Davidtslim sharing

DAYANG: My Analysis on Dayang (Davidtslim)

1. DAYANG is one of the largest providers of offshore platform services in Malaysia. It is principally involved in the provision of offshore Topside Maintenance Services (TMS), minor fabrication operations, offshore hook-up and commissioning, and charter of marine vessels relating to the oil and gas companies (like Petronas etc).

2. It owns a fleet of 9 offshore support vessels (excluding subsidiary Perdana's young fleet of 17 vessels). The vessels are known as Dayang Pertama, Dayang Maju, Dayang Cempaka, Dayang Berlian, Dayang Nilam, Dayang Zamrud, Dayang Topaz and Dayang Opal. As at the end of December 2018, its total orderbook stood at RM3.0 billion; which can last at least until 2023.

3. DAYANG delivered the highest ever revenue and earnings in 4Q18 quarter, on the back of a revenue improvement of 64.9%, a reversal of impairment loss on PPE amounting to RM20.8m and forex gain of RM15.4m. Core earnings in 4Q18 was about RM80m as compared to an adjusted loss of RM33.6m in 4Q17.

4. The surge in revenue in 4Q18 was driven by much higher lump sum order and vessel utilization rate of 73% (vs 4Q17: 51%). In FY18, due to lower debt as compared to FY17, lead to lower net finance costs (-13.6%), Dayang made a profit turnaround of RM164.2m (EPS 17.02 sen) in FY18.

5. In view of the substantial pick-up in the work orders in the last three quarters of FY18, the management is optimistic that the strong earnings trend would be sustainable in FY19, on the back of strong contract execution track records, high profit margin and 3 billion orderbooks.

6. A few recent Investment banks reports saying Dayang recent quarter strong performance may not be sustainable due to lump sum orders may not repeatable. However, let me share with you an interesting excerpt from Hong Leong’s Dayang research report as below:

Source: HLB Dayang’s report (page 1)

It is stated that Dayang is expected to receive additional lump sum orders from clients in their meeting with management. Actually Dayang has been recorded lump sum revenues for 2017 and 2018 which were 251 millions and 473 millions respectively.

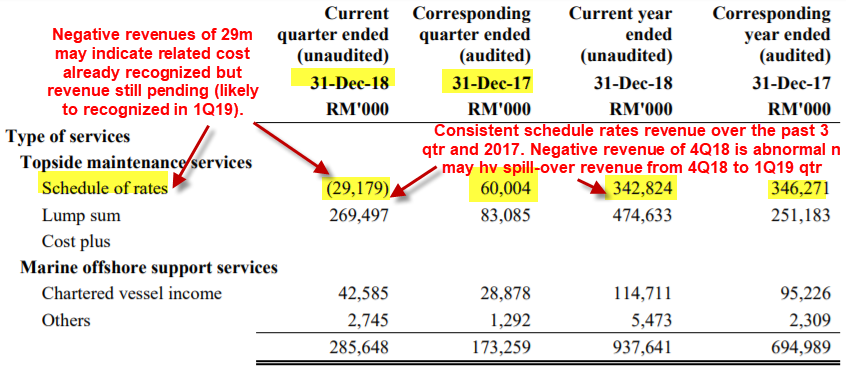

Another more interesting fact from last qtr report (Q4) of Dayang is the missing of schedule rates revenue which is likely to book or surface in coming quarter result. Let see the extract from Dayang last quarter report on its schedule rate revenue as below:

Source: Dayang 4Q18 report (page 18)

Negative revenues of schedule rates of TMS division may due to related cost already recognized but revenue still pending or not yet recognized. If this leftover schedule rate revenue can be recognized in 1Q19, then profit margin may be even higher than conventional quarter due to related cost already recognized or booked.

The schedule rates revenue for 2017 and 2018 were 346 mil and 371 mil respectively (total of Q1,Q2 and Q3 revenues but exclude Q4). This average schedule rates revenue over the past 3 quarter about 123mil, thus, I estimate the possible leftover schedule rates revenue could be around 120 mil+. Don’t forget there is also normal schedule rate revenue in 1Q19 which may make double or exceptional higher schedule rate revenue in 1Q19 (normal + leftover from 4Q18).

Even assuming high lump sum revenue or profit may not sustainable in 1Q19 (estimated to drop 50-60%), the leftover schedule rate revenues from 4Q18 may be enough to cover the revenue of lump sum orders. Besides, according to HLB report (guidance from management), there are some variation orders have been carried out but not yet reflected in their revenue (pending client approval).

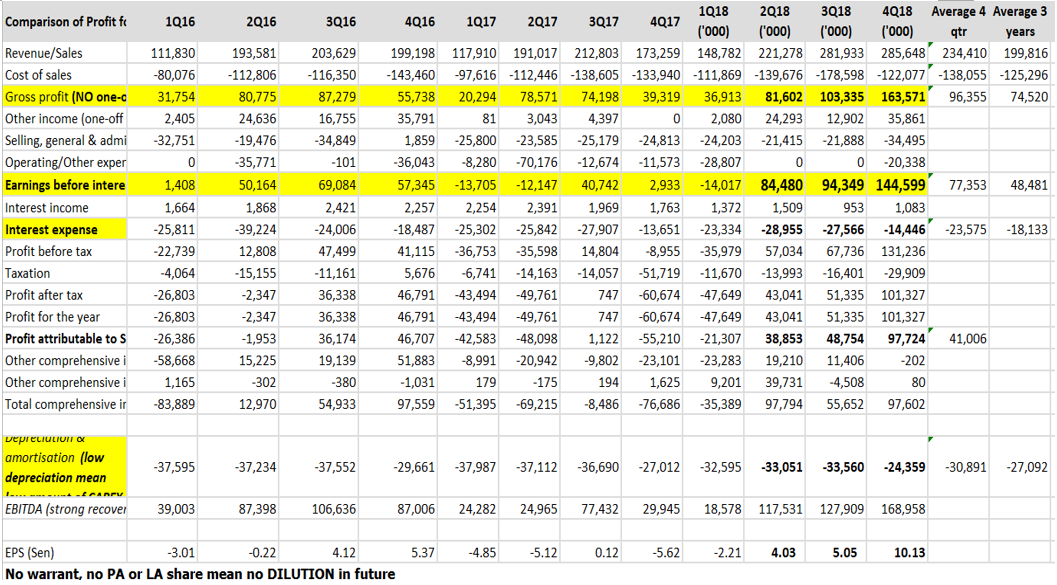

7. One of the metrics to evaluate the earning capability of a company is by looking at its gross profit margin and general & admin expenses. The table below shows the gross profit (no one-off profit) and admin expenses of Dayang in the past 3 years.

We can see dayang has achieved impressive gross margin and keep admin expenses low in the recent 3 quarter on the rising revenue trend. This leads to higher Ebit (earning before interest and tax) and resulting in higher net profit in recent 3 qtr.

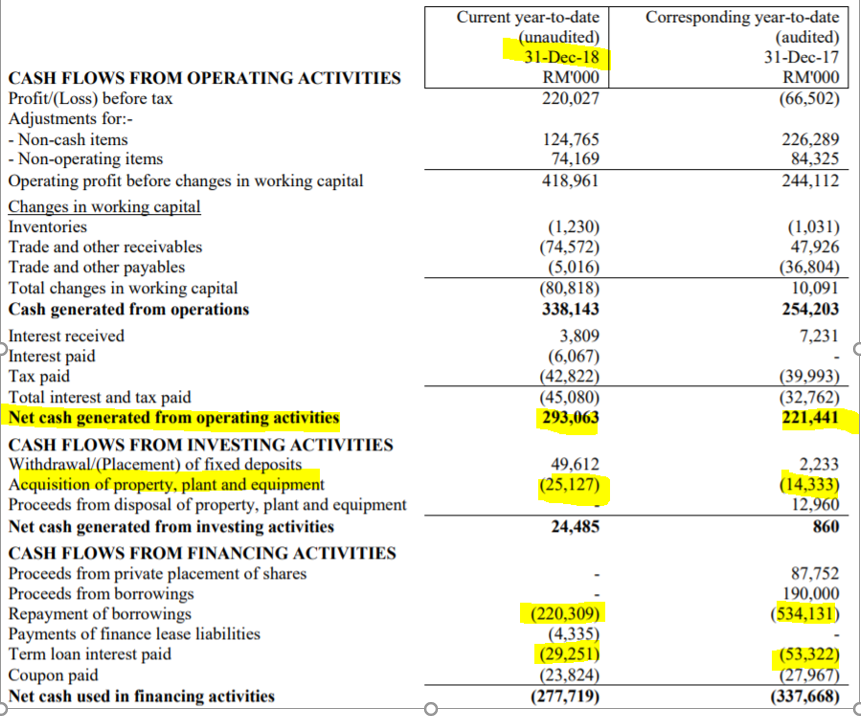

8. High quality of earning. Cash flow from operation is a metric to evaluate quality of earning of a company. Let see the cash flow from operation of Dayang as below:

Source: 4Q18 report

Dayang has generated 293mil cash from operation with an 25 mil capex spent on PPE (property, plant and equipment) in FY2018. In addition, Dayang has paid off about 250mil of borrowings in 2018.

9. Improving balance sheet due to strong cash from operation. Dayang has paid off more than 550 mil debt over the past 3 years (net debt reducing from 1.56B to 0.86B) from the impressive free cash flow as shown in table below:

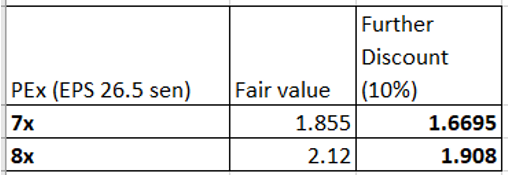

10. Attractive Valuation - Achieved net profit of RM97 million last quarter. Exclude one-off earnings (reversal of impairment), adjusted net profit about RM80 mil. Annualize = 320mil, discount 20%, discounted annualized profit = 256mil --> Estimated FY19 EPS = 26.5 sen. Fair value of Dayang can be summarized on the table below:

The first 20% discount is due to this EPS estimation is based on highest quarter profit and there is a possibility that coming quarter may not achieve the similar high earning (maybe due to previous qtr result has big lump sum which may not sustaianble in 2018).

The second 10% discount is due to there is a possibility that Dayang may propose private placement due to good share price to raise some fund to prepare for Perdana Bhd coming right issue fund raising. The maximum private placement (pp) is up to 10% where this pp can cause dilution of EPS up to 10%.

Why Dayang should worth PE of 7-8x? Below are the justifications for this valuation:

- Strong and Stable Margins - Average Gross Profit margin of above 35% and Net Profit margin of above 15%, one of the most efficient O&G service providers among all.

- Proven track records of project execution with good profit and never fall into operation loss over the past 7 years (except in 2016 & 2017 due to non-cash big impairment from subsidiary Perdana Bhd, impairment is not belong to operation loss)

- Strong orderbook of 3 billion and good profit visibility for the next 3-4 years as Dayang has shown improving profit for last 3 quarters.

- Strong cash flow generation over the past 3 years and pare down debt of 700 mil in 3 years.

Another valuation method is using Discounted Cash Flow (DCF). Based on past 3 years records on average cash flow generation of 294 mil, let's assume the average cash generated per year in future is 250 million (~10-20% discount), the discounted cash flow per share per year is about 26 sen. If this strong cash flow generation trend can continue for 3-5 years (based on strong 3B orderbook and higher rig operation counts from Petronas), the cash generated per share over 5 years could reach RM1.30 per share. Over long run of 10 years, the cash per share could reach RM2.6 using DCF method with some discount.

11. Contract awards secured by Dayang and Perdana from international clients (not only from Petronas) as table below:

|

Date secured |

Effective date |

Types of works |

Client |

|

Sept 2017 |

5-yr contract, effective from 20/9/17 |

Maintenance, construction and modification Services Package A (Offshore) |

PETRONAS Carigali Sdn Bhd |

|

Aug 2018 |

5-yr contracts effective from 17/7/18 - 16/7/23 |

provision of Pan Malaysia Maintenance, Construction and Modification (PM-MCM) |

JX Nippon Oil & Gas Exploration (M) and Repsol Oil & Gas Malaysia Limited |

|

Oct 2016 by DAYANG's 60%-owned subsidiary, Perdana Petroleum |

3-yr contract worth RM67m effective from Sept/2018 - 2019 |

to supply one unit of floating accommodation vessel |

Petronas Carigali Sdn Bhd |

|

Nov 2018 |

3-yr subcontract, USD100mil, effective from 1/1/19 - 31/12/21 |

provision of Facilities Maintenance Support in Turkmenistan |

Gujurly Inzener |

11. Let us have a comparison of Oil and Gas related companies in Bursa and SWOT as tables below:

Comparison is not for Public. SWOT analysis is not for Public.

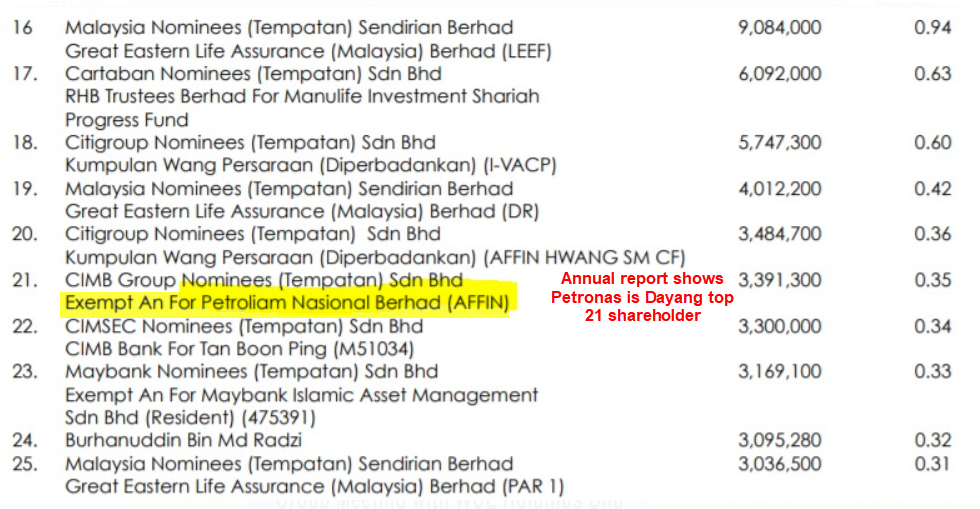

12. Let see the annual report of Dayang and see who is the top 21 shareholder

Source: Annual report 2017

In fact dayang receiving increasing order of lump sum works in 2017 and 2018 from Petronas. One of the reasons I guess is due to 25 years track records and experience of Dayang in MCM in Oil & Gas. Another possible reason maybe due to Petronas may try to take care of Dayang in contract awards due to Dayang's track records and project execution capability. FYI, the schedule rate revenue mainly come from 3B orderbook which is mainly based on call-out basis (refer to their AR). The high gross margin of their lump sum works maybe due to their arrangement of charter vessel by campaign to another campaign and fully utilize them at offshore.

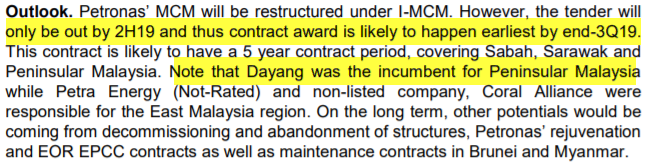

13. Let see the outlook of Dayang from HLB recent report (after their meeting with management) as below:

Source: HLB Dayang report (19 March)

Oil price in 1Q19 and April 2019 remain strong and currently close to USD69 per barrel. Petronas also needs more income in 2019 as they need to pay higher dividend to government of Malaysia. Thus, more oil rig may be in operation that lead to higher maintenance or modification works.

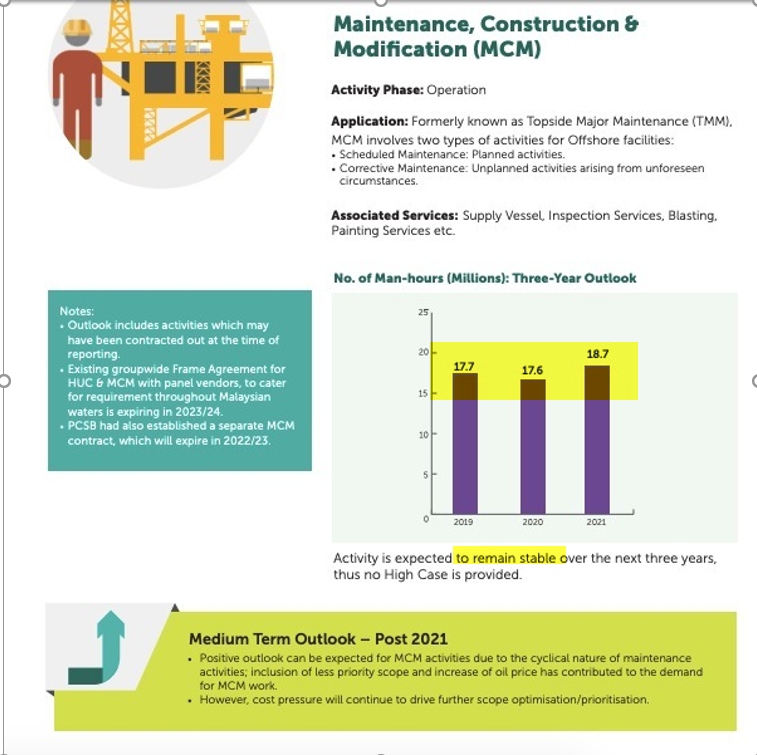

14. Increase of activities in MCM segment in Petronas activity outlook report 2019 to 2021 - Dayang is a direct beneficiary. In the report, “The respective offshore fabrication, linepipes, offshore installation and hook-up & commissioning (HUC)/ maintenance, construction & modification (MCM) segments will also see increase of workflows in 2019-21. Report below shows the MCM activities outlook of Petronas.

If you interested on my analysis report, please contact me at davidlimtsi3@gmail.com

You can get my latest update on share analysis at Telegram Channel ==> https://t.me/davidshare

Disclaimer:

This writing is based on my own assumptions and estimations. It is strictly for sharing purpose, not a buy or sell call of the company.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Davidtslim sharing

LCTITAN: Beneficiary of Strong demands of Packaging, Mask and Glove's raw materials (Davidtslim)

Created by davidtslim | Oct 03, 2020

NOVA: An Expanding Healthcare OBM player with high profit margin (Davidtslim)

Created by davidtslim | Aug 28, 2020

Samchem – Beneficiary of Raw Chemical Material supply to support healthcare industry (Davidtslim)

Created by davidtslim | Aug 06, 2020

Supermax Part 2: Timely Expansion and Increasing ASP (Davidtslim)

Created by davidtslim | Aug 04, 2020

STRAITS (0080): A winner from the structural changes to bunker biz due to IMO2020 (Davidtslim)

Created by davidtslim | May 15, 2019

Discussions

6 people like this. Showing 42 of 42 comments

as such the PE rating should definitely be comparable to Serbadinamik level

no way at 7 or 8 like David had used above

2019-04-05 23:13

Isn't Dayang just doing what serbadinamik is doing on land, but on sea.....

only difference is they have yet to capture overseas market like what serba had done..

2019-04-05 23:21

Alr up like hell...only comw out with tis article.

Why not write about petron at depress price now....lower downaide but higher upaide than dayang.

2019-04-06 00:21

David , good write up .In my opinion, your valuations of Dayang is better than the 3 IBs . Your report cover more details with factual figures than the IBs. You have also consider the outlook of Dayang in longer term rather than just the IB's " next qtr earning is not sustainable " . I am happy that you have also pick up the last qtr "missing " schedule rate revenue which is estimated to be about RM 120 million which in my opinion will be booked in Q1 2019 . In the last 2 weeks , I have commented in bit and pieces in the i3 forum about the missing schedule revenue , the great cash flow of dayang and the brief valuations of dayang using both PE and DCF . I am glad that you have been able to put in nicely in a your write up so that most of the i3 readers can comprehend .

2019-04-06 11:18

The oil and gas bull will continue for all of 2019 and into 2020 for very strong reasons:

1. Petronas Refinery needs extra 54.7 million barrels of oil a year

2. Brent Crude now over USD70 makes it worth while to extract more oil

3. PH Govt still need Petronas Revenue to help Malaysia

After this short rest dayang should firm up.

Only liability is in perdana's debt load

I think Penergy should also play catch up as it has been included in Both phase 1 and phase 2 ogse jobs

And T7 global will also get follow dayang and penergy because Petronas bypass ogse and award jobs directly to Sme support ogse entities

2019-04-06 11:33

An impressive writeup with substance. That's how a proper analysis should be done with facts and figures. The 3 IBs should learn from you. I believe the TP should be easily RM2-3 in 6 months time based on your writeup.

2019-04-06 11:59

Another valuation method is using Discounted Cash Flow (DCF). Based on past 3 years records on average cash flow generation of 294 mil, let's assume the average cash generated per year in future is 250 million (~10-20% discount), the discounted cash flow per share per year is about 26 sen.

...........................

Using above data from David, which takes the average of last 3 years (under depressed market condition), i think we can use PE 10.....to derive TP of 2.60.

reason being i see its depreciation need and maintenance capex would be almost nil going forward.... its assets which are not utilized can be disposed to generate cash....

2019-04-06 12:54

https://klse.i3investor.com/blogs/www.eaglevisioninvest.com/201122.jsp

Buy JTiasa still cheap . Buy low sell high. Forgot about dayang. Already up more than 200% what do you expect ?

https://www.theedgemarkets.com/article/palm-rises-6week-high-stronger-export-outlook

Palm rises to 6-week high on stronger export outlook

2019-04-06 14:39

https://www.forbes.com/asia200/list/#header:country_country:Malaysia

serba is in the list for 2018

2019 will be Dayang (It was on the list in 2014)

2019-04-06 15:29

You're being overly simplistic in your analysis of a highly complex business, in an industry with multiple feedbacks.

Do you remember hengyuan, masteel etc.

How precise your predictions are and how incredible wrong they were?

2019-04-06 15:45

wei..dont delete this post of Jon...

Posted by Choivo Capital > Apr 6, 2019 3:45 PM | Report Abuse

You're being overly simplistic in your analysis of a highly complex business, in an industry with multiple feedbacks.

Do you remember hengyuan, masteel etc.

How precise your predictions are and how incredible wrong they were?

2019-04-06 15:51

Jon dont shoot first !

Risk only come for the blind spot unknown...

Afterall, investment is something we trying to do a set of assumption.

Then, u apply a safety of margin by discounting your calculated TP.

Can you enlighten us here ?

2019-04-06 16:03

Choivo boy you are not contributing shit and now you wanna come out and shoot?

2019-04-06 21:33

Connie, why delete the Evil Or Angel blog? We were busy discussing choivo, 3rd person Calvintaneng, autism, asperger etc

2019-04-06 21:57

choivo ,it will be more constructive if you can objectively point out which parts of David analysis or assumptions are incorrect factually rather than asking a very subjective question on how accurate is his prediction. We will appreciate your comments if you can critique his analysis objectively. We will appreciate more if you can come out with your versions of analysis and prediction.

2019-04-06 22:09

I repost already, out of my heart of sympathy i decided to withdraw it yesterday, however after all seems like he never learn his lesson, so i reposted.

2019-04-06 22:11

Dear pjseow,

Choivo needs to be treated differently, logic does not apply to him as he prefers making comments than acting on stocks in which he has followed kyy and most money on.

Therefore he has stock loss bias, meaning if he loss money on JAKS, no matter how much you may make, he already is opinionated, because while you may start from a neutral point of view, he starts from a negative one.

2019-04-07 06:16

Oil price is going uptrend.... positive news for O&G companies including Dayang, Hibiscus, etc

2019-04-07 09:49

unker probability is right lor! Biggest profit for capital items is made in the after sales service! Just like Rolls Royce mah, they make plane engines and sell to customers near the cost of making it. Then they only make profit from the maintenance and repair of the engines! That's how you make money, so if the companies that bought the capital items uses it more then it's good for you!

2019-04-07 11:23

science + art = stock market reality. However, sometimes it is the art part that counts. Good write up though.

2019-04-07 12:16

Negative Revenue is due to over-provide revenue in previous quarters, right? It made no sense to me the Negative-Revenue is due to cost recognition 1st and revenue later. If so, It will be operating loss, rather than negative revenue. Am i right?

2019-04-07 19:40

YiStock, in my opinion, the Negative Revenue for Schedule rate in Q4 2018 was not due to over provision in previous qtrs . The schedule rate revenues for 2018 were 124M , 120M , 127 M and -29 M respectively for the 4 qtrs while for 2017 , they were 97 M, 113M , 75M and 60 M respectively . You can see that the first 3 qtr revenues of 2018 were about 120 M per qtr . It was abnormal and unusual that Q4 has no revenue of schedule rate at all . Even in 2017 , minimum schedule rate revenue was 60 M in Q4 . Even without this revenue ,Dayang already made record profit due to exceptionally high revenue from the lump sum revenue of 269 million. THe management has over met the target . Hence , I suspect they invoice the schedule rate revenue of Q4 into Q1 2019 which was usually the low season . This will " smoothen " the linearity of revenues by qtr.

2019-04-07 20:33

https://klse.i3investor.com/blogs/hleresearch/199652.jsp

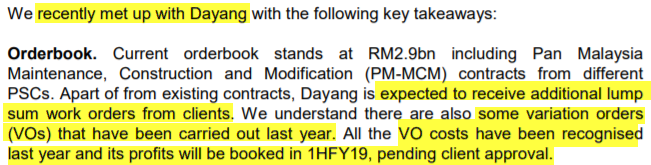

Orderbook. Current orderbook stands at RM2.9bn including Pan Malaysia Maintenance, Construction and Modification (PM-MCM) contracts from different PSCs. Apart of from existing contracts, Dayang is expected to receive additional lump sum work orders from clients. We understand there are also some variation orders (VOs) that have been carried out last year. All the VO costs have been recognised last year and its profits will be booked in 1HFY19, pending client approval.

..................

It could be extra costs which took place beyond the agreed schedule rate and subject to customer scrutiny before agreeing on the value.

Since it is executed without a prior agreed contract due to urgency or mishaps (procurement of material to facilitate the intended services), the revenue recognizable are subjective to customer agreement.

It may be accounting requirement that these extra costs are recognized as it is executed without a contract in hand.

It is very well possible for Dayang to execute this way knowing Petronas is their key long term customer based on trust.

2019-04-07 21:07

Tycoon with more than Rm 500m networth willing to donate Rm 10m here & there, thus the pledge Of Rm 2m underwriting is peanuts to him mah...!!

2019-04-08 17:06

Read carefully loh...in order for u to entitle to the guarantee, which have a composite pool fund of Rm 2m, u must buy Dayang at Rm 1.50 or below and must hold it for at least 9 mths and this cover only maximum 50,000 shares per person.

The offer is effective on 7 april 2019 onwards loh....!!

Meaning u must buy on 8-4-2019 onwards.

At the moment, even if u bought dayang at Rm 1.54, and if the share price subsequently fall below Rm 1.50 u r not entitle for the guarantee claim loh..!!

In fact not many people entitle loh...unless they manage to buy at Rm 1.50 & below today loh....!!

In addition KYY max loss reimbursement is only max Rm 2m.

KYY got alot of trick lah....he knows alot of gimmick mah....!!

This info are fed by raider's lawyer friends loh....!!

Don get con loh.....!!

It is a share moving scam loh.....!!

2019-04-08 21:38

@connie555, yes i don't like to contribute shit, like overly optimistic shit.

2019-05-23 12:40

Davidslim's analysis is very detail and complex. But it is often so wrong when events unfold post his analysis.

Essentially, he has not proven his ability in giving good analysis of stocks.

It is better to be approximately right than to be absolutely wrong.

2019-05-24 16:17

3i,can you point out which part of his analysis is wrong. With Q1 2019 result published yesterday,the 4 qtr rolling eps is 18.78 sen and PE of 4.9 with current share price of 91 sen. What he stated in his analysis are all facts. You should not use the market pricing which can swing up and down to say that he is so wrong. Mr markets are filled with emotions . The market can swing +and -50% without any change in the fundamentals.

2019-05-24 16:40

that is david style......................can make money or not don't know lah.

too complex and too detail...can see the trees but don't know whether can see the forest?

dayng is quality share or not?

2019-05-24 17:31

@pjseow - As far as my understanding, 50% of this article is about extrapolating the past into the future. You would agree everything about the future is not 'fact' but hypothesis. Just as I can state the same kind of fact but come to a totally different conclusion.

The elephant in the entire article is the $294 mil cash flow over the past 3 years, and the assumption if that can be maintained over the next 3-5 years, then Dayang is worth PE 7-8 and price XXX. Based on an equity of $1.3 bil. The ability to generate that amount of cash flow in the long run is like amazing (22%). Literally putting it in the top 5% of bursa.

But no one talks about the fade rate, how long can this go? Oh right, someone forgot to talk about depreciation of close to $130 mil per year. Purchase of PPE has not been keeping up with depreciation, accounting for only 10% over the past 3 years. Yes sure Dayang can pay off all the debt in record time. And how long before they can skim on purchase PPE before the big bills comes in to normalised the cash flow figure?

2019-05-27 08:28

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-25 16:50:00

EMA 5

5 Mins

BUY

2024-11-25 16:00:00

EMA 5

30 Mins

SELL

2024-11-25 15:30:00

EMA 5

30 Mins

SELL

2024-11-25 15:15:00

ADX

5 Mins

SELL

2024-11-25 15:00:00

EMA 5

30 Mins

SELL

Apps

Top Articles

1

2

3

Good Articles to Share

4

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

probability

Now days in most Engineered capital equipment Supply & Service providers...biggest profits are made on the service segment than capital sales.....

capital investment by customers can only grow to a certain extent....service is almost forever...

need not say on the fat margins services naturally have (cost being mainly the workforce), and the ease of increasing or reducing these resources (skilled labor) as per the changing need, i.e its not a capital intensive business.

2019-04-05 23:07