Art of Investments

INVESTORS ARE UNDERESTIMATING THIS IPO GEM THAT HAS A POTENTIAL MINIMUM 78% UPSIDE!

Recently, a company listed on Bursa and while the opening price was strong, it was quite clear that investors have underestimated the potential of this company.

The company is Feytech.

What does Feytech do?

Feytech is a manufacturer of automotive seats and seat covers. From investment bank research reports, we know that Feytech's existing main customers are Mazda and Kia. This means that Bermaz Auto is Feytech's existing main customer. The research reports also state that Feytech recently won 2 new customers and they are expected to contribute substantially. The 2 new customers are Peugeot and another unnamed customer. According to the research reports, Feytech will use their IPO proceeds to build new manufacturing plants in Kulim and their floor space is expected to almost triple from 64k sqft to 165k sqft in the near term.

Here is where investors have underestimated the potential of the company. While the company did not name the 2nd new customer, it is widely known in the industry that this unnamed new customer is Chery. Investors may not have realised the potential of Feytech because they did not know about Chery. Meanwhile, investors who are aware of Chery have clearly underestimated the popularity and selling power of Chery in Malaysia. Below is a screenshot of an article on Chery Malaysia:

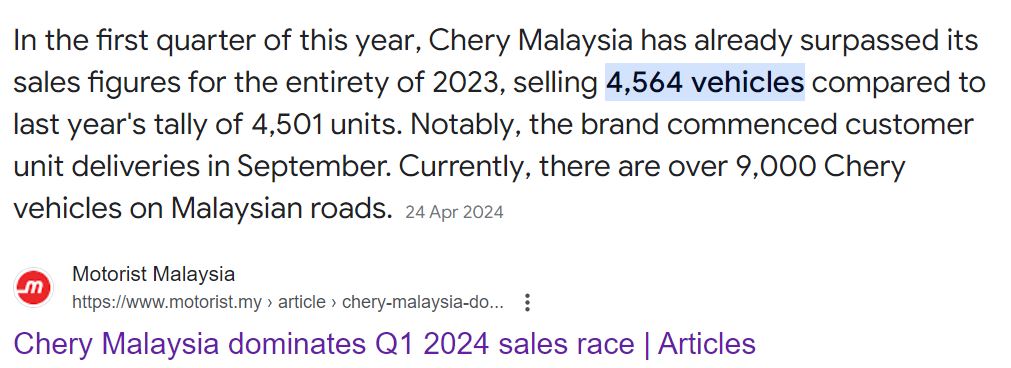

Chery cars, especially its SUV, is wildly popular in Malaysia due to their sporty interior and exterior designs, powerful performance and cheap price points. It is so popular that their sales volume is actually now quite close to Proton X50! Below is an article on Chery's sales volume performance for the 1st quarter of 2024:

https://paultan.org/2024/04/05/chery-malaysia-sold-4564-units-in-q1-2024-omoda-5-and-tiggo-8-sales-not-far-short-of-proton-x50-x90/

How to value Feytech?

It is actually quite simple. There is a very close comparable and this company is Pecca. Pecca's share price has increased by 7x in the last 5 years! They are currently trading at a PE multiple of 24.5x.

Can Feytech's 1Q24 net profit of RM16.8 million sustain? There is no doubt that this number will not only sustain but it will be much stronger because of Chery's blazing sales. If we were to be conservative and annualise their 1Q24 profit and use Pecca's PE multiple of 24.5x, Feytech will be valued at a market cap of RM1.65 billion or RM1.96 per share. At the current share price of RM1.10, Feytech is trading at a PE of 14x and is crazily undervalued.

It is a matter of time before the share price of Feytech increases significantly like Pecca to reflect the strong potential of the company.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Art of Investments

ICON: This is why Yinson's boss bought the company. He bought it at a steal!

Created by csan | Apr 01, 2024

MANUFACTURING GEM THAT RECENTLY DOUBLED ITS PROFIT AND IS ABOUT TO TRIPLE ITS CAPACITY!

Created by csan | Nov 18, 2023

THE MOST UNDERVALUED TOURISM STOCK IN THE HISTORY OF BURSA THAT COULD INCREASE BY 400-800%! (UPDATED)

Created by csan | Mar 06, 2023

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-26 16:35:00

EMA 5

5 Mins

BUY

2024-07-26 16:35:00

TURTLE SYSTEM 20

5 Mins

BUY

2024-07-26 16:30:00

EMA 5

30 Mins

BUY

2024-07-26 16:30:00

EMA 5

10 Mins

BUY

2024-07-26 14:30:00

EMA 5

10 Mins

SELL

Apps

Top Articles

1

BFM Podcast

2

MQ Market Updates

3

BFM Podcast

4

BFM Podcast

5

BFM Podcast

6

M+ Online Research Articles

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....