported by good margin of safety like very good pick insas mah!

2024-01-17 19:54

Remember this loh!

Upside of Insas is not value trap mah!

But it is investors price discovery of the good enormous value insas which rerate its share upward mah!

In fact as more people discover the value of insas, which be much higher, it will go up higher & higher loh!

Tong Kooi Ong a tycoon had value insas at Rm 4.33 per share mah!

2024-01-22 20:36

Alot of Insas value investors sifu after holding so long have dispose a sizeable of their holdings, R they right in disposing so soon leh ?

Ans; As a value investor selling so soon is wrong loh! As our master sifu Tong Kooi Ong had indicated a conservative fair value of Rm 4.33, thus selling at Rm 1.30 & below is a wrong decision loh! Surely u can safely hold on insas longer & sell it at 50% fair value that is roughly Rm 2.15 per share mah!

The only justifications of selling insas prematurely at Rm 1.30 & below is just to buy insurance loh! In which alot of sellers did that loh!

But after selling enough to buy adequate insurance, it is time u hang on to your remaining insas for higher target above Rm 2.15 loh!

Forget of all the naysayers shouting value traps lah! This lah! That lah!

Just have convictions & believe in the proven facts that insas worth alot of monies above Rm 4.33 loh!

Thats how value investors become damn rich loh!

2024-01-23 07:59

Whether u r an investor, speculator or gambler....u must learn from this Good Song by Kenny Rogers loh!

If u gonna to play the game, u gotta learn to play it right.

"U got to know when to hold them.

Know when to fold them.

Know when to walk away

Know when to run

Know when to runaway

Know when to keep

Cause every hand is a winner

And every hand is a loser"

For investor the emergence of prominent tycoon investor Tong Kooi Ong n his valuation of Insas Rm 4.33 is an indication of Insas fair value , is a sign u should keep insas & not to runaway loh!

Lu tau boh ?!

Posted by Sslee > 19 minutes ago | Report Abuse

The only reason to buy or sell is to make money. Else why are you in Bursa the biggest casino in Malaysia

2024-01-23 10:09

On what occasion should Insas be value at around Rm 7.00 to Rm 10.00 leh ?

When there is a hostile sizeable investors coming in loh!

Sizeable means investors willing to buy more than 20% of insas share & to be a business partner to Thong loh!

Who r the sizeable partner willing to fork up so much monies of more than Rm 250m just to buy 20% of insas leh ??

It should be a value investors who understand Insas type of business n a good fit is Edge Tong & his allies loh!

It could Raider & Gangs with support of Tycoon behind the scene supporting & financing the deals loh!

Base on raider & gang matrix , the big investors is accumulating big in insas at rm 1.26 and warrants Rm 0.45, the funds require purchase 20% exposure will be Rm 250m loh!

This work out to a cost of roughly Rm 1.80 per share compare to the potential intrinsic value of insas Rm 7.00 to Rm 10.00 loh!

Thus minority shareholders should expect big volume of insas will be traded everyday from rm 1.26 to rm 1.80 over the next 6 mths loh!

Beyond 6 mths after this insas should be flying from Rm 1.80 towards Rm 10.00 loh!

Thus get ready to board the plane loh!

2024-01-27 11:53

The story of Ahfah a successful Pudu mkt vegetable seller, making big in her Insas & insas-w loh!

Ahfah had been holding more than 400k of insas at average cost at 75 sen and warrant 450k at average cost at 25 sen for more than 3 yrs had hit jackpot recently loh!

She had followed raider & gang buying into insas & she has faith to hang tight not only bcos, she trust raider but her deep believe in the good financial figure of insas never lies loh!

Her long patiencely wait for insas certainly payoff loh! Despite Insas broke out above high of Rm 1.00, she did not sold a lot of insas, bcos like raider she believe in insas will worth much more given time loh!

Not many of her peers in pudu mkt is successful bcos many do not have the patience to hold tight & easily jolted to sell when insas share price came down loh!

For example her best friend ahmoi follow her to buy Insas 300k at 80 sen.....immediately sold down, when insas when hit 90sen to Rm 1.00 loh!

Luckily due to her best friend scolding for selling insas too early....Ahmoi still manage to hold back 100k of precious Insas loh!

Ahmoi says i swear to God, that i will not sell anymore of insas, if it is still below rm 3.00 or unless ahfah start selling loh!

The Pudu mkt is active loh.....beside people buying vegetables....alot of them are talking about insas share loh!

Alot of people want to buy insas, but they are afraid bcos the price has risen loh!

Not many people are so lucky like ahfah sitting on big gain of insas without selling loh!

2024-01-27 12:32

Many prominent value investors value insas differently loh!

1. Sifu Sslee Target Rm 1.50.

2. Insas Eps 18.2 @ pe 12x = Rm 2.20.

3.Ahmoi the best friend of Ahfah in Pasar Pudu Rm 3.00.

4. Nta of insas exclude all the potential hidden gain Rm 3.56

5. Ahfah the investment queen in pasar Pudu Rm 3.90 to Rm 4.80

6. Tong Kooi Ong of Edge Rm 4.33

7. Leno Rm 6.00 and Rm60.00

8. General Raider Rm 7.00 to Rm 8.00

People always think of getting or hoping a new major shareholder, unlocking the hidden value of insas loh!

The truth is Thong is quietly unlocking value stealthly without people noticing mah!

Once people realized this.....there will be chasing Insas above Rm 3.00 loh!

Lu tau boh ah ???

" Insas strength is a very strong incubator of business loh!"

Thats why u have Inari, M&A in respect of Insas & Microlink in respect of Omesti loh!

All these private equity type of business had contributed billions of profit to insas mah!

In fact Insas is a msia equivalent of Black Rock & Goldman Sachs of the USA loh!

"The story of Ahfah a successful Pudu mkt vegetable seller, making big in her Insas & insas-w loh!

Ahfah had been holding more than 400k of insas at average cost at 75 sen and warrant 450k at average cost at 25 sen for more than 3 yrs had hit jackpot recently loh!

She had followed raider & gang buying into insas & she has faith to hang tight not only bcos, she trust raider but her deep believe in the good financial figure of insas never lies loh!

Her long patiencely wait for insas certainly payoff loh! Despite Insas broke out above high of Rm 1.00, she did not sold a lot of insas, bcos like raider she believe in insas will worth much more given time loh!

Not many of her peers in pudu mkt is successful bcos many do not have the patience to hold tight & easily jolted to sell when insas share price came down loh!

For example her best friend ahmoi follow her to buy Insas 300k at 80 sen.....immediately sold down, when insas when hit 90sen to Rm 1.00 loh!

Luckily due to her best friend scolding for selling insas too early....Ahmoi still manage to hold back 100k of precious Insas loh!

Ahmoi says i swear to God, that i will not sell anymore of insas, if it is still below rm 3.00 or unless ahfah start selling loh!

The Pudu mkt is active loh.....beside people buying vegetables....alot of them are talking about insas share loh!

Alot of people want to buy insas, but they are afraid bcos the price has risen loh!

Not many people are so lucky like ahfah sitting on big gain of insas without selling loh!"

Raider answer to the dilema of Ahfah & his followers is to get your bearing of investment valuation of Insas Right mah!

With proper valuation of Insas you are not afraid n confident to hold on to Insas loh!

2024-01-27 17:56

Below advice given by contrarian is a slow way 3rd world method of accumulation of substantial wealth loh! In which General Raider see this is not that efficient loh!

If u think Insas is going to move up to Rm 1.50 to Rm 2.00 soon, & u know Insas should be worth at least Rm 4.33 base on Edge Tong conservative valuation n in which insas has huge margin of safety loh! There r better way loh!

What u should do is allocate substantial resources to insas in order to get rich safely & steadily loh!

The correct approach for insas are as follows loh!

1. Allocate substantial investable assets into insas, say u have Rm 1m.....u must invest at least 30% @ Rm 300k into Insas loh!

2. Allocate substantial of your future saving by investing insas more loh! For example U n your wife earn Rm 20k a month & u can save Rm 6k a mth...........thus u should invest in insas Rm 18k every 3 mths loh!

Raider suggest this Rm 18k is a comparative smaller sum, thus u should allocate this savings fund just for investing in insas-w to maximise exposure loh!

Having done that, u will on the route of great wealth loh!

But u must monitor Insas share price to ensure that u have adequate margin of safety loh....Raider suggest u stop putting more money into insas when it hit above Rm 3.20 mah!

And u may consider sell a small % of insas slowly when it trade above Rm 3.80 loh!

The above r the right way of investing in insas & raider follower ahfah the queen of investment in Pasar Pudu adopt this method & gain substantial wealth without taking excessive risk loh!

Ahfah proudly tell his fellow vegetable sellers this loh!:

"I have make about Rm 200k profit just investing in insas & its warrant within 3 mths loh! Just imagine how much i need to sell vegetables, if i make rm 1 per kg from vegetable, that will be 200,000 kg or 200 tonnes loh!"

"Good share management & investment tech is very important if we want to accumulate substantial wealth sustainably & i would like to thank General Raider for that mah!"

Posted by TheContrarian > 3 minutes ago | Report Abuse

If you buy 10,000 shares at 60 sen, sells all at RM1.10 your original RM6,000 becomes RM11,000 and with that amount you can later buy back say, 15,000 shares at around 70 sen. Then sell the 15,000 shares at RM1.20 to get RM18,000. Later when price drops back to say, 80 sen, you can buy 22,500 shares.

2024-01-28 10:18

4 folds in less than 1 year ? Supere.

@Posted by TheContrarian > 14 hours ago | Report Abuse

Already made 4 fold gain on Insas, hahahahaha

2024-01-29 15:33

Correct loh.....this point to sitting on insas will be long run more beneficial as a way of growing your wealth loh!

Posted by Integrity. Intelligent. Industrious. 3iii (iiinvestsmart)$â¬Â£Â¥ > 1 day ago | Report Abuse

General trading: anticipating moves in the market as a whole.

Selective trading: picking out stocks which will do better than the market in the short term.

Benjamin Graham warned what NOT to do. He did not consider that either general trading or selective trading has any place in investment practice. Both of them are essentially *speculative* in character because they depend for success not only on the ability to foretell specifically what is going to happen, but on the ability also to do this more cleverly than a host of competitors in the field.

The real money in investing will have to be made - as most of it has been in the past - not out of buying and selling, but out of OWNING AND HOLDING securities, receiving interest and dividends, and benefiting from their long-term increase in value.

2024-02-01 12:42

Post a Comment

Featured Posts

Latest Videos

.png)

MQ Trading Signals

Time

Signal

Duration

Type

2024-08-27 15:30:00

EMA 5

5 Mins

SELL

2024-08-27 15:30:00

MACD/RSI

5 Mins

SELL

2024-08-27 15:25:00

ADX

5 Mins

SELL

2024-08-27 12:00:00

EMA 5

5 Mins

BUY

2024-08-27 11:55:00

ADX

5 Mins

BUY

Apps

Top Articles

1

Koon Yew Yin's Blog

3

Koon Yew Yin's Blog

4

Stock Market Enthusiast

PBBANK: Technical Outlook Suggest Target of RM5 (Uptrend but Overbought) - KingKKK

5

6

Koon Yew Yin's Blog

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

Welcome back to i3 forum

Long time no see

2024-01-15 23:24