Icon8888 Gossips About Stocks

(Icon) Can-One Bhd - Can Buy Or Cannot Buy ?

1. Introduction

Canone used to trade as high as RM5.06 few months ago. Now it is trading at RM3.35, down by 34%.

Its weak March 2016 quarterly profit is one of the major reason for the sell down. But is that quarter's proifit really that bad ?

My objective for this article is very clear and simple - I want to put its recent historical P&Ls in a table, and make adjustments to the figures by excluding all exceptional items. By doing so, I want to find out how much the group has actually been making over the past few years, and make a decision on whether it is a good buy at current price.

I will not be going into details its business, cash flow, etc in this article. Certain forum members have written about Canone extensively. Please refer to those articles if you are interested in finding out more.

http://klse.i3investor.com/blogs/rarecharms/91402.jsp

http://klse.i3investor.com/blogs/canone/92357.jsp

http://klse.i3investor.com/blogs/rarecharms/93026.jsp

http://klse.i3investor.com/blogs/canone/95148.jsp

http://klse.i3investor.com/blogs/ivsastockreview/98589.jsp

2. Historical Profitability

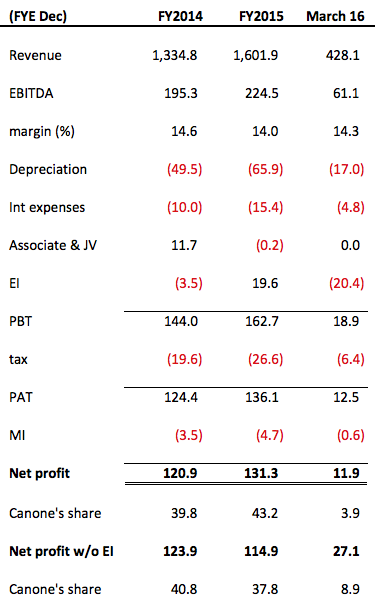

2.1 Kian Joo

If you strip out the exceptional items, Kian Joo's profitability is quite stable at about RM110 mil per annum.

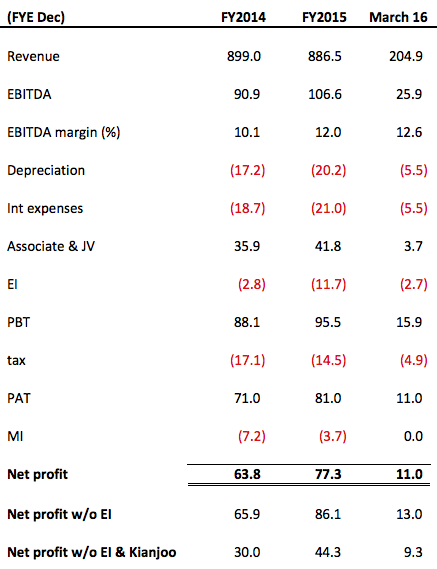

2.2 Canone

Canone reported net profit of RM11 mil in March 2016 quarter. I believe that is not reflective of its actual earning potential.

So how much can Canone make in a normal year ?

2.3 Financial Model

First of all, we need to determine how much Kian Joo can make in a normal year. We have already done that in Section 2.1 above - Kian Joo should make about RM110 mil per annum. Canone's 32.9% share is approximately RM36 mil per annum.

Secondly, we need to determine how much profit Canone's own operation (tin manufacturing as well as dairy) can generate. If you look at the table in Section 2.2 above, those divisions generated net profit of RM30 mil and RM44 mil for FY2014 and FY2015 respectively. Lets take the average. That will give you RM37 mil per annum.

Based on the foregoing, it seemed that Canone's core earning is approximately RM36 mil + RM37 mil = RM73 mil.

Based on 192 mil shares, EPS should be approximately 38 sen.

3. Concluding Remarks

(a) In this article, I built a crude financial model by playing with historical figures. I arrived at core earnings of RM73 mil.

(b) Is this "earning prediction" ? Not really. I think it is more a "pro forma" figure. I derived the core earning without making any assumption of growth rate, profit margin, etc. All I have done is to exclude the exceptional items.

(c) Is the RM73 mil figure reliable ? That depends on how you look at Canone group's business fundamentals.

If you believe that Canone's business is matured, the RM73 mil will be reflective of its future earnings.

However, if you believe that Canone has huge potential to grow, or that Canone's cost structure is sensitive to fluctuation of raw material price, you should throw the financial model out of the window.

(d) I believe that Canone group's business is quite matured. As a contract manufacturer, it's profit margin should be quite stable. As a result, the pro forma figure of RM73 mil is good enough for me.

Based on EPS of 38 sen and PER of 12 times (for F&B companies), I ascribe a fair value of RM4.56 to the stock.

The PER of 12 times is plucked from the air. You can disagree with me and derive a more "authoritative" figure by using financial tools such as EV/EBITDA, Discounted Cashflow, Dividend Discount Model, Sum of Parts Valuation, etc.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

1 person likes this. Showing 16 of 16 comments

Short term wise, RM3.80 will be critical, if can break, then upward trend will most likely prevail

2016-06-29 16:17

The suggested financial model is sufficiently easy for those not financial savvy to understand. Thanks Icon.

2016-06-29 16:40

Canone is a good company. But speakup will skip cos Mr Koon is already heavily in it. When Mr Koon promotes a stock, it is normally time to sell.

2016-06-30 09:41

FA aside, there still no clear sign it is bottoming out and changing to uptrend with building volume support.

2016-06-30 14:18

As long as its can't make much money and have high debt, the share is not worth to hold.

2016-07-01 01:01

value creation can come in many forms......

sale of Kian Joo

sale of milk division

restructuring with listing of milk division

sale of can division to Kian Joo

as the market PE for food consumables - milk is 15 -25 much higher than the PE 8 to 12 for can division by restructuring and focusing on milk division will be re-rated to $6.

of course, there is previous talk of KWAP taking a stake in the milk division at PE 20, the share will be rerated once the deal is confirmed.

The share is much over sold at current price.

Milk division profits FY 2015 is $ 62 million....and growing fast.

2016-07-01 09:50

while waiting for the restructurings and value creations, the share is traded at its NTA and a PE below 10........hahah

2016-07-01 09:56

Icon8888, based on EPS of 38 sen and PER of 12 times (for F&B companies), I ascribe a fair value of RM4.56 to the stock.

2016-11-22 11:49

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-23 16:40:00

EMA 5

5 Mins

SELL

2024-07-23 16:35:00

ADX

5 Mins

SELL

2024-07-23 16:30:00

ADX

10 Mins

SELL

2024-07-23 16:30:00

EMA 5

5 Mins

BUY

2024-07-23 16:25:00

ADX

5 Mins

BUY

Apps

Top Articles

1

BFM Podcast

2

Koon Yew Yin's Blog

3

CGS-CIMB Research

Genting Plantations - Proposed Land Acquisition in Indonesia

5

save malaysia!

6

Koon Yew Yin's Blog

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

ksng0307

Safety wise, buy when it breaks 3.50

2016-06-29 16:12