THE INVESTMENT APPROACH OF CALVIN TAN

Top 10 reasons why you must be very careful not to chase AAX or AirAsia shares now! (Calvin Tan)

calvintaneng

Publish date: Mon, 28 Nov 2016, 02:14 AM

calvintaneng

0 1,854

Hi Guys,

I have An Investment Approach I which I would like to all.

I have An Investment Approach I which I would like to all.

Hi guys/gals,

These are the 10 reasons why you must not hold but sell your AAX & AirAsia shares

1) HIDDEN DEBT IN OFF BALANCE SHEET: AirAsia's debt is Rm79 Billion while AAX's is Rm110 Billion

If only just proposed purchase it should be reported under Company Announcement. But these ARE COMMITED PURCHASE. So they must be accounted for. In this case it is placed under "Off Balance Sheets" accounting. These debts are real as we shall SEE later.

2) US DOLLAR UNCERTAINTY WILL IMPACT ON AAX & AirAsia's Huge Borrowings

The collapse of the ringgit during the Asian Finacial Crisis was the undoing of Malaysia weak banks & companies. Many went belly up. While AirAsia/AAX have partially hedged their US Dollar Debt. Those unhedged debts are still ernomous. Then there are ordered planes due for delivery in year 2017 and onward which are not hedged as yet. So the risks going forward will be even more amplified.

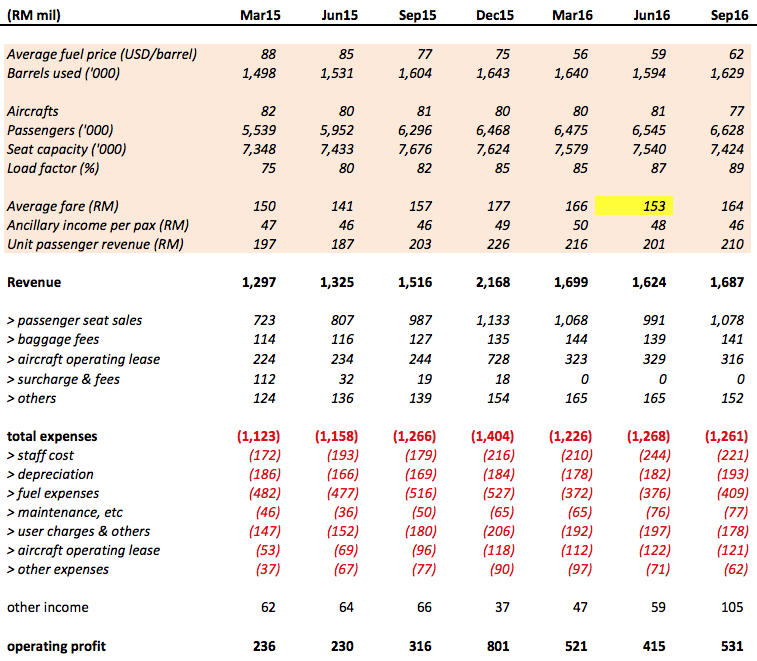

3) The Latest Figures show that AirAsia is having thining margin in profit

While Average fare has increased from last quarter Rm153 to Rm164

Ancillary income per pax has actually dropped from Rm48 to only Rm46

For a seat in a plane worth Rm400 million with such razor thin margin of Rm46 profit? This is even worst than using Roll Royce as Uber taxi getting Rm15 fares?

No wonder Bloomberg came out with an article saying AirAsia would be making a Loss if not for Leasing planes to subsidiaries!!

SEE

4) DEPRECIATION IS MINIMIZED FOR A HIDDEN DEBT BOMB OF RM79 BILLION

X

Depreciation

for last 4 quarters

184 + 178 + 182 + 193 = Rm737 million for Airplanes, property & equipment is just too little lah!

Now AirAsia has 170 A320 flying in the Sky. Total committed debt from Qr report is a Whopping Rm79 BILLION

So depreciation per year of Rm737 million over Rm79 BILLION = 0.009%?

AirCraft depreciation less than 1%?

Where got such accounting?

So AirAsia lease?

Under Aircraft operating lease

for last 4 quarters

118 + 112 + 122 + 121 =RM473 million

So add AirCraft (PPE) depreciation Rm737 Million + all leases Rm473 Million

= RM1.21 BILLION

Now divides by Rm79 BILLION (listed away from Main Balance sheet as Off Balance Sheet expenses)

= 1.5% Total depreciation plus operating lease cost?

Where in the whole world where car, plane, train or ship depreciates by only 1.5% per year?

This is hidden fraud accounting. Looks like the trick learnt from China listed companies?

Depreciation

for last 4 quarters

184 + 178 + 182 + 193 = Rm737 million for Airplanes, property & equipment is just too little lah!

Now AirAsia has 170 A320 flying in the Sky. Total committed debt from Qr report is a Whopping Rm79 BILLION

So depreciation per year of Rm737 million over Rm79 BILLION = 0.009%?

AirCraft depreciation less than 1%?

Where got such accounting?

So AirAsia lease?

Under Aircraft operating lease

for last 4 quarters

118 + 112 + 122 + 121 =RM473 million

So add AirCraft (PPE) depreciation Rm737 Million + all leases Rm473 Million

= RM1.21 BILLION

Now divides by Rm79 BILLION (listed away from Main Balance sheet as Off Balance Sheet expenses)

= 1.5% Total depreciation plus operating lease cost?

Where in the whole world where car, plane, train or ship depreciates by only 1.5% per year?

This is hidden fraud accounting. Looks like the trick learnt from China listed companies?

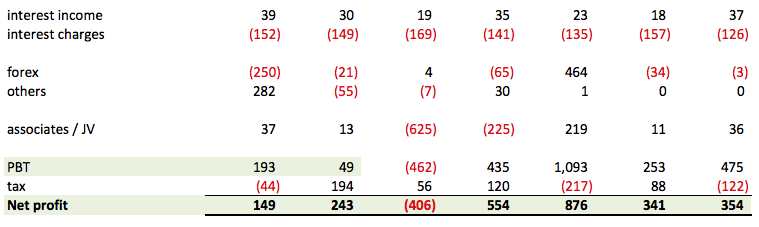

5. BLOOMBERG STATED THAT AIRASIA ACTUALLY BOOKED ITS LEASING REVENUE FROM SUBSIDIARY AS PROFIT

SO IF WE DEDUCT LEASING REVENUE FROM THIS QUARTER PROFIT THE FIGURES WILL BE

RM354 MILLION - RM316 MILLION

THIS WILL BE THE ACTUAL PROFIT OF THIS QUARTER

RM38 MILLION

And since AirAsia is leasing planes to AAX Thailand, AAX Indonesia, AAXPhillipines & AAXIndia for profit the model is flawed as it is like

a) Robbing Peter to pay Paul (And both Peter & Paul are in the same family)

b) Transferring monies from left hand to right hand?

c) Swallow own saliva to quench thirst?

This kind of accounting cannot Solve The Huge Debt Burden in US Dollars. Nor can it stem the high depreciation cost.

6. HIGH DEBT REPAYMENT

Repayment of borrowings for Jan to June 2016 = Rm2.056 BILLION

Full year would be over Rm4 BILLION (So how could the total debt of AirAsia be around Rm10 BILLION?

AA is paying for Off Balance Sheet Debt of Rm79 BILLION!

Don't believe?

Well, look at year 2015 Jan to June figures

Rm2.199 BILLION (6 month). Annualized = Rm4.3 BILLION!!

SO THERE HAS BEEN HUGE DEBT PAYMENTS ALL ALONG.

7) ACTUAL CASH POSITION HAS SHRUNK!!

CASH POSITION OF AIRASIA HAS DROPPED!!

(Refer to Balance Sheet again!)

Cash in the Beginning of Year = RM2.46 BILLION

Less Cash (RM929 MILLION)

Cash Position Now: RM1.533 BILLION

Cash Position has dropped by 39% to only Rm1.533 BILLION Only

SO CASH POSITION CANNOT COVER COMING BORROWING PAYMENT OF OVER RM2 BILLION For 2nd Half Year of 2016!!

This AAC can only cover Debt payment for 2nd half year of 2016

A little will be left for debt payment for Jan to June 2017 (Again Rm2 BILLION to be paid)

That's why Calvin Tan Research already stated clearly that

Airasia is sitting on a Time Debt Bomb!!

Forget about "special dividend" from AAC sale.

So don't be surprised that AirAsia will still need go a begging for more monies by selling other stuff or other tricks?

8) AS PRICE OF AIRASIA IS GOING UP FUNDS & INSIDERS ARE SELLING & SELLING

Just like Gadang where Insiders like Kok Onn, ColdEye & KYY are selling into strength

Wellington have sold & left AirAsia. TF is also selling. And EPF has sold down and ceased to be a substantial shareholder now. As EPF is no longer a substantial share holder now is EPF continuing its disposal quietly?

9) THE SALE OF AAC Shows Signs of Debt Distress!

Why sell the golden goose that lays the golden egg? If not for the debt distress! No one will go and pawn his precious family treasure or heirlooms UNLESS he is in financial distress!

As the monies from Rm1 Billion pp to TF & others are slow in coming AirAsia is increasingly stressed by

a) High US Debt going out of control

b) Constant challenge from Malino Airlines throwing 1 million seat offers. MAS relaunching China & other routes. Leading to fierce competition & low profit per passenger seat = only Rm46 net income. This razor thin margin will continue indefinitely.

c) Huge leasing/hire purchase debt of over Rm4 BILLION each year!

10) BEST TIME TO SELL BEFORE ANOTHER COMING STORM ON THE WAY

Now that Trump is elected into power US will go into deglobalization. As such we are now flying into unchartered territory of protectionism which will hit all the economies of the world. Will it trigger another Great Depression?

If so better stay firm on terra firma. Lest we are swept away by a Depression era financial tornado

Catching "Air" in Asia?

Great the Depression,

Global the Recession;

Many a millionaire

Jumped, clutching the air.

Millions flown away

Fortunes gone astray,

Bursa in retreat,

Bulls by bears were beat.

Hard the lessons learnt;

Fingers - more - were burnt;

Conman has done his job

All are finally robbed!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on THE INVESTMENT APPROACH OF CALVIN TAN

JCY (5161) Posted a 2nd Qtr of Good Profits: Showing a Clear Sign of A Turnaround, Calvin Tan

Created by calvintaneng | Aug 23, 2024

TSH RESOURCES AUGUST 2024 RESULTS: A Look at its Latest Balance Sheet, Calvin Tan

Created by calvintaneng | Aug 22, 2024

UNDERSTANDING DIFFERENT FORMS OF VALUE IN VALUE INVESTING, Calvin Tan

Created by calvintaneng | Aug 03, 2024

Discussions

Be the first to like this. Showing 50 of 60 comments

Alamak...Calvin masteel go to holland...pity those follow Calvin at 1.04. 35% drop

2016-11-28 11:12

Calvin selling another house to average down his Masteel...i am curious how many house he have...liar of i3 or 车大炮 is his new nick now

2016-11-28 11:14

Dun disturb him lah .. He currently open a new stall in Chowkit selling underwear few weeks ago. If you are one of his disciples you can still meet him @ Jalan Alor selling something else. This line of business give better returns than his stock picks ... according to his friend wahaha

2016-11-28 11:35

Thanks for many points presented but still not convincing. Element of selective interpretation and focusing only on cons from overall financial performance datasheet. Like Chinese say, try only to picking bone from an egg!

2016-11-28 11:38

I'm newbie in market so do correct me if i'm wrong. I just try to understand this article and I have few queries here.

1. I believe that 79billion is refer to undelivered aircraft. In accounting basis, you can book the undelivered aircraft as asset or debt if you not receive the item yet, am I right? From business sense perspective, if you item is not receive to operate your business yet, why you need to book it as debt which it does not cause u a single cent now?

2. Weaken in ringgit is definitely not a good thing to AA. But when we look back to Q3 2016 report, AA manage superbly on forex gain loss. For undelivered aircraft, it should book under the current currency and it's won't cause the forex gain loss. In term of margin, the may slightly cut in my view but as long as the business is growth with healthy profit margin, I does not foreseen any issue there in future.

3. AA is a low cost carrier, ALL the LCC business model is always work like this way. Take your Roll Royce as Uber taxi as an example. Your roll royce is worth 1M, depreciation is 5% per annum which is 50k, assume your expense (fuel, operational cost,etc) is 50k, interest is 50k per years. But u earn 200k for ticket (include luggage charge, sell food in car, lol). You still received handsome profit 50k. Profit margin should look like this way: operation profit / total revenue = 50k / 200k = 25% but not 50k / 1M = 5%.

4. Why undelivered aircraft involve in depreciation? It does not make sense.

5. Bloomberg is exactly true in my view and the calculation part is definitely wrong. Please refer to Icon8888 article. Numbers wont lie.

http://klse.i3investor.com/blogs/icon8888/110097.jsp

6. Repayment of borrowing to reduce debt. I do not see any problem on this. Sound good to me.

7. I never worried about cash position for AA as long as they can earn money. AA is always healthy in cash flow when they are in earning position. y? All your air ticket need to pay advance, right? lol.. This is the beauty for this kind of business.

8. I do not know where u can get this news such as TF is selling, etc. Thus, I cant prove it wrong but don't think that you can prove it right as well.. lol.

9. AAC selling is good but public does not value it as it was. Let say it worth RM1, but public (share price) only reflect it RM0.50. And now someone offer your RM1.40. I think is a good timing to spin-off. I do not few weird if AA have another AAC in few years later and spin-off again.

10. This fear sound a bit silly to me. It's like to avoid the car accident, so you better not to drive a all. Lol...

2016-11-28 11:52

Calvi gives sell call so that he can buy cheap..... Look airasia price goes up

2016-11-28 16:38

Dont trust calvin because when Q4 result out, IB especially CIMB will revise price upwards..... first year orofit since listing

2016-11-28 16:50

I wonder how Calvin lives in real life, he seems to be classified as unwelcome figure here.

2016-11-28 16:52

Calvin call to sell fast fast Mycron.

I can't sleep last nite, sure good result this qtr.

2016-11-28 16:53

to all especially newbies. kindly do not trust this calvin's articles.

he conveniently omited so many facts becoz he simply did not understand the word depreciation.

http://klse.i3investor.com/blogs/www.eaglevisioninvest.com/109716.jsp

this article will explain all depreciation n operating lease ideas on AA.

calvin has abandoned the thread simply becoz we are right n he is wrong.

good investing all.

calvin this time we have seen that you have spread misinformation DELIBERATELY on i3.

this is just plain wrong. now i see that u are a really bad person at heart.

my god. bless us all.

2016-11-28 16:57

Hi guys,,

Go to Ifca forum and read the whole tread.

90% of the ifca diehard hopeful hated Calvin. All rejected my kind warning. In the end?

90% of. the people in ifca forum lost all and stopped posting

2016-11-28 17:01

Go back to Masteel & Bpuri , u owe newbies an explanation for the pricey holland trip.

2016-11-28 17:09

Calvin reaction of his stock recommendations :

When stock up : he will make noise n say chun chun

When stock down : he will keep quite

when people criticize him stock down : he say this is for long term

hahahahahaha....Jokers of the century...

2016-11-28 17:14

only those who made a mistake of buying expensive mentions the words averaging down n long term everytime.

lol

2016-11-28 17:16

Calvin blue bird, how is your Masteel MRT project in Iskandar Malaysia? What else u know about MRT/LRT project in JB?

2016-11-28 17:47

the scary thing about Calvin is that he keep talking kind words while stabbing you and pouring poison down your throat... spooky... hoo hoo hoo....

Posted by calvintaneng > Nov 28, 2016 05:01 PM | Report Abuse

Hi guys,,

Go to Ifca forum and read the whole tread.

90% of the ifca diehard hopeful hated Calvin. All rejected my kind warning. In the end?

90% of. the people in ifca forum lost all and stopped posting

2016-11-28 17:51

By the way, calvin use Icon8888 table in no3. Lol... highlighted cell is exactly same.

2016-11-28 18:34

Icon8888 the scary thing about Calvin is that he keep talking kind words while stabbing you and pouring poison down your throat... spooky... hoo hoo hoo....

Posted by calvintaneng > Nov 28, 2016 05:01 PM | Report Abuse

Hi guys,,

Go to Ifca forum and read the whole tread.

90% of the ifca diehard hopeful hated Calvin. All rejected my kind warning. In the end?

90% of. the people in ifca forum lost all and stopped posting

28/11/2016 17:51

Icon8888, Icon8888,

There is nothing scary about Calvin. Calvin has been very concerned that all the people of i3 forum be safe, secure & well.

My kind intention of warning about danger has been misconstrued & misinterpreted.

Never mind. Time will tell. And I am happy to wait for the ultimate truth to surface one fine day.

One more thing.

Your assessment of Bj Corp's Net Asset Value is faulty. Please go and correct the article. Bj Corp - No muscle, no brain.

2016-11-28 20:42

Posted by Icon8888 > Nov 28, 2016 08:46 PM | Report Abuse

Another round of kind words by Calvin Tan....

Yes,

I want you to correct the Net Net report of Bj Corp's Properties first.

See, I don't want to over right what you already posted.

2016-11-28 20:48

Posted by Benjamin_8888 > Nov 28, 2016 08:49 PM | Report Abuse

Ya ka kind words? What about your Masteel MRT project ?

Masteel?

MASTER OF ALL LONG STEEL!

Don't look at just one or two quarters. Think longer term.

2016-11-28 20:52

This Calvin last time still has a bit of style. Loss money but still act like gentleman

But this year after registering portfolio loss of 60%, he has turned disparate. Bark and bite like a mad dxg

Poor Calvin...

2016-11-28 20:53

Posted by Icon8888 > Nov 28, 2016 08:56 PM | Report Abuse

Wow DRB 1.01 !!!! This stock was intensively promoted by Calvin

YES! CALVIN IS HERE!!!

I AM A FIRM BELIEVER IN ECOMMERCE!

DRB HAS TAKEN 53.5% OF POS

AND POS GOING INTO ECOMMERCE BIG BIG TIME!!

JACKMA OF ALIBABA WILL BE HERE IN MARCH 2017 TO LAUNCH E FTZ (FREE TRADE ZONE)

AND SO IF DRB PRICE GETS CHEAPER I WILL TURN EVEN MORE BULLISH!!

THE TIME TO BE BULLISH ON TGUAN WAS BELOW RM1.00

THE TIME TO BE BULLISH ON PERAK CORP WAS 60 CTS

AND SO CALVIN IS TOTALLY DIFFERENT FROM ALL OTHERS

WHILE OTHERS ARE BULLISH AT MARKET TOPS

CALVIN IS BULLISH AT MARKET BOTTOM!!!

HIP HIP HAPPY!!

2016-11-28 21:02

Yeah Calvin you can be bulish at market bottom ... Buy Perisai 5sen. PN17 Market bottom

2016-11-28 21:41

HOLD TIGHT YOUR PRECIOUS DRB SHARES!! CANDIDATE FOR PRIVATIZATION!!

CALVIN HIT PRIVATIZATION JACK POT NO. 4 TODAY

THE STORE BEING TAKEN PRIVATE FOR A 50% UPSIDE GAIN

calvintaneng WOW! WOW! WOW!

Another Chun Chun Call by Calvin Tan Research

On January 19th 2014 Calvin called for a buy on The Store at Rm2.35

Today, It is being taken private at a Nice Rm3.52

So price plus small dividend of 3.75% equal to a 50% Gain!!

Now These Are The Stocks Recommended by Calvin Tan Research taken private

1) SUPER ENTERPRIZE

Call to buy Rm1.25. Taken private Rm3.75 (UP A WHOPPING 200%)

2) KULIM

Call to buy at Rm2.50. Taken private by Johor Corp for Rm4.10 (UP A NICE 60%)

3) TMAKMUR - Land of Prosperity

Call to buy at Rm1.38. Taken private by Pahang Sultan at Rm1.90 (37% Profit)

4) AND NOW THE STORE

Call to buy at Rm2.35 on January 19th 2014 at Rm2.35 .

OFFER TO TAKE PRIVATE AT RM3.52

Plus 3.75% dividend = THE GAIN IS 50%

YAHHOOOOOOOOOOOO!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

Calvin Tan Research specializes in overlooked, under researched & undervalue stocks!

HITTING JACK POT TIME AFTER TIME AFTER TIME!!!

28/11/2016 22:08

2016-11-28 22:16

You keep The Store for three years and price now is RM 3.05. So, price gain only around 35%. Divide by 3 - get 10%, if consider compounded rate, only around 8% per year....

Aiyaa.... in this case, keep money in Public Mutual better .... or buy AAX better...Buy AAX around 20 cents , in less than one already 40%. One year - 100% capital gain. Where can get ?

2016-11-28 23:37

Posted by radzi > Nov 28, 2016 11:37 PM | Report Abuse

You keep The Store for three years and price now is RM 3.05. So, price gain only around 35%. Divide by 3 - get 10%, if consider compounded rate, only around 8% per year....

Aiyaa.... in this case, keep money in Public Mutual better .... or buy AAX better...Buy AAX around 20 cents , in less than one already 40%. One year - 100% capital gain. Where can get ?

Calvin replies:

Price was Rm2.35 on January 19th 2014. Every year got dividend. MGO is Rm3.52

So 18% per year lah!

6 times Bank FD at 3%.

As for AAX the price on January 19th 2014 was a high of 99 cts.

Today AAX is 37 cts. So a drop of 63%

So between loss of 63% plus gain of 54% in THE STORE

The difference is 117% for 3 years. Or 39% per year (of course for those who avoided losses in AAX but bought THE STORE instead!

Ok mah.

2016-11-28 23:48

Calvin, as a pioneer in eB2B, i would say e-commerce is not practical at this moment.

亞航這盤生意如履薄冰,如今山雨欲來,新一輪插水將歷史重現!

2016-11-28 23:56

CT's Another moronic suggestion. He accidently locked himself inside the THE STOREroom now shouting like tanjung rambutan escapee waiting for sohai to open the door for him so he can run away ... Something like DKSH today ..... kekekekeke.

Non stop laughter from this clown stock picks

2016-11-28 23:57

Posted by supersaiyan3 > Nov 28, 2016 11:56 PM | Report Abuse

Calvin, as a pioneer in eB2B, i would say e-commerce is not practical at this moment.

亞航這盤生意如履薄冰,如今山雨欲來,新一輪插水將歷史重現!

Calvin replies:

Precisely times are getting so bad that ECommerce will thrive!

Why is it so?

Answer:

In bad times people want to save monies.

By buying from Lazada or 11th Street a person can save from 30% to 50% for all aircond, fridge, tv, bed, household stuff & others.

All brand new with warranty. And delivered to your door step at your convenience.

So just like taking MRT Train, eating McDonald fast food, using iphone - ECommerce will be a sunrising industry.

After I had bought so many stuff from Lazada & 11 Street in Malaysia. And from Alibaba, Tabao & Amazon from Singapore I don't think I will buy any thing through conventional means any more except going out for dining maybe.

LISTEN LISTEN LISTEN

WHETHER YOU LIKE IT OR NOT ECOMMERCE WILL BE SWEEPING ALL OVER MALAYSIA WHEN JACKMA COMES ON MARCH 2017

AND BETTER LOAD UP POS/DRB SHARES NOW IN CASE

SYED MOKTAR SUDDENLY TAKE THEM PRIVATE!

2016-11-29 00:05

If like Ecommerce, buy POS. Dont like big debt, dont buy DRB. People dont know what to be taken private unless it is Insider Trading. Insider Trading is punishable in Malaysia.

2016-11-29 05:23

Calvin replies:

Price was Rm2.35 on January 19th 2014. Every year got dividend. MGO is Rm3.52

So 18% per year lah!

6 times Bank FD at 3%.

.......................

Radzi replies :

Why should I follow you if I can make more than 50% a year ? LOL.

As for AAX, price is 20 sen January 2016 and now around 37 sen.

More than 75% profit in less than 1 year time.

2 times Calvin call and shorter time period achieved.

2016-11-29 05:28

Jun 12, 2015 09:35 AM | Report Abuse

SCOMI

Its Salient Factors

1) Now selling at 44% Discount to NTA

2) Selling at forward P/E of only 3.85

3) Forward growth (annualized} is 25%

4) Rebound of Crude Oil

5) At 22.5 cents Scomi has fallen to attractive levels now!

6) With New Awards to Scomies (Scomi subsidiary) for drilling oils Scomi fundamental is great!

7) By all yardsticks Scomi is now a strong buy!

Another Penny Stock With Potential

Brought to you by

Calvin Tan Research

..... and today the " super counter of Malaysia investment " sank to 9 cents

2016-11-29 16:33

Calvin promotes DRB and DRB Q3 loss is RM 300 million. I guess DRB share price should be less than AAX share price which makes profit.

2016-11-30 09:18

"3) The Latest Figures show that AirAsia is having thining margin in profit

While Average fare has increased from last quarter Rm153 to Rm164

Ancillary income per pax has actually dropped from Rm48 to only Rm46

For a seat in a plane worth Rm400 million with such razor thin margin of Rm46 profit? This is even worst than using Roll Royce as Uber taxi getting Rm15 fares?

No wonder Bloomberg came out with an article saying AirAsia would be making a Loss if not for Leasing planes to subsidiaries!!"

Remember why the GMT RESEARCH titled their reports for Airasia Parent Company as "New dog, old trick" ? Because it found out that AA parent company are using its subsidiaries to lease aircrafts from parent company just to put AA in the "black" every quarter. By not doing so, AA already in the "red" for many years now.

While what we know for many years, those subsidiaries like Philippines AA, Indo AA and Thai AA been making tremendous losses every year. Just this year Thai AA returns to the black.

Besides, GMT Research pointed out that the cash flow position is trending and dwindling down to zero even BEFORE RM crashed below 1:4 against USD, and oil price slump when AA group hedged oil above USD 80 for many years.

2016-12-02 00:16

Jollibee, I urge you to read all the comments in other posts and do your own due diligence.

Calvin doesn't even know about operating lease and depreciation.

On Bloomberg article on incoming on operating lease, there is article by icon88.

I also emailed Bloomberg's writers and article editors to ask them to clarify the points raised. No reply received. Maybe I am too small fish. But my respect for them go down the hill as they don't even want to clarify.

2016-12-02 00:32

Memang benar loh!

Airasia & AAX totally bankrupted with many billion negative funds loh!

It also cannot operate on normal basis....as many borders still close loh!

Hence tough time for investors loh!

Better sell & switch to plantation lah!

2022-05-29 10:09

Post a Comment

Featured Posts

Latest Videos

.png)

Apps

Top Articles

2

Koon Yew Yin's Blog

3

4

Koon Yew Yin's Blog

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

MuttonCurry

Dun be overly concern by a used car salesman wannabe FA/TA. The cash and results are real enuff. Even the great buffet start to invest in airline .... something that he has not done for many decades.

If his airline investment works out ... there will be other big timers who may eye AA/AAX. Current problem is USD/MYR pair ... invest if your horizon is 1 month

2016-11-28 11:10