Koon Yew Yin's Blog

Plantation stocks comparison update - Koon Yew Yin

Koon Yew Yin

Publish date: Tue, 19 Apr 2022, 07:08 AM

Koon Yew Yin

0 1,454

An official blog in i3investor to publish sharing by Mr. Koon Yew Yin.

All materials published here are prepared by Mr. Koon Yew Yin

All materials published here are prepared by Mr. Koon Yew Yin

Due to the historical record high price of CPO, all plantation companies have been reporting increased profit and will continue to report increased profit for the next few quarters. As a result, all plantation stock prices have been going up higher and higher. Investors should study the comparison based on historical PE and Market cap per planted hectare to know which are the better stocks to buy.

Comparison based on historical PE

|

Name |

Price Rm |

Latest EPS |

Latest EPS X4 |

Price ÷EPS X4 |

|

Subur |

2.20 |

16.15 |

64.6 |

3.4 |

|

Cepat |

1.14 |

7.74 |

31.0 |

3.4 |

|

SOP |

6.32 |

36.44 |

Rm1.56 |

4.1 |

|

Jaya Tiasa |

1.09 |

5.28 |

21.12 |

5.2 |

|

Sarawak Pl |

2.90 |

11.66 |

46.6 |

6.2 |

|

Hap Seng |

2.49 |

11.79 |

47.2 |

6.3 |

|

Ta Ann |

5.59 |

21.8 |

82.2 |

6.4 |

Comparison based on Market cap ÷ planted Hectare

|

Name |

Price Rm |

Market Cap Million |

Hectare |

MC÷Ha |

|

Subur |

2.20 |

460 |

44,000 |

10.5 |

|

Jaya Tiasa |

1.09 |

1,062 |

70,000 |

15.2 |

|

SarawakPl |

2.90 |

812 |

35,000 |

23.0 |

|

Cepat |

1.14 |

360 |

10,000 |

36.0 |

|

SOP |

6.20 |

3,580 |

88,000 |

40.6 |

|

Ta Ann |

5.94 |

2,642 |

50,000 |

52.8 |

|

Hap Seng |

3.05 |

2,392 |

35,000 |

67.0 |

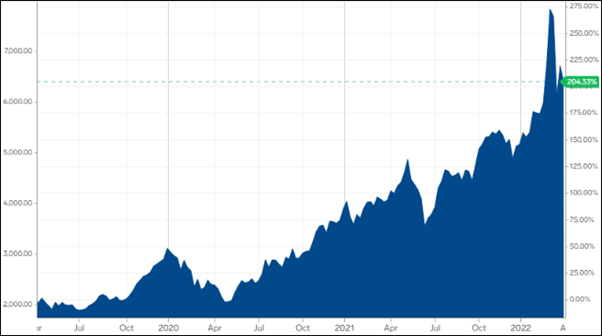

The CPO price chart below shows that CPO price started to go up from Rm 2,500 per ton about 2 years ago to peak at above Rm 7,000 per ton. CPO price has been around Rm 2,500 per ton for many years.

Due to the Ukraine -Russia conflict all food prices have gone up. Moreover, the Indonesian Government export restriction to reserve 20% to help local consumers, CPO high price will remain.

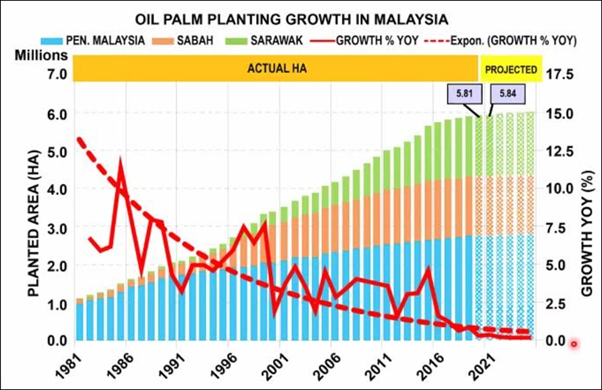

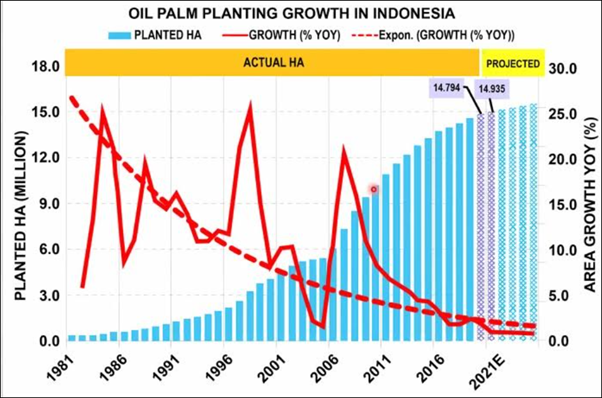

Investors should study the 2 charts below.

As agricultural land becomes limited, oil palm replanting is key to boosting palm oil yield across Indonesia and Malaysia. It is important replant to sustain supply because Indonesia and Malaysia produce about 85% of the world’s palm oil need.

Due to land shortage, plantation companies with larger planted acreage is a very important consideration for investors.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Koon Yew Yin's Blog

Plantation stocks comparison - Koon Yew Yin

Created by Koon Yew Yin | Dec 26, 2024

Indonesia is the biggest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offi..

All plantation companies will report historical record profit - Koon Yew Yin

Created by Koon Yew Yin | Dec 13, 2024

Indonesia remains committed to start implementing a 40% mandatory biodiesel mix with palm oil-based fuel, or B40, on Jan 1 next year, its chief economic minister said. Indonesia, the world's largest..

Who buys palm oil - Koon Yew Yin

Created by Koon Yew Yin | Dec 12, 2024

Indonesia is the world's largest producer of palm oil, producing an estimated 46 million metric tons in the 2022/23 marketing year. Indonesia also exports over 58% of its production, making it the w..

TH Plant is the best buy - Koon Yew Yin

Created by Koon Yew Yin | Dec 03, 2024

Indonesia is the largest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offi..

What is Bipolar Disorder? - Koon Yew Yin

Created by Koon Yew Yin | Nov 25, 2024

My younger brother who was a dentist had bipolar disorder. Unfortunately, he committed suicide about 12 years ago.

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

Created by Koon Yew Yin | Nov 22, 2024

All plantation companies are reporting better profit for the quarter ending September when CPO price was about RM 3,800 per ton.

MHC Reported Increased Profit - Koon Yew Yin

Created by Koon Yew Yin | Nov 21, 2024

Indonesia is the biggest palm oil producer in the world. Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry offici

Why all plantation companies will continue to report more profit - Koon Yew Yin

Created by Koon Yew Yin | Nov 20, 2024

Indonesia plans to implement biodiesel with a mandatory 40% blend of palm oil-based fuel from Jan. 1 next year, a senior energy ministry official said recently, lifting prices of the vegetable oil...

Who will win the Presidential Election? - Koon Yew Yin

Created by Koon Yew Yin | Oct 30, 2024

Latest poll on 30th Oct 2024

Who will win the Presidential Election? - Koon Yew Yin

Created by Koon Yew Yin | Oct 30, 2024

Latest poll on 30th Oct 2024

Discussions

2 people like this. Showing 40 of 40 comments

Cost of cpo production can no longer maintain at rm1600 per ton because of high fertilizer price and minimum wage. But then the increase of cost is still no way match the increase of cpo price. So even if production cost raises to rm2000 per ton, Palm oils company still can generate huge profit that no one ever seen before.

It is a no brainer to buy palm oil stock that has plenty of lands to hedge against inflation, somemore these lands able to generate huge cash flow.

2022-04-19 14:47

Noticed Cepat and MHC Plantation is not mentioned. Also curious as to how Plantation Companies are taxed - Excess profit Tax when CPO price over Rm3500? Windfall Tax when annual profit above RM 100 million, and normal Tax of 24 % on Net Profit.

2022-04-19 20:47

Based on the latest financial reports, in fact MHC and Cepat are the most undervalued at current share price.

2022-04-20 05:45

Based on the latest financial reports, in fact MHC and Cepat are the most undervalued plantations stocks at current share price.

2022-04-20 05:46

Should change 'M.Cap/Ha' to '(M.Cap+T.Debt-C.Asset)/Ha'.

If your dun know the management very well, dun buy those small companies that pay very little dividend.

2022-04-20 07:47

calvin tan koresh, you are really a thick skinned arrogant c.... Who made u god to decide what is right or wrong? u think u god ah? u make money no need to brag. Other people got their point of views...not for u to judge and say who is right or wrong.

2022-04-20 08:59

@Calvin

Get your facts right!

"Because Mhc plant palm oil estates are mostly located in Telok Anson

Those lands are swampy and so quite useless "

Where u think Utd Plt lands are ?They have highest CPO per hectare in whole Malaysia.

2022-04-20 09:37

@Calvin, I visited Utd Plt estates for 16 years. So many orang putih have visited this estate!!!! Useless, say you???!!!!

2022-04-20 09:56

I think Calvin meant Utd Plt estates in TI are peat soil and no good for housing development ;not that they are no good for oil palm (or coconut). Utd Plt manage their estates efficiently and treat their workers very well. Their little bakery selling delicious bread and bakery products at TI estate is a must visit every time I pass by that area.

2022-04-20 10:15

hahaha

I bought mhc plant at 46 sen and sold for over 100% profit to buy Tsh resources

Tsh resources will make 1,000% profit

2022-04-20 11:45

No doubt the CPO price now will bring windfall to all oil palm plantation owners, big or small, but the cost of production had also gone way up. Cost at RM1600 was way back at least 10 years ago, even in those days it can be up to Rm2300 for the less efficient producers. Do not go into just any oil palm company blindly.. try to understand their management properly.

Few points all of us must take note:

1. Does the company shares their bumper profit with their share holders.. do they have the nasty attitude of socialise when losing and privatise when making.. such companies are only for punters.. hit and run.

2. With such unprecedented price, a lot of big players are selling forward since the CPO was at around RM4000.. these big players seldom tell share holders how much of their stock(future) already committed at much lower price.. especially those developing ones, they care about stability and commitment for debt and full development of their land.

3. Even worse if company sold forward but a huge percentage of their FFB is not their own but small holders in their vicinity. These small holders will be given average 'spot price' on the month they deliver.. with price going up, these companies(taking outside FFB) will lose money. Generally, this is reflected in their quarterly financial statement that the revenue is huge compare to the size of plantation.

GOOD LUCK

2022-04-20 12:07

@joerakmo and william wang....good points brought up. That's what a good discussion should be, balanced and fair. Unlike the brother of david koresh who goes around trying to brainwash i3 readers

2022-04-20 12:33

Lu tau boh ??

Cost of production now is Rm 2200 to Rm 2400.....but every type of other planted competing commodities are already up mah!

Thus the Rm 4000 should be sustainable even if cpo price correct loh!

Yes owner sell fwd....bcos they do not believe cpo can go above Rm 4,000 bcos previously this is the record price loh!

Even if owner sell fwd at Rm 4,000 and now it is at above rm 6,000.....the owner still make more money bcos the previous avg was rm 3200 which already consider lucrative mah!

Now at above rm 6,000 the plantation still make money....base on selling price of Rm 4000 loh!

Companies take outside FFB still make money....bcos normally the conversion Gross margin from FFB to CPO.....is around 15% to 20% mah!

The crusher mills should make monies mah! If cannot make monies why take up the FFB leh?

2022-04-20 12:42

Hi Calvintaneng , what you said about MHC’s land in Telok Anson are swampy and useless is UNTRUE!

You liquidated MHC around $1.08 many months ago was simply because

Mr Chan Kam Leong , a director who hold insignificant amount of share ,was selling down .

MHC’s about 7,600 acres 0f lands are in Durien Sebatang, chankat Jong and hutan melintang are planted and generating revenue . Some of these lands are freehold and with good development value .

The biggest assets of MHC is the investment in cepatwawasan.

2022-04-20 13:44

Now I know why he wrote 'MHC was cheap'. That could be also meant by him that it is expensive now.

2022-04-20 14:10

Correctloh....MHC has plantation estate near TG malim & slim river.....quality land near development area....easily converted to industrial, commercial and residential area...a big potential for mixed development projects loh!

2022-04-20 19:11

Bought into MHC because of their "ownership" of Cepat Wawasan. Plus Cepatwawasan has significant "under Valued" land/plantations.

2022-04-20 19:59

yeah MHC owns 29% of cepat. This shares alone already worth 106mil, which is 40% of MHC's market cap.

2022-04-20 21:19

The company is not generous in giving out dividend like Innoprise and Kmloong. That maybe the reason it is lagging behind the two. Note that Kmloong latest QR, its EPS is 3.27c only even CPO average price was above RM5,000 in that quarter.

2022-04-20 21:31

amazingly ommited out the single most important palm oil counter in the calculations..... KLK, it may not just up 100% but surely its the sturdeast and strongest of all if ever there was a downturn

2022-04-21 04:08

Calvin, I would say most of the plantation companies do not know what they doing. They have no idea what efficiency mean.

Years ago, I looked at TSH, they say they are using new clones (A, B mixed with clones), that is going to be 50% more productive. The production figures just doesn't add up. (I have some A, B, C, D, but that's not relevant lah). I would say they are slightly better off but not up to 50%.

Its a simple multiplier effect. If you have a big tree that have more leaves and higher percentage of female branches, plus bigger bunches, then you have more yield.

Most companies just do not care, they just have too little ffb and let half of them rot on the tree. (because they do not maintain the roads and plan properly, its difficult to harvest by then).

If you are in west malaysia or sarawak, the soil is so poor and hardly any fruits to be seen.

Its annoying to see people just divide the land area.....

come one, its 2022, learn efficiency.

2022-04-21 06:34

Klk or Uplant can only buy in bad times for dividend and not now

Why?

They say in bad times buy good stocks and avoid bad stocks

But in boom times like now you don't buy good stocks but better buy bad stocks

Why like that?

answer:

if bad times 2nd and 3rd liners will drop a lot

in bad times good stocks still pay dividends cannot drop much so price not cheap

In bad times 3rd liners can collapse by 60% to 80%

So in good times good blue chip still holding firm also CANNOT MAKE MUCH MONEY

WHEREAS IN GOOD TIMES THOSE BOMBED OUT 3RD LINERS VERY CHEAP CAN GO UP 300% TO 500%

IT TAKES LONG EXPERIENCE AND REAL KNOWLEDGE TO KNOW THIS TRUTH

THAT IS WHY WE DON'T ADVOCATE BUYING KLK AND UPLANT NOW

THEN?

THEN GO FOR THESE

JTIASA

BPLANT

THPLANT

TSH RESOURCES

ABOVE 4 WILL OUTPERFORM ALL OTHERS

2022-04-21 15:21

Thanks for your comments Calvin. So far only bought 3 of the above in small amount, except THPlant. From observation, TaAnn is very good, as it is constantly on the move up and second is HSPlantation which went up after buying within a short time. Seems IOI Corp is responsive to CPO price movement but its price is lagging compared to others. SHChan is also a laggard.

2022-04-21 17:15

Personally i prefer those plantation stocks with small cap but still making money at least 4 consecutive quarters.

Chances that they double or triple in market cap is much higher but with relatively small risk.

2022-04-21 18:05

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

2

3

4

Koon Yew Yin's Blog

5

THE INVESTMENT APPROACH OF CALVIN TAN

6

M+ Online Research Articles

7

TA Sector Research

8

Mercury Securities Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

Post removed.Why?

2022-04-19 13:43