Icon8888 Gossips About Stocks

(Icon) MKH - Strong Earning Momentum

1. Introduction

MKH recently reported two consecutive quarters of strong earnings.

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS |

|---|---|---|---|---|---|---|

| 2016-09-30 | 2016-03-31 | 322,231 | 55,379 | 13.20 | - | 2.8300 |

| 2016-09-30 | 2015-12-31 | 266,365 | 61,570 | 14.68 | 7.00 | 2.7100 |

| 2015-09-30 | 2015-09-30 | 348,710 | 24,411 | 5.82 | - | 2.6300 |

| 2015-09-30 | 2015-06-30 | 255,838 | 20,886 | 4.98 | - | 2.5400 |

| 2015-09-30 | 2015-03-31 | 229,720 | 10,904 | 2.60 | - | 2.4900 |

| 2015-09-30 | 2014-12-31 | 207,634 | 30,129 | 7.18 | 8.00 | 2.4600 |

Are those earnings real ? Are they sustainable ? Let's take a look.

2. Background Information

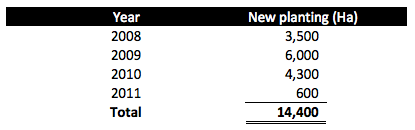

MKH is principally involved in property development. In 2008, it ventured into oil palm plantations in Kalimantan, Indonesia. It completed planting the entire 14,400 Ha by 2011.

Based on 420 mil shares and latest price of RM2.55, market cap is RM1.07 billion. Based on past twelve months aggregate net profit of RM162 mil, historical PER is 6.6 times.

The group has net assets of RM1.2 billion, loans of RM827 mil and cash of RM296 mil. As such, net gearing is 0.44 times.

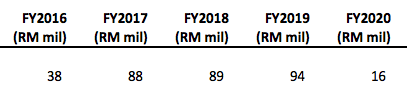

Out of RM827 mil borrowings, RM326 mil is denominated in US Dollars (which explained why the group incurred huge forex losses in past few years). The USD borrowings were used to finance the group's plantation capex in the past few years.

According to FY2015 annual report, the USD borrowings are repayable over 5 tranches as follows :-

As trees are now matured and producing FFBs, the group should be very comfortable servicing its debt obligations going forward.

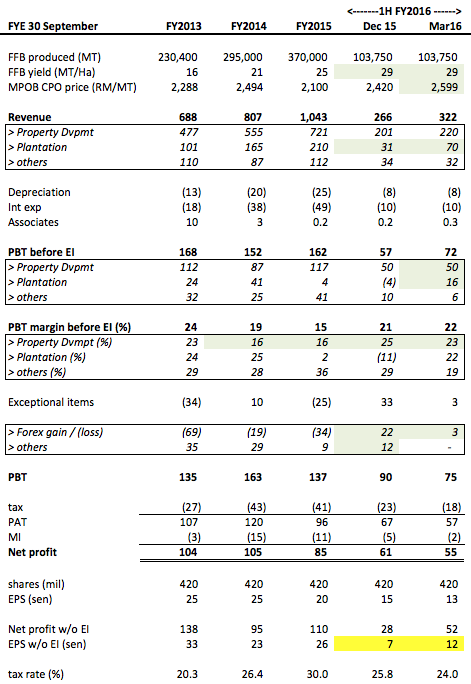

3. Historical Profitability

Key observations :-

(a) Plantation division reported PBT of RM20 mil in March 2016 quarter. However, there was net forex gain of RM3 mil. Excluding that item, core PBT would be RM17 mil per quarter.

(b) Property division generated PBT of RM62 mil in December 2015 quarter. However, there was a government grant of RM12 mil. Excluding that item, core PBT would be RM50 mil. That translated into PBT margin of 25%. It is not clear whether this high profit margin is sustainable as in FY2014 and FY2015, property division's PBT margin was only 16%.

(c) Property division generated PBT of RM50 mil in March 2016 quarter. That translated into PBT margin of 23%. Same as above, it is not clear whether this high profit margin is sustainable.

(d) After stripping off the forex gain and government grant, MKH's core EPS for 1H FY2016 is 19 sen (being 7 sen + 12 sen).

(e) The following factors will determine whether the recent two quarters' strong profitability can be sustained going forward :-

(i) Property division - It is unclear how much progress billing will be booked in in the coming quarters. However, the group has unbilled sales of RM800 mil plus and will be launching closed to RM1 billion new projects this year.

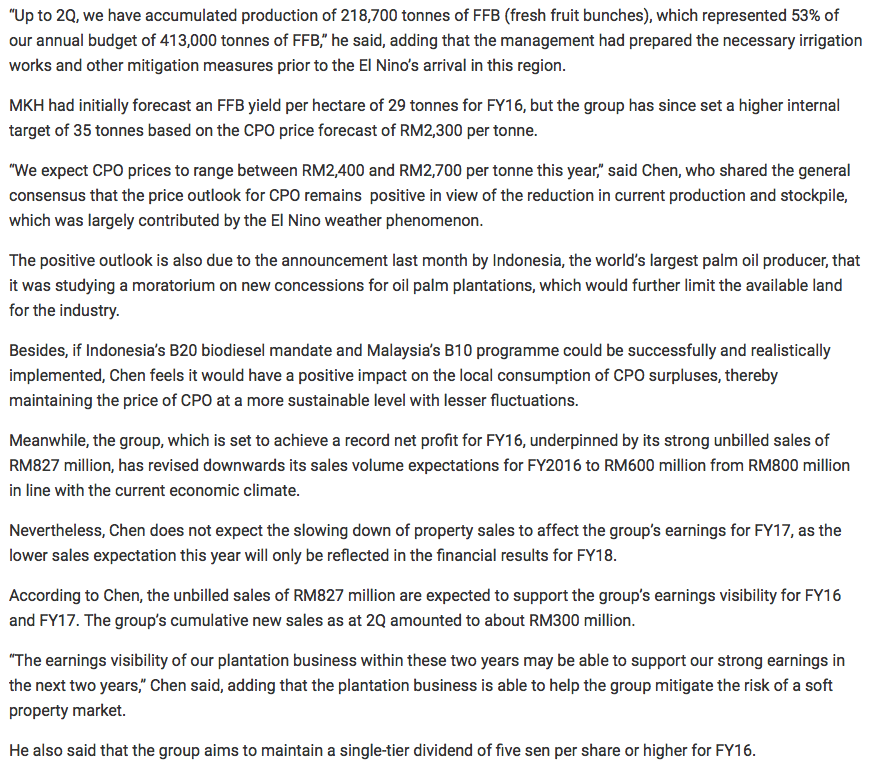

(ii) FFB yield - At average age of 7 years, the group's palms are still growing. FFB yield is expected to continue to increase over next few years.

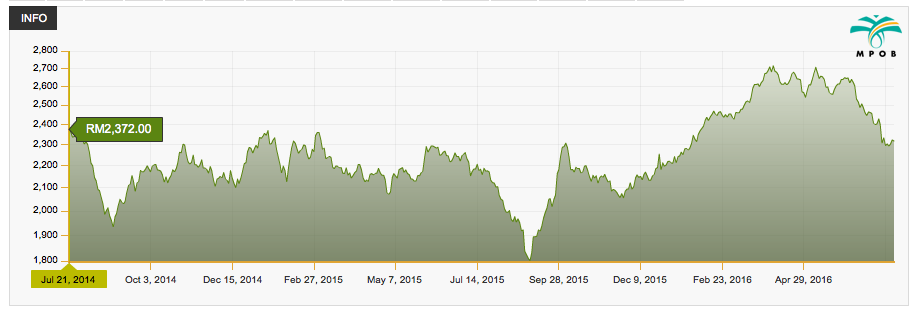

(iii) CPO price - During the period from April until June 2016, average CPO price was RM2,599 per MT. This is higher than the March 2016 quarter's RM2,420 per MT.

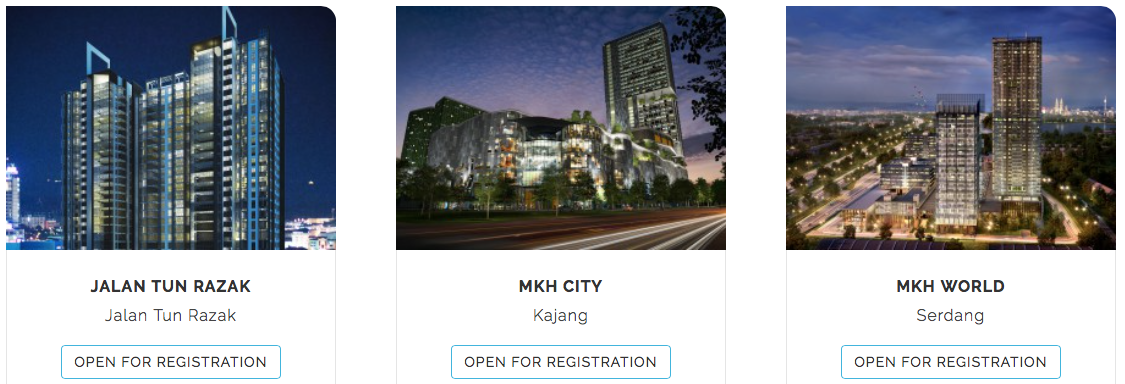

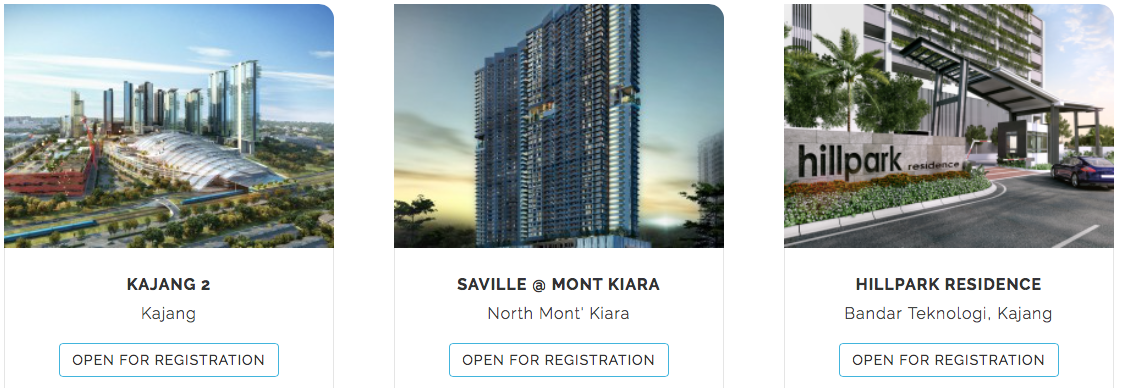

4. Property Projects

The following are the group's ongoing projects :-

I notice that they are mostly located in popular and matured residential areas.

5. Super Trees

MKH's plantations are located at Kota Samarinda, East Kalimantan. The region was not affected by the recent El Nino. As such, MKH enjoyed the best of both world - high yield + high CPO price during 1H 2016.

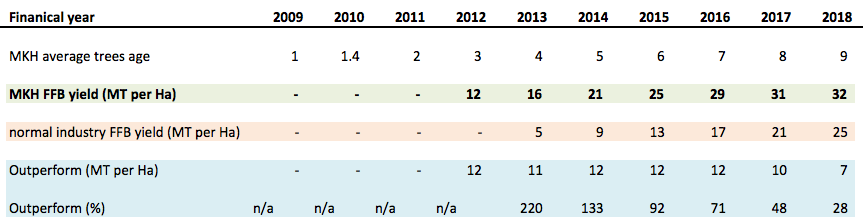

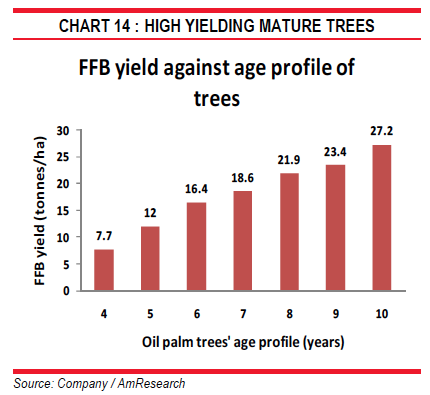

MKH's Kalimantan plantations have exceptionally high FFB yield. A comparison of their yield with industry average is as set out below :-

As shown in table above, MKH's yield are SUBSTANTIALLY higher than industry average.

For example, in 2016, with trees at 7 years old, the group's FFB yield is expected to reach an astounding 29 MT per Ha. To get a feel of how good those yields are, just compare it with Uncle Koon's blue eye boy, Jayatiasa. According to this analyst report published by AmResearch in January 2014, Jayatiasa's 7 years old trees are expected to produce 18.6 MT FFB per Ha.

MKH did not explain why its yield is so impressive. However, I did hear before of such cases of exceptionally high yield in Indonesia, especially in region of fertile volcanic soil. If anybody knows the answer for MKH, please drop me a note.

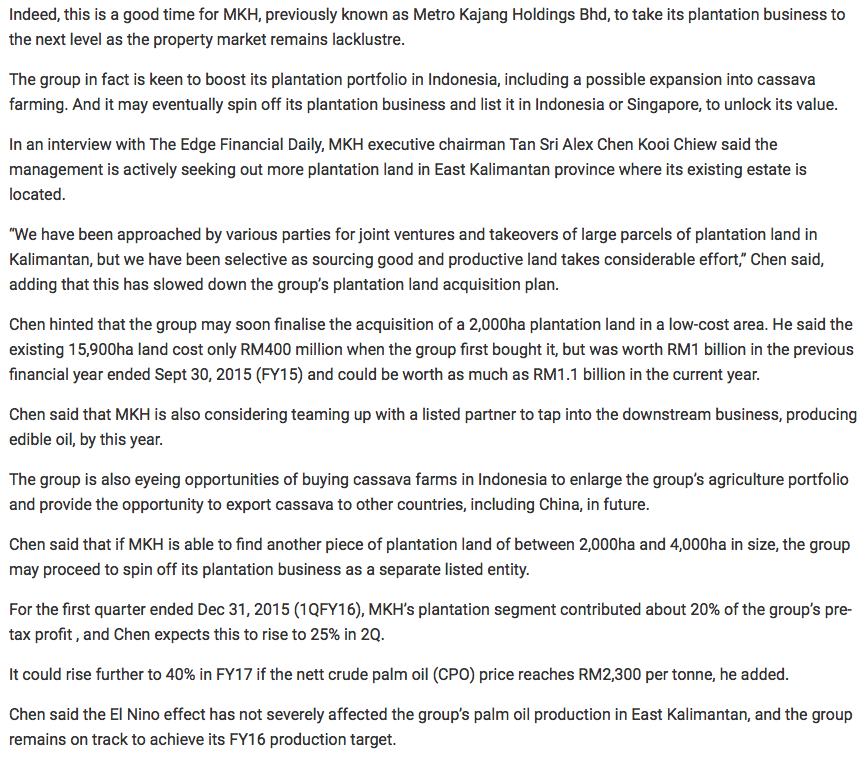

6. Potential Listing Of Plantation Division Soon ?

In an interview with The Edge in May 2016, the company's Executive Chairman mentioned that they might list the plantation division if they were able to secure another 2,000 to 4,000 Ha of plantation land.

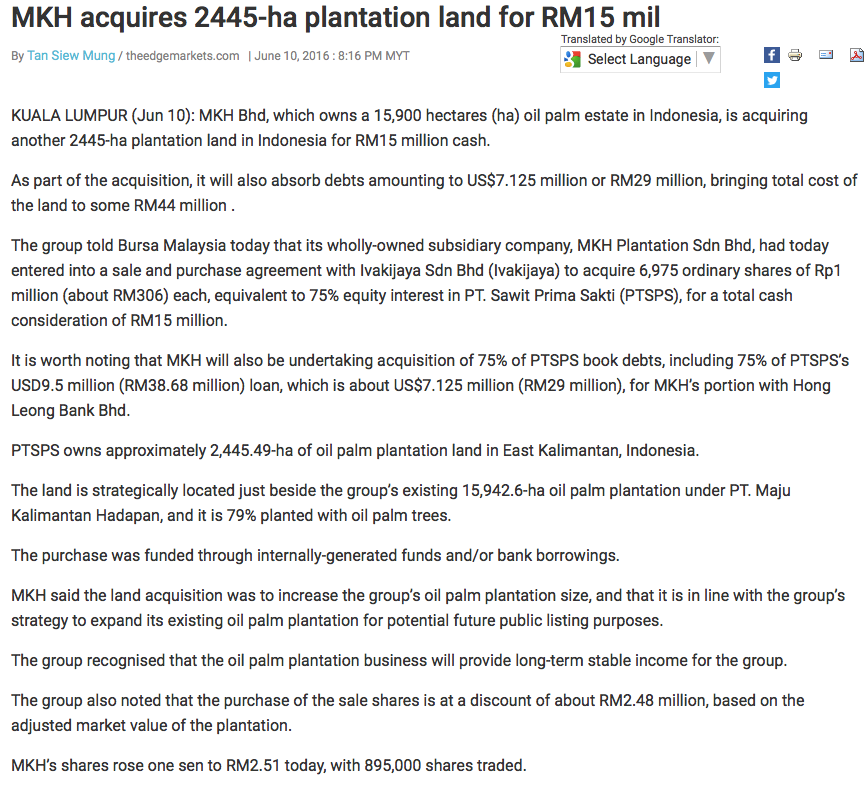

His wish came true sooner than expected. On 10 June 2016, MKH announced that it is acquiring 75% of PT Sawit Prima Sakti (PTSPS) for cash consideration of RM15 mil. PTSPS owns 2,445 Ha of plantation land in East Kalimantan.

Does that mean that the listing will happen very soon ? Let's just wait and see.

7. Concluding Remarks

(a) MKH attracted my attention because it has performed well in recent two quarters.

(b) Its plantation division generated core PBT of RM17 mil in latest quarter. For discussion sake, let's assume that the same performance can be repeated in next few quarters (FFB yield expected to remain strong while June 2016 quarter CPO price is higher than that of March 2016 quarter).

Based on annualised PBT of RM68 mil, tax rate of 25% and MI of 5% (Indonesian partners), can this division deliver net profit of at least RM48 mil ?

(c) Property division generated core PBT of RM50 mil in latest quarter. If annualised, full year PBT will be RM200 mil. However, this could be too aggressive. To be prudent, I prefer past 3 years average PBT of approximately RM110 mil.

Based on 75% tax rate, can this division deliver net profit of RM82 mil ?

(d) The group's other divisions (investment properties, trading, etc) generated PBT of approximately RM25 mil per annum in the past.

Based on 25% tax rate, can those divisions deliver net profit of RM19 mil ?

(e) By putting all the above figures together, I arrived at theoretical net profit of RM149 mil. Based on 420 mil shares, EPS is approximately 35 sen. Based on latest price of RM2.55, prospective PER of 7.3 times ?

(f) Can the above EPS be achieved ? Nobody knows. I guess we can only find out over time.

Have a nice day.

Appendix - The Edge Article Dated 23 May 2016

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

7 people like this. Showing 26 of 26 comments

MKH received the government grant RM11.7 million in Q1 December 2015 only. Don't think it receives again in Q2 March 2016. So the PBT margin in Q2 should be higher than 17% as mentioned.

2016-07-20 17:41

The Chairman had clearly stated that they had good irrigation system in place, as reported by the Edge dated 23 May 2016, to mitigate the adverse impact of El Nino. In Perlis which is traditionally the dry zone of Malaysia, Felda was able to achieve a 30% increase in FFB on a traditionally 30% lower yielding zone of Kedah, by experimenting with irrigation on an experimental basis. Not surprising if MKH can harness the natural advantage of streams and rivers passing thro on higher terrain without additional cost, in an environment of fertile volcanic soil

2016-07-20 17:47

Not at all Icon sifu. Finally its the cost that matters. Irrigation without incurring high cost, why not ??

2016-07-20 18:06

This was what announced in 2008 when MKH acquired the land.

"The Land covers an area of approximately 15,942.60 hectares. The Land is generally flat with very slight undulation and the soil and climate conditions are suited for oil palm cultivation. The Land has 2 small rivers passing through and is ideal as a source of water for the future oil processing mill. In addition, the main river known as Sungai Mahakam provides an ideal transportation mode to ship out the crude palm oil. Currently, the Land comprises mainly of ‘belukar’ and shrubs and progressive clearing of the Land for the planting of oil palm trees is in progress. Currently, approximately 80 hectares of oil palm nursery has been established.

PT Khaleda has also engaged a professional plantation managing firm to assist in the plantation development of the Land in addition to its own management team comprising of personnels with many years of experience in the oil palm plantation sector in Indonesia. The MKHB Group currently owns and manages several hundred acres of oil palm plantation in Peninsular Malaysia with its first venture in year 1995. In addition, the Executive Chairman of MKHB has more than 18 years of experience in managing oil palm plantation."

2016-07-20 18:06

Chen has learned Cultivation of Oil Pam from KL Kepong. The existing land owned by MKH if I have not mistaken was introduced by KLK . That is why its yield is high.

2016-07-20 20:31

Many of the MKH land bank are closed to the stations of MRT1 and MRT2. These include Jalan Tun Razak project, Saville Cheras, Jalan Bukit project and MKH City. Furthermore, Kajang 2 and its adjacent, Kajang South (new land bank)are in very good location and will be well received. During slow market like now, MKH also can launch their more affordable products like Bandar Teknologi,Saville @ Kajang n Saville @ D'Lake. Therefore, the company is still doing very well at this time.

The management of MKH are people with integrity. Their track record has shown that the shareholders are well rewarded for holding long term.

2016-07-20 23:15

misleading title "MKH - Strong Earning Momentum" with many question marks at the conclusion remarks. Strong company but written by Icoon8888 became questionable. Became a con company

2016-07-21 06:38

My original title was "can strong earning be sustained ?". But after getting positive feedback from readers about MKH, I decided to be more straightforward and called it "strong earning momentum", which is a fact

No intention to con your roti canai. You can keep it

Btw, if a simple thing like this irritates you, I don't think you can go very far in your life

2016-07-21 08:50

Hi Icon8888, i have been tracking this stock for several quarters, but still unable to open any position due to below reason:

1) I noticed this company USD debt in indonesia give significant impact (positive & negative) to the earning. Latest 2 quarter result has 22 million forex gain (Q1) & 5 million forex gain (Q2), coincidentally when rupiah appreciated about 6% and 4 % respectively. For Q3 (April to Jun), Rupiah did not change much. So, we can more or rest rule out the forex gain/loss. By taking out the forex impact, the core net profit for 2 quarters total at approximately 45 mil per quarter or 10.7 sen per quarter. If annualised it, will be 40 sen per year. But, there may be other factors as below.

2) i noticed the operating margin for property fluctuate a lot..in the region of 15% to 35%. This could be a significant factor.

3) For Q2 plantation segment, the "unusually" high revenue & operating profit could be due to the "stocking" up of the FFB/ CPO or the like in Q1 as indicated by the management. They may have take advantage of Q2 high CPO price and sold them, which lead to high income.

4) the recent purchase of agriculture land has further "assumed" more USD denominated debt.

5) the tree age are indeed in the high production age, but i suppose the high earning from plantation may be "normalized"

Just sharing some of my tracking data

2016-07-21 09:22

Thank you YiStock for your info and opinion. I agree the latest property profit might not be sustainable. Lets just wait and see what will be their result in coming quarters.

2016-07-21 09:25

Btw, if a simple thing like this irritates you, I don't think you can go very far in your life.

Icon8888, if simple thing you make mistake, you are not qualify to handle bigger thing, this is how i look at it. you simply cannot take comment and narrow minded

2016-07-21 09:30

there is obvious reason to put misleading title to con ppl into believing MKH by Icon8888, next he will say he never ask you to buy or sell but doing extensive promotion. this is con or not???

2016-07-21 09:40

007, he is just presenting his homework and undoubtedly these are facts indeed that the past 2 quarters posted really good results. from the charts, if the syndicates and operators behind has entered silently, it would be in the range of RM2 to RM2.50 back in 2015. there is still "meat" if you wish to chase after these "recommendation", just dun be too greedy as being the 1st to board the ship, the operators will be the first to jump ship also. ride along the tide and eject after a decent run, should be fine.

2016-07-21 10:30

Is it correct to just value a property counter by basing on its PE ratio? I thk it is wrong, it shld be PE ratio together with its RNAV(Revised Net Asset Value).

For simplified example, we assume a company just has one shophpouse that is worth RM2mil. The shophouse is able to generate income of RM200k per year in 2014

Therfore

PE ratio = 10

Market capitalisation = RM2mil (Assume 1mil shares, share price=RM2.00)

In 2016, property market is bad. The income generated drops to RM100k. Market reacted n share price drops to RM1.00 because ppl focus to its profit n PE ratio.

PE ratio = 10

Market capitalisation = RM1mil.

Just think, has the the value of the shophouse drops to RM1mil due to the lower income. It has not, the value is still RM2mil.

The big IB analysts always merely based on PE ratio to make their calls and this is totally wrong. It has make the property counters severely undervalued. That is the reason a lot of privatisation happened in these few years. To name a few,

Hunza is privatised at RM2.90 when the actual woth is RM9.00

OSK Property is privatised at RM2.00 when the actual worth is RM6.50

The major shareholders knows the actual values of their companies n they are laughing all the way to the bank.

2016-07-21 12:28

Very well said, if the property generated income to 100K from 200K, the value of property should drop accordingly to 1 miliion, not stay at 2 mils.

Let's take an old shophouse in bukit bintang previously purchase 30years ago with 100K and today the rental is 40K/month. what would be the shophouse value? I would buy at 2 mils. It's still ok, even it is very old house (the asset value equal to zero). The importance is the income generated from asset, not the value itself. Unless the owner sell the property for 2 mils. The property still worst nothing in the accounting book.

2016-07-21 16:58

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

AmInvest Research Reports

2

TA Sector Research

3

4

save malaysia!

5

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Ricky Kiat

i bought it n hold it more than 3 year after recommend by cold eye.

2016-07-20 17:11