THE INVESTMENT APPROACH OF CALVIN TAN

BPLANT PRIVATISATION NEWS OUT! AND COMPARE BPLANT'S VALUE WITH PAST PRIVATISED STOCKS: KULIM, KWANTAS, IJMPLANT & TMAKMUR, Calvin Tan

calvintaneng

Publish date: Thu, 24 Aug 2023, 06:30 AM

calvintaneng

0 1,854

Hi Guys,

I have An Investment Approach I which I would like to all.

I have An Investment Approach I which I would like to all.

Dear Friends of i3 Forum,

What an exciting time for all Investors of Bplant. Finally it is going to be suspended today for Privatisation News from KLK.

We will now compare previous Privatisation of Palm Oil Shares

Namely:

KULIM

KWANTAS

IJM PLANT

& TMAKMUR

But first look at the News from THEEDGEDAILY

Our comments are highlighted in Blue

See

KLK to buy major stake in Boustead Plantations from LTAT, followed by MGO

KLK to buy major stake in Boustead Plantations from LTAT, followed by MGO

24 Aug 2023, 12:53 am

KUALA LUMPUR (Aug 24): Kuala Lumpur Kepong Bhd (KLK) is believed to be buying a 33% stake in Boustead Plantations Bhd from Lembaga Tabung Angkatan Tentera (LTAT), according to sources.

Sources told The Edge that LTAT will retain a 35% stake in Boustead Plantations.

LTAT’s stake sale comes on the heels of the privatisation of Boustead Plantations' parent company — Boustead Holdings Bhd — two months back. Boustead Holdings is the single largest shareholder of Boustead Plantations with a 57.42% stake, followed by LTAT with a 10.59% stake. Collectively, LTAT owns a 68% stake in Boustead Plantations prior to the share disposal.

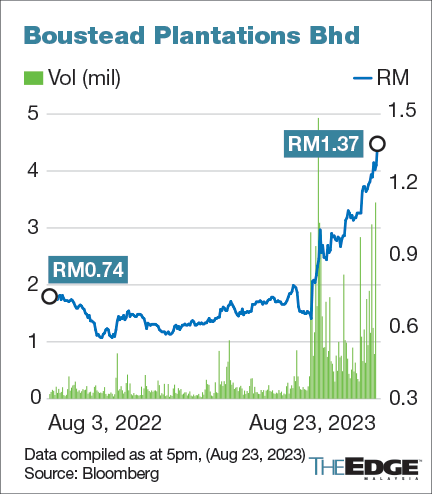

(Only 32% not owned by LTAT and since Others in Bplant Top 30 owns another 10% there is only 22% in free float or only 484 million shares being traded in the open market. Yesterday total shares of Bplant traded was 34.4 million which is about 7.1% and no wonder Bplant shot up by another 9 sen to close at Rm1.37

Upon completion of the deal, KLK is obliged to make a mandatory general offer (MGO) for Boustead Plantations, whose share price hit a record high of RM1.37 on Wednesday (Aug 23).

Boustead Plantations’ share price has staged a strong rebound from a low of 64 sen on June 8. It has more than doubled within three months to RM1.37 on Wednesday, which was higher than its net assets per share of RM1.30 as at March 31, 2023.

(Please note: The Assets of Bplant has not been revalued and updated yet) Later see our comments on Ijm Plant to compare

Closing at RM1.37, Boustead Plantations was valued at RM3.068 billion, and at a price-to-earnings ratio of 18.56 times. Dividend yield stood at 5.95%.

Boustead Plantations has suspended the trading of its shares on Thursday (Aug 24). In a filing with Bursa Malaysia, it said the trading suspension is pending on material announcement.

Boustead Plantations owns 42 operating oil palm plantation estates, including 16 plantation estates in Peninsular Malaysia, as well as 26 in Sabah and Sarawak, and 10 palm oil mills, comprising three mills in Peninsular Malaysia, five in Sabah and two in Sarawak.

Its latest annual report stated that 72,300 ha of the group’s landbank is utilised for oil palm cultivation, representing 74% of its total landbank of 97,400 ha. This consists of 23,300 ha in Peninsular Malaysia, 38,700 ha in Sabah and 10,300 ha in Sarawak.

On its financial front, Boustead Plantations reported an 89% drop year-on-year in its first quarter ended March 31, 2023 (1QFY2023). It attributed substantial earnings contraction to lower palm product prices and the adverse impact of fresh fruit bunches valuation.

Its net profit shrunk to RM5.22 million from RM435.16 million in 1QFY2022, while revenue shed 38% to RM199.74 million from RM324.16 million.

As at end-March, Boustead Plantations had short term borrowings of RM451.9 million and long-term borrowings of RM379.7 million. Cash and bank balances stood at RM99.2 million.

(Bplant has borrowings of Rm830 Million and less cash Rm99 mil: it has a debt of Rm731 Millions (about the same amount of debt like Thplant)

Third acquisition by KLK

Boustead Plantations will be the third major acquisition by KLK and its parent company Batu Kawan Bhd within three years.

To recap, Batu Kawan took over Chemical Co of Malaysia Bhd (CCM) in March 2021 at the peak of the Covid-19 pandemic. KLK then made an offer to buyout IJM Plantations Bhd, including IJM Corp Bhd’s 56.2% stake in IJM Plantations.

(KLK also bought over Ijm Plant from Ijm Corp for Rm3.10 last year)

Batu Kawan bought 56.32% of CCM from Permodalan Nasional Bhd and undertook an MGO for the remaining shares it did not own in the chemical and polymer manufacturer. The RM519.86 million deal strengthened Batu Kawan’s market position as a chlor-alkali chemical manufacturer.

So now we know KLK already taken over Chemical Co of Malaysia (CCM) & Ijm Plant. And Bplant will be its 3rd acquisition

Why is KLK so bullish while All The Research Houses in Malaysia (Except UOB) are neutral?

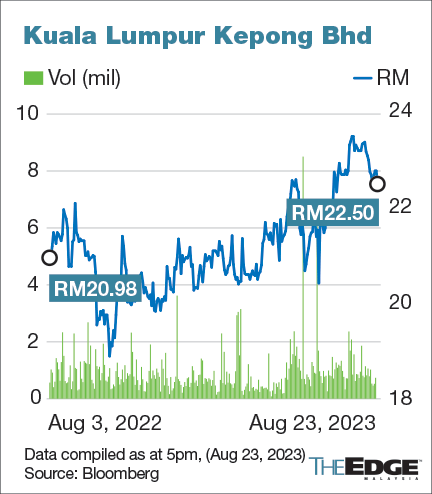

KLK has been growing from strength to strength since listing and now a Blue Chip Plantation Stock over Rm20.00

So we SHOULD FOLLOW KLK THE PALM OIL VETERAN & PROVEN EXPERT RATHER THAN TAKING ADVISE FROM OTHER ANALYSTS SITTING IN THEIR OFFICE COCOONED IN THEIR ARM CHAIRS WITHOUT ANY REAL LIFE EXPERIENCE

Ok, let's move on!

And these were the Privatisations of Past Palm Oil Cos listed (now delisted) in KLSE

1. KULIM (Refer to Bursa Official Webpage)

Our buy call for Kulim was Rm2.50

JCORP took Kulim private to do 2 New Townships in Pengerang

There was a repurpose of Palm oil Estates into Housing

And JCORP paid extra Rm1.60 to buy Kulim at Rm4.10 from Rm2.50 (Very generous indeed)

Now last two qtr results of Kulim were both negatives

Don't believe?

Then see these

SUMMARY OF KEY FINANCIAL INFORMATION31 Dec 2015 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 31 Dec 2015 | 31 Dec 2014 | 31 Dec 2015 | 31 Dec 2014 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 300,729 | 283,633 | 1,487,347 | 1,095,158 |

| 2 | Profit/(loss) before tax | 2,116 | 23,261 | 162,506 | 95,533 |

| 3 | Profit/(loss) for the period | -32,736 | 42,843 | 1,417,519 | 308,441 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | -35,980 | 10,054 | 1,410,263 | 164,303 |

| 5 | Basic earnings/(loss) per share (Subunit) | -2.80 | 0.77 | 109.78 | 12.55 |

| 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.38 | 0.00 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 3.8600 | 3.0300 | ||

LOSS of -2.8 sen

SUMMARY OF KEY FINANCIAL INFORMATION31 Mar 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 31 Mar 2016 | 31 Mar 2015 | 31 Mar 2016 | 31 Mar 2015 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 404,030 | 268,170 | 404,030 | 268,170 |

| 2 | Profit/(loss) before tax | -19,447 | 24,584 | -19,447 | 24,584 |

| 3 | Profit/(loss) for the period | -23,526 | 1,351,519 | -23,526 | 1,351,519 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | -36,349 | 1,360,502 | -36,349 | 1,360,502 |

| 5 | Basic earnings/(loss) per share (Subunit) | -2.87 | 102.48 | -2.87 | 102.48 |

| 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.38 | 0.00 | 0.38 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 3.8200 | 3.8800 | ||

Another loss of 2.87 sen for Kulim final results before delisting

SO THE PRIVATISATION OF KULIM AT SUCH HIGH PRICES CLEARLY DEMONSTRATE TO US THE EARNINGS ARE NOT ONLY THE PRIMARY REASON FOR SHARE PRICE VALUE OR PERFORMANCE

VALUE IS VALUE IRRESPECTIVE OF CURRENT EARNINGS

PLEASE GET THIS STRAIGHT!

2. KWANTAS

KWANTAS was 50 sen & to the surprise of all Majority Owners offered Rm1.65 to take over KWANTAS

See the second last results

SUMMARY OF KEY FINANCIAL INFORMATION30 Sep 2020 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 30 Sep 2020 | 30 Sep 2019 | 30 Sep 2020 | 30 Sep 2019 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 259,129 | 203,766 | 259,129 | 203,766 |

| 2 | Profit/(loss) before tax | 8,106 | -9,792 | 8,106 | -9,792 |

| 3 | Profit/(loss) for the period | 6,606 | -10,292 | 6,606 | -10,292 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 7,042 | -9,912 | 7,042 | -9,912 |

| 5 | Basic earnings/(loss) per share (Subunit) | 2.26 | -3.18 | 2.26 | -3.18 |

| 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 3.6359 | 3.6108 | ||

It made 2.26 sen profit (mediocre)

Look again the final qtr result before being delisted

SUMMARY OF KEY FINANCIAL INFORMATION31 Dec 2020 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 31 Dec 2020 | 31 Dec 2019 | 31 Dec 2020 | 31 Dec 2019 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 293,489 | 252,729 | 552,618 | 456,495 |

| 2 | Profit/(loss) before tax | 29,352 | -6,237 | 37,458 | -16,029 |

| 3 | Profit/(loss) for the period | 26,352 | -6,837 | 32,958 | -17,129 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 26,873 | -6,229 | 33,915 | -16,141 |

| 5 | Basic earnings/(loss) per share (Subunit) | 8.62 | -2.00 | 10.88 | -5.18 |

| 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 3.7239 | 3.6108 | ||

A nice 8.62 sen profit

Now all the Estates of KWANTAS are located in Sabah & fully revalued plus it has several chemical factories in China

We have no way of knowing the exact intrinsic value of KWANTAS as those chemical assets are in China

In any case to give Rm1.65 (when it was 50 sen) is extremely generous of Majority Owners

3. IJM PLANT

SUMMARY OF KEY FINANCIAL INFORMATION30 Sep 2021 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 30 Sep 2021 | 30 Sep 2020 | 30 Sep 2021 | 30 Sep 2020 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 299,782 | 211,370 | 571,497 | 417,355 |

| 2 | Profit/(loss) before tax | 132,422 | -2,430 | 215,539 | 112,868 |

| 3 | Profit/(loss) for the period | 103,942 | -3,201 | 165,728 | 84,723 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 101,040 | -1,040 | 161,100 | 81,076 |

| 5 | Basic earnings/(loss) per share (Subunit) | 11.47 | -0.12 | 18.29 | 9.21 |

| 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 1.7400 | 1.6300 | ||

Above is the last and final Results of IJM PLANT before saying Sayonara to us.

It reported a decent profit of 11.47 sen

But look at its NAV(NTA)

It was Rm1.74

And yet KLK took over at Rm3.10

That means that KLK sees IJMPLANT worth more than Rm1.74 in Value

A check into IJM PLANT shows its Palm Oil Estates are located in Sabah, East Kalimantan & Sumatra(Exactly the same for TSH Resources located in the same regions except TSH got 94,700 acres jackpot lands in Nusantara now the New Capital of Indonesia)

Ok we go see TMakmur before taking a look at Bplant's latest results

Oophs!

Tmakmur already delisted and removed from Bursa

Ok go see comments in i3 forum under Tmakmur

TANAH MAKMUR BERHAD

KLSE (MYR): TMAKMUR (5251)

WAHAHA!

OFFER FOR PRIVATIZATION INCRASED FROM RM1.80 to RM1.90

Calvin Tan Research Chun Chun Call to Buy TMakmur at Rm1.38

TMAKMUR (LAND OF PROSPERITY) NOW TAKEN PRIVATE AT RM1.90

UP A NICE 37.6%

HIP HIP HOORAY!

2016-10-26 08:28

Calvin is very happy for all here.

You all have made the right decision to buy into TMakmur for

1) Defensive quality

2) Growth

3) Above all for TMakmur's exceptionally generous dividends.

And because all here are TRUE VALUE INVESTORS YOU ARE NOW REWARDED FOR YOUR PATIENCE.

CONGRATULATIONS! CONGRATULATIONS!!

2017-02-21 22:05

tommorow at 5.00pm must say goodbye already...

2017-02-27 09:17

must say thank you to tmakmur....a very short life but worth since knowing about tmakmur...

2017-02-27 09:28

congrats calvin and all

2017-03-03 01:45

Good bye tmakmur.....it will be delisted from bursa very soon...

2017-03-04 06:35

Finally....good bye tmakmur !!!

2017-03-04 09:25

when can see the money in our acct?

2017-03-07 13:55

Received the proceeds in the bank accounts. Thank you my highness Royal Pahang for this kind bonus.

2017-03-20 20:25

Just got my mine also...Thanks to tmakmur.....Finally, we can move on.......Kindly be advised that the shares of TMAKMUR will be removed from the Official

List of Bursa Securities with effect from 9.00 a.m., Monday, 27 March 2017

2017-03-27 10:39

Very Happy New Year

Tmakmur the land of prosperity

2019-01-01 21:58

tmakmur...we miss you....

2019-04-03 13:51

OK WE NOW SEE BPLANT LATEST RESULTS

SUMMARY OF KEY FINANCIAL INFORMATION31 Mar 2023 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | |||

| CURRENT YEAR QUARTER | PRECEDING YEAR CORRESPONDING QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR CORRESPONDING PERIOD | ||

| 31 Mar 2023 | 31 Mar 2022 | 31 Mar 2023 | 31 Mar 2022 | ||

| $$'000 | $$'000 | $$'000 | $$'000 | ||

| 1 | Revenue | 199,743 | 324,156 | 199,743 | 324,156 |

| 2 | Profit/(loss) before tax | 13,471 | 509,519 | 13,471 | 509,519 |

| 3 | Profit/(loss) for the period | 3,004 | 435,546 | 3,004 | 435,546 |

| 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 5,215 | 435,158 | 5,215 | 435,158 |

| 5 | Basic earnings/(loss) per share (Subunit) | 0.23 | 19.43 | 0.23 | 19.43 |

| 6 | Proposed/Declared dividend per share (Subunit) | 1.00 | 7.30 | 1.00 | 7.30 |

| | | AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | ||

| 7 | Net assets per share attributable to ordinary equity holders of the parent ($$) | 1.3000 | 1.3300 | ||

As you can see Bplant only earn a mediocre 0.23 sen profit

And its NTA Rm1.30

Now Bplant has been chased past its Rm1.30 NTA to the high of Rm1.37

BUT REMEMBER THE WORDS OF TOK MAT WHO SAID BPLANT IS PLANTING TREES ON :A GOLD MINE"

In other words Bplant got Land Assets located in prime prime areas now ripe for developments in Peninsular as well as ideal Palm Oil Landsin Sabah and Sarawak

If KULIM with less than 150,000 acres, Tmakmur & Kwantas both less than 80,000 acres & Ijmplant about 160,000 acres are worth

Rm4.10, Rm1.90, Rm1.65 & Rm3.10 respectively with smaller acreages plus less promising locations DO YOU THINK BPLANT'S ASSETS ARE INFERIOR TO THEM OR SHOULD BPLANT BE ACCORDED A MORE DECENT PRIVATISATION PRICE?

In time Past Harrison wanted to take it private at Rm1.30 but one guy called Peter from USA kept buying and buying till he had more than 10% of Harrison & averted privatisation. Then Harrison stay listed & crossed Rm10.00 a blue chip. Even today Harrison at Rm8.62 is far far higher than Rm1.30

Another one was Hong Leong Capital for which HL Bank offered Rm1.71.However, one major shareholder blocked it & then Hl Capital share price shot up above Rm10.00

Today Hl Cap is still Rm5.43 or 200% more than offer price

So let us keep finger crossed that Bplant will at least get a fairly good privatisation price.

With Kind Regards

Calvin Tan

Please buy or sell after doing your own due diligent study and investigation

More articles on THE INVESTMENT APPROACH OF CALVIN TAN

JCY (5161) Posted a 2nd Qtr of Good Profits: Showing a Clear Sign of A Turnaround, Calvin Tan

Created by calvintaneng | Aug 23, 2024

TSH RESOURCES AUGUST 2024 RESULTS: A Look at its Latest Balance Sheet, Calvin Tan

Created by calvintaneng | Aug 22, 2024

UNDERSTANDING DIFFERENT FORMS OF VALUE IN VALUE INVESTING, Calvin Tan

Created by calvintaneng | Aug 03, 2024

Discussions

1 person likes this. Showing 23 of 23 comments

Ok better stay listed like Harrison & Hold Leong Capital

Who knows?

Bplant might one day cross Rm10.00

2023-08-24 06:49

Very Good Write up Calvin! Thanks for sharing.

Calvin is really a Smart Investor who can smell money from miles away!

We are happy to have you with us. YOU are our GOLD MINE!

2023-08-24 10:47

With the latest acquisition KLK acreage in Malaysia and Indonesia now is about :

KLK - 300,000 hectares

IJM - 60, 979 hectares

BPPlant - 97,400 hectares

Well Done KLK and Batu Kawan!

We now have secured a GOLD MINE!

To Our Success !

Meow Meow Meow

2023-08-24 10:47

Price offered by KLK seems a bit low at RM 1.55/share, for 33%, since some prime land have not been revalued. Bplant will still remain listed since BHldg will still hold 35 %. Can it be like Ewein , went up to double the Offer Price, since amount of shares in free float will be quite small ?

2023-08-24 15:13

Posted by Mabel > 4 hours ago | Report Abuse

Very Good Write up Calvin! Thanks for sharing.

Calvin is really a Smart Investor who can smell money from miles away!

We are happy to have you with us. YOU are our GOLD MINE!

Thank you Mabel

2023-08-24 15:46

Posted by investor77 > 34 minutes ago | Report Abuse

Price offered by KLK seems a bit low at RM 1.55/share, for 33%, since some prime land have not been revalued. Bplant will still remain listed since BHldg will still hold 35 %. Can it be like Ewein , went up to double the Offer Price, since amount of shares in free float will be quite small ?

correct

Klk should have offered a better price for Bplant. However, KLK is overstretched after buying Chemical Co (CCM) & Ijm plant

If Bplant should stay listed KLK can do wonders to make it a great co

Under KLK Bplant has the potential to be a blue chip

2023-08-24 15:50

KLK down 30 sen today upon BP Plant privatisation news. If I EPF fund manager will sell KLK heavily.

2023-08-24 15:58

chamlo got buy bplant at 57 sen?

If not chamlo is you

See

https://klse.i3investor.com/web/blog/detail/www.eaglevisioninvest.com/2021-04-12-story-h1563301593-PALM_OIL_JEWEL_BPLANT_OR_BOUSTEAD_PLANTATION_5254_BPLANT_HAS_DEEP_VALUE

2023-08-24 16:02

Integrity. Intelligent. Industrious. 3iii (iiinvestsmart)$â¬Â£Â¥

>>>

Posted by calvintaneng > 25 minutes ago | Report Abuse

Posted by Mabel > 4 hours ago | Report Abuse

Very Good Write up Calvin! Thanks for sharing.

Calvin is really a Smart Investor who can smell money from miles away!

We are happy to have you with us. YOU are our GOLD MINE!

Thank you Mabel

>>>

😀

He smelt huge profits in Netx in 2019 too.

😀

2023-08-24 16:13

Only Netx Calvin smell? How about TalamT, TSH and many more?

Integrity. Intelligent. Industrious. 3iii (iiinvestsmart)$â¬Â£Â¥

>>>

Posted by calvintaneng > 25 minutes ago | Report Abuse

Posted by Mabel > 4 hours ago | Report Abuse

Very Good Write up Calvin! Thanks for sharing.

Calvin is really a Smart Investor who can smell money from miles away!

We are happy to have you with us. YOU are our GOLD MINE!

Thank you Mabel

>>>

😀

He smelt huge profits in Netx in 2019 too.

😀

4 hours ago

2023-08-24 20:58

SEE

TSH IS NOW IN PRINCIPLE DEBT FREE & CASH RICH

VERY HEALTHY AND AT ITS BEST STATE

2023-08-24 21:06

Finally

Bplant in Top volume and reached Rm1.50

Time to buy laggards like Tsh, Thplant and Jtiasa while they are still in pessimism

Bplant at 57 sen was during pessimism

2023-08-25 09:59

This week has been a fantastic week. 1st we have the marriage between Mabel Batu Kawan and CCM, 2nd we have Mabel KLK and IJM Plantation, 3rd we have Mabel KLK and BP Plantation and yesterday, 4th we have Mabel Sime Darby and UMW. Perhaps next PNB will consolidate MHB and Lady Sapura. All these couples have generated interest in KLSE.

Marriage is a partnership that requires trust, communication, and compromise. It also involves sharing responsibilities, goals, and values. These are the same qualities that make a successful business. In both cases, you need to respect your partner, listen to their feedback, and work together to overcome challenges. You also need to celebrate your achievements, support each other's growth, and have some fun along the way. Marriage and business are not easy, but they can be rewarding if you apply the wisdom of love, loyalty, and leadership.

To Our Success!

Meow Meow Meow

2023-08-25 10:03

WHY BPLANT WILL PERFORM EXCEPTIONALLY WELL WITH THE EXPERTISE OF KLK IF IT STAYS LISTED, Calvin Tan

https://klse.i3investor.com/web/blog/detail/www.eaglevisioninvest.com/2023-08-26-story-h-241833228-WHY_BPLANT_WILL_PERFORM_EXCEPTIONALLY_WELL_WITH_THE_EXPERTISE_OF_KLK_IF

2023-08-26 07:07

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

.png)

Apps

Top Articles

1

Mercury Securities Research

2

The Alpha Trader

4

5

save malaysia!

6

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

calvintaneng

Post removed.Why?

2023-08-24 06:46