ValueGrowth Investing

Some Crazy thinking about purpose of AirAsia's AAC disposal

valuegrowth

Publish date: Fri, 10 Mar 2017, 10:34 PM

valuegrowth

0 5

Stock market is keep changing from seconds to seconds, but business environment isn't.

Instead of keep looking at the market conditions, do your due diligent will work more.

Instead of keep looking at the market conditions, do your due diligent will work more.

After an impressive 4Q2016 result annoucement on end Feb, the main focus on AirAsia Berhad ("AAB") is about disposal of its aircraft leasing arm - Asia Aviation Capital ("AAC"). The tender closing date for binding bid would be on 27 March 2017 and it's expect to be conclude by 3Q2017.

In its latest analyst meeting early this week, AAB has disclosed the following:

1. AAB will transfer 7 more aircrafts to AAC, then...

erm... let not waste our precious friday night writing/reading a lengthy article, go straight to summary table:

Basically, we could see from above that AirAsia is trying to (1) disposal of 207 out of 545 of total owned aircrafts (current & future) as well as to (2) remove 34 aircraft leasing commitments from it balance sheet. Do note that normal practice in aircrafts leasing business is that once you commited to lessor, you are not allow to cancel it before maturity. By transfer those 34 leasing commitments to AAC, AirAsia is now free from this mandatory commitment.

Now, the crazy thinking i would like to share is not about item(2), it's about item (1) - disposal of 207 out of 545 owned aircrafts.

This number doesn't have any meaning by its own, to illustrate what I am thinking about, we would have to refer to 2 reference material:

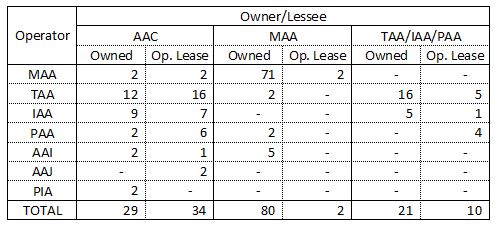

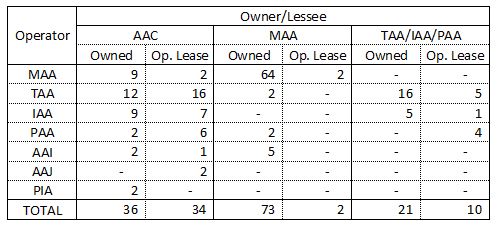

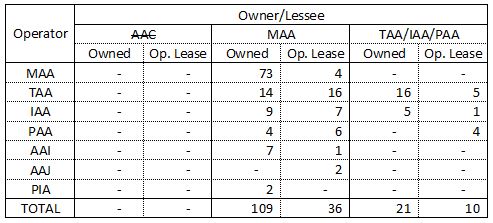

Reference 1. Aircrafts profile of AAC, MAA & associates (shared by MIDF)

a)This is what current profile look like: (pls ignore Op lease column, that's item (2) above)

b)This is how it look like after transfering of 7 aircrafts:

c)This is how it look like if AAC is not exist and all AAC's aircrafts belong to MAA:

So, what I think about is that AirAsia is trying to remove 36 aircrafts from its balance sheet, which is about 33% of total aircrafts currently owned by MAA. For future deliveries, AirAsia also considering to sell 33% of future deliveries to MAA.

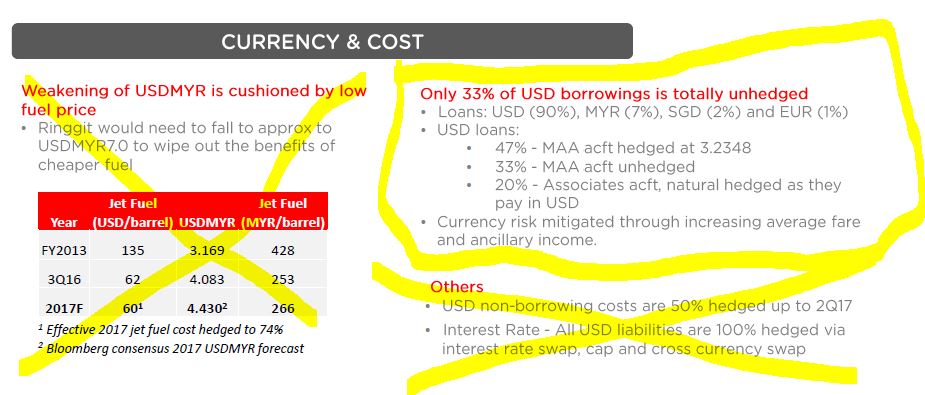

Reference 2. AirAsia's hedging/loan profile on aircraft deliveries

This is what we get from Pg11 of 3Q2016 's Presentation slide:

(Hey! look at the hedge profile, not my beautiful art, ok?!)

I think you get what I am thinking about, right?

The purpose of AAC could probably not only about SLB, cash dividends, and unrealise forex gain by converting Asset value in RM to Asset value in USD, it's probably also to dispose those unhedged aircrafts which AirAsia must convert their Ringgit cash to USD at 1:4.48 exchange rate to repay their loan now. If this is true, this would become the most important reason why AAC exist and need to be disposed.

Imagine that, by selling those 33% unhedged aircrafts (via AAC), AirAsia make an immediate realised forex gain of RM(4.48-3.23) x (aircraft market value + difference between aircraft market value & AirAsia's purchase price + time value of aircraft deliveries slot). That's humonguos gain isn't it??

Of course, this scenario would only be possible if the hedging is tied to the aircraft, i.e the forex rate for each one of 47% of aircrafts is paid in 1:3.2 while each one of 33% is paid at current exchange rate, instead of compound exchange rate for each aircraft.

That's why I say this is a crazy thinking.

But who know, maybe I am correct about it.

Imagine again, all those ugly unrealised loss on aircrafts loan, it's all gone by now (probably with little bit of gain)! it's gone!!!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on ValueGrowth Investing

AirAsia & AAX named in UK's bribery case against Rolls-Royce (Mkini)

Created by valuegrowth | Jan 22, 2017

2017 is a bad year for AirAsia due to higher fuel price & low RM? let check!

Created by valuegrowth | Dec 20, 2016

AirAsia Bhd will be doomed due to subscription of IAA's Capital Securities? Let check the facts.

Created by valuegrowth | Dec 17, 2016

Discussions

3 people like this. Showing 14 of 14 comments

Magic number! 33%! If AAC worth 1B USD, current Airasia should worth 3B USD which is 3x4.45= 12.35B Ringgit /3.34 NOSH = 4.00 per share. Haha.. simple mathematics.

2017-03-11 01:24

Valuegrowth,

I try to digest your story but not sure I understand it correctly or not. Please forgive me if I ask some stupid questions here.

1. Do you mean that the hedging strategy is apply to future aircraft booking as well? I personally don't think so la but I hope that you are right and I'm wrong. haha..

2. For existing US loan, I think that you are right. The hedging portion should tied with aircraft loan. But as long as MAA still hold the aircraft, we can't see these as one off profit (generally retailers are happy to see huge jump if got one off profit). Am i right? I believe that this gain will only slowly show in operational profit since you serve loan in 3.2 ringgit but gain in 4.45 ringgit asset and 34% AA revenue in foreign currencies.

3. Is this the main reason 28 aircraft from MAA would entail a SLB agreement and make it one off profit in P&L? If yes, then Q1 PAT may reach 800M!!! 400M from operating profit and 350M foreign gain!!! And it is realised gain!!!!! If it is true, Q1 PAT will be super NICE!! But later some reporters may say PAT Q117 vs Q116 is drop from 878M to 800M. hahahahaha...

Thanks valuegrowth for your sharing. Learn a lot from you!

2017-03-11 02:16

Hi valuegrowth, if follow the example below :

http://imgur.com/a/SIgDi

Either to go for options or forwarded contract, the hedging is totally isolated from the aircraft loan itself as they are different transactions.

And AAC accounts are all denominated in USD. When AA transfer a plane from its associate to AAC, there is no point to transfer together with the plane loan hedging as the hedging would be settled in RM, however AAC cash flow are mostly in USD. Imagine how silly a deal would be to convert the USD to RM by AAC to settle the hedging for USD borrowing but in fact you have rich of RM in MAA accounts?

There would be extra forex services charges incurred to do that.

https://www.youtube.com/watch?v=LrRymIPFobY&feature=youtu.be&t=2890

This AA senior management claimed that AAC has USD600+M immuned from forex fluctuation.

If you cross check to AAC account from 4Q16 report, its borrowing is USD632.2M which is totally matched to his statement.

Hence, we can conclude that all of the AAC aircrafts borrowing are unhedged loan.

I believe this would apply the same after AAC sales, the hedged contract or options would be retained in AA as it does not make sense for the buyer to purchase together with RM based hedge contract for this USD orientated AAC.

2017-03-11 02:42

feicsh/valuegrowth,

Let say the loan amount =10B ringgit (70% hedged at 3.2 ringgit : 1 USD, 30% unhedged). Worth 7B /3.2 + 3B /4.45 = 2.86B

MAA owned 70 aircraft, AAC owned 30 aircraft

Assume your asset value = loan amount is USD = 2.86B USD = 2.86x 4.45 =12.7B ringgit

Now MAA sell all aircraft to AAC

MAA owned 0 aircraft, AAC owned 100 aircraft

MAA balance sheet before selling

Asset=10B

Liability=10B

Equity=0

MAA balance sheet after selling (sell with 12.7B)

Asset=0

Liability=0

Equity= 2.7B

Am I correct under this scenario? Please correct me if i'm wrong. Appreciate it.

2017-03-11 11:27

batu88, I think the hedged contract/options would keep booked under MAA's USD borrowing hedge before expiry. MAA would not possible to become 0 liability as new aircrafts would coming in, there is no indication of AA planning on 100% aircraft operating lease, some of the new deliverables would still parked under MAA. So in the condition of USD/RM rate keep staying above the hedging rate, those isolated contract/option would help MAA to dilute further for MAA's USD loan no matter it's growing or shrinking.

2017-03-11 12:01

Batu

1. What I mean is MAA will outright sell all future aircraft (those without hedge) to AAC in future. Which mean the remaining aircraft they would take delivery are either hedged at 3.2 or would be delivered to associates (natural hedge).

2. feisch has replied and corrected what i am wrong: purchase & hedging are 2 transaction. But I do still believe that even if it's 2 transactions, that would still be 1 hedge contract/option tie to 1 aircraft, and MAA only transfer/sell those without hedging to AAC.

[Those hedged would ensure MAA wouldn't suffer from forex loss, while those unhedged are now transferred to AAC to remove MAA's forex loss.]

3. those 38 aircrafts from MAA (HLIB & CIMB: 38, MIDF said 28) just a normal sell & lease back and probably are hedged aircrafts, so when they SLB, probably they would earn value difference & forex gain (as they paid in RM3.28 and now received RM4.48).

2017-03-11 13:08

Agree with feisch, he pointed out a very important thing: hedging has no meaning to AAC as they are USD denominated.

Transferring of hedged aircrafts to AAC has no benefit to AAC and the only gain to MAA are value difference in SLB. MAA would have to pay higher lease rate at higher exchange rate of 4.48 now, instead of paying their borrowing now at 3.23.

2017-03-11 13:26

Thanks feicsh. We all know that AA is undervalue with their current fundamental /valuation. But these have not been clearly show in P&L and balance sheet.

Thus, I'm trying to guess what TF going to do with AA balance sheet and how to reflect these gain into P&L in coming 17Q1. Should have big action to Q1 to boost up their MAX valuation on AA since they are going to listed in HK. Currently what we know are:

1. Transfer 7 aircraft to AAC - will write off those unrealised gain and will see the significant forex gain by next Q report. Just like Q4 16 report, suppose to have 300M forex loss, but fully offset by 29 aircraft in AAC by booking their asset in USD. As simple as 1 click only. Lol..

2. SLB 28 Aircraft to AAC - Same as above.

3. Gearing may drop below 0.8 after these actions.

Before this, i guess AA will sell 100% of AAC and distribute 70% money receive from AA as special dividend + balance 30% to clear new debt (8 new aircraft for MAA this year). But now I guess it differently. AA might only sell 80% of AAC with around 1B USD and 100% distribute as dividend (RM1.30 per share), this is quite close with CIMB analysis. New debt can be 100% offset by disposal of old aircraft to AAC and those unrealised loss is gone as mentioned by valuegrowth.

Now TF action is better than what I can imagine before. No wonder he is the one become AA CEO but no me.. Hahahahaha... Everything is smooth and we just wait AA fly to the peak very very soon. Now I can guaranteed PAT in Q1 is at least +600M.

Yes, f**king to unrealised loss. Hahaha

2017-03-11 13:36

Thanks valuegrowth. Can I summaries like this way:

1. AA will earn higher margin with loan payment 3.23 MY:1.00 USD for own fleets and at the same time earn the asset in USD.

2. But lower margin from leasing units since you need pay leasing fees base on current currency rate.

3. Show significant amount in forex gain (not in cash) due to write off most of the unrealised lose.

Am i right?

Thanks for valuegrowth and feich for sharing. Sorry if I trouble you two too much. I'm still new in stocks and still got many things to learn from you all. REally appreciate it.

2017-03-11 13:50

USD always the same, the difference is in RM.

For AAC, the leasing margin would remain same, as always USD.

Not sure if they will show it as FOREX gain or other revenue.

2017-03-11 14:15

Batu, everyone at here are to learn from each other. I learned a lot from u too

2017-03-11 14:17

Valuegrowth & batu88, Ya, I hv learned a lot from both of you and other sifu too......thanks and pls keep contributing

2017-03-11 17:42

Appreciate the analysis.Some of it is a bit too much for my layman's head but I get the gist of what you're saying. Thanks for taking time out of your Friday night to benefit the rest of us.

2017-03-14 15:16

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-23 14:50:00

EMA 5

5 Mins

BUY

2024-07-23 14:35:00

EMA 5

5 Mins

SELL

2024-07-23 12:00:00

EMA 5

30 Mins

BUY

2024-07-23 10:50:00

TURTLE SYSTEM 20

10 Mins

SELL

2024-07-23 10:40:00

TURTLE SYSTEM 20

10 Mins

BUY

Apps

Top Articles

1

BFM Podcast

2

https://dividendguy67.blogspot.com

3

4

5

6

Koon Yew Yin's Blog

7

save malaysia!

8

save malaysia!

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

cruger12345

Ha ha ha that is very imaginative. You shall work in AA treasury department . I hoe you are right ;)

2017-03-11 00:18