Icon8888 Gossips About Stocks

(Icon) Borneo Oil (2) - Struck Gold Worth RM270 mil

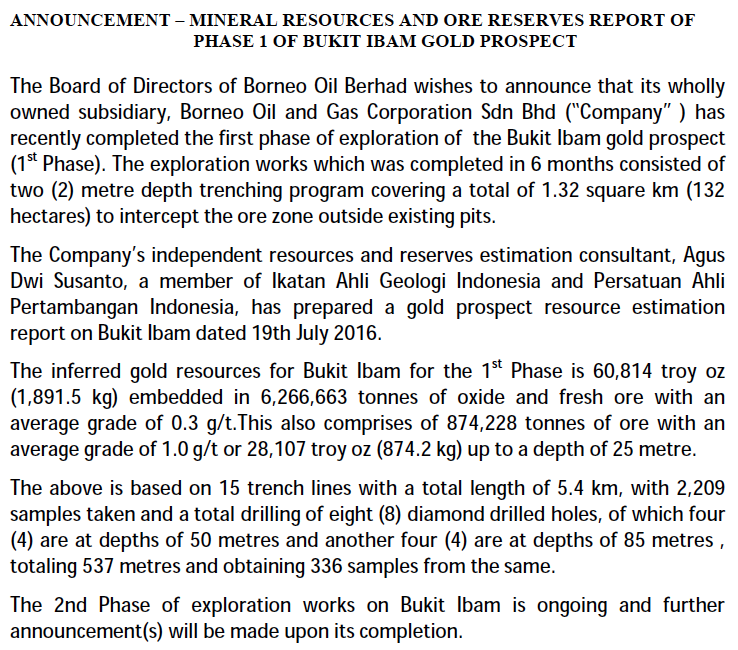

On 19 July 2016, Borneo Oil announced that its exploration activities had uncovered estimated Gold reserve of 1,892 kg in its Bukit Ibam Mine in Pahang. Based on conservative Gold price of RM150,000 per kg, the reserve is worth RM270 mil.

Upon publishing my first article, one of the major negative feedback from my readers is that Borneo Oil's existing gold inventories might have been obtained through trading activities instead of mining. This was later confirmed by the Company in its announcement dated 11 July 2016.

However, this latest discovery of physical Gold finally put the issue to rest. Borneo Oil's Gold is no more a figment of imagination. And it is only just the beginning. Borneo still have many promising sites which are pending exploration.

When I first started investing in Borneo Oil, I was a bit skeptical of its fundamentals. However, now I would say that I have more comfort with it. Hopefully they will announce further discoveries in the future.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

4 people like this. Showing 35 of 35 comments

icon, i think mango2 deserves an official apology from you... as he had mentioned many times in the past that most of the gold inventory was purchased for trading (which you insisted it was from mining activities)...

and it has prand it has proven what mango2 and I deduced is correct (that most of the gold inventory is purchased for trading)... you guys better watch out as gold trading is also a bit risky if gold price drops instead of go up... it is like betting to me...no one knows if gold will continue its uptrend move or the opposite direction...

2016-07-21 11:38

I don't need to apologise lah...when he raised the issue, I treated him with respect to the extent that I cut and paste his comments on my articles to alert my readers of the possibility that Mango could be correct. What more do you want me to do ? sigh

I will apologise to somebody if I was rude to him. But apologise to him because he got something right and I got it wrong ? It doesn't work that way, right ?

======

iloveshare128 icon, i think mango2 deserves an official apology from you... as he had mentioned many times in the past that most of the gold inventory was purchased for trading (which you insisted it was from mining activities)...

and it has prand it has proven what mango2 and I deduced is correct (that most of the gold inventory is purchased for trading)... you guys better watch out as gold trading is also a bit risky if gold price drops instead of go up... it is like betting to me...no one knows if gold will continue its uptrend move or the opposite direction...

21/07/2016 11:38

2016-07-21 11:43

forget it lah iloveshare, no apology will you have from low life character macam ni

2016-07-21 11:49

I am not always correct (nobody is perfect).

Sometime after I published an article, if I discovered some of my view is incorrect, I can't simply publish another article to make a U Turn. Many readers bought the stock after reading my articles. If I change my stance too drastically, there will be a lot of commotion, leading to losses by my readers. It is better to wait and see first and let market forces slowly play it out.

In Borneo Oil's case, I accepted Mango's view might be correct when he raised it few weeks ago. However, instead of drastically revamping my article, I feel that a better way is to cut and paste his comments on my articles for everybody to read.

In actual fact, the way I handle this case has proven to be correct. If I simply revamped my earlier article, many of my readers would have panic and sold at a lost. By allowing them to hold on their shares, they can now benefit from Borneo Oil's subsequent announcement of gold discoveries.

Investing is like that mah - you be a bit patient to ride out the rough patch. Don't simply panic and sell. As long as the company is ok (not in financial distress), no harm take a wait and see approach.

2016-07-21 12:01

I have no regret how I have been handling the case, and I don't see the need to apologise to anybody

2016-07-21 12:01

ok icon, you have your stance too, understandable... no worry.. just cheers and enjoy the investment... :)

2016-07-21 13:42

well said icon8888!!! U know, the biggest mistake I din do is to buy airasia when the time u mentioned "sailang"... N bcos of ur airasia article, I spend lot of time in i3 now ^^

Thumb up!!!

2016-07-21 13:48

Relax, relax. Everything on this forum are merely opinions. So are all of the analysts' reports.

Feel free to acknowledge or agree to disagree. No one pointed a gun to your head and forced you to buy.

2016-07-21 14:11

Thanks iloveshare128 for your support.

Anywhere I do not think an apology is necessary as at least Icon "... treated him with respect to the extent that I cut and paste his comments on my articles to alert my readers of the possibility that Mango could be correct." and thanks for that Icon.

What puzzled me is with Icon's sharp analysis skill as proven in the past, why he steadfastly held the view that the Bornoil gold inventory is gold mined, when circumstantial evidences clearly said otherwise. It make me wonder is Icon part of syndicate (no offence intended)?

Maybe Icon may have an answer to my puzzlement. Thanks in advance.

2016-07-21 17:31

tipu one lah i seen many companies like this before.....in the 80's remember KESANG strike gold. then a few years back RANHILL strike oil all tipu. after they dispose off their stocks they will say no gold.

2016-07-21 21:44

Still got plenty of gold? Thought brexit took most off the gold many many moons ago. If really still got plenty, others would have got hold of it first. Leave it there for bo to pick it up?

2016-07-21 21:45

In the future, if you disagree with my article, go and write another article to argue against it lah. That is easier than trying to convince me to change my article. I don't mind input from others, but I reserve the right to decide how I write them. Nobody can dictate to me what to write

2016-07-21 22:12

Thanks for your suggestion, Icon. I don't think I am up to the standard to write article yet. I think I just stay with commenting for the moment (minus convincing u to change your article)

2016-07-21 22:50

Icon really PPP who bring bad luck one. See! Proven again, more he wrote, the share price will goes down....damn bad luck magnet

2016-07-22 00:43

Haha.........why must I tell you my move?

You keep asking me sell, but share price up and up saja.

2016-07-22 00:54

Bornoil no matter business is gold mining or gold trading, they still in right track of business. The gold resources become limited in near future. Value of gold will be appreciate slowly. Long investment in gold is alternative investment by the rich investor now. With discovery of the new mining at Indonesia, I believe bornoil future is very bright.

2016-07-22 03:54

Mining of gold take longer time and process to show profit. If bornoil not trading gold, they may not able to provide us profit this quarter. Although small profit but show they are very eager to turn the company to black again.

2016-07-22 03:58

Icon888, do not simply pick a stock to write. Only good stock fit his criteria then only he write. For long term bornoil worth more than 0.40

2016-07-22 03:59

So far bornoil performance is still strong since support price 0.145 . U will see more uptrend in coming quarter. The stock inventory of gold mining is increase day by day by bornoil. The next quarter result will be exciting

2016-07-22 04:04

Do simple calculation before you write, not sure either ignorance or pure x@#x&*

2016-07-22 09:19

All bros, there is no absolute answer one. If you don't like gold investment or gold trading due to it is high risk, pls stay away from this counter. As the share price might be collapsed if gold price drop.

There is nothing wrong if someone foresees gold price will be up further in near future and top up more shares.

Anyhow, I have made my profit as I don't like gold investment. the revenue of latest quarter is already more than 5.5x of this newly discovered gold reserve.

Decision is yours. Huat ar!

2016-07-22 10:09

Due to the lack of clarification in the inventory report, many ppl have been caused to believe that gold in the inventory are gold mined, when they are not.

Now with this annoucement of gold reserve of 1,892 kg in its Bukit Ibam Mine in Pahang, but the actual cost of mining not ascertained/affirmed yet, many ppl may have been caused to believe that the reserve can bring good profit to the company, when at the end of the day it may not, due to the cost issue.

(Pls see soojinhou comment below, reproduced from Bornoil thread)

Will ppl belief about good profit from the reserve be crushed in due course, just like their belief about the gold inventory earlier? I do not know.

But so far Bornoil has set a not so illustrious precedent in its unclarified inventory report.

----------------------------------------------------------------------------------

soojinhou: Sumika, I agree with everything you said, but it all boils down to cost. How much does it cost to get the gold out from the ground. If it cost less than spot price, it is profitable, if it is more, then it is not. Now CNMC's ore grade is actually quite poor by global standards, and Bornoil is 4-5 times worse than CNMC's. Bornoil is also using a non-cyanide technique which I'm not familiar with. I'm not pouring cold water on you, I hope you make truckloads, but at this moment, it is too difficult to deduce the approximate cost. Mind you, the management guided that they produce gold at a cost of USD 500/oz. I don't know which mine they are talking about but it is almost certainly impossible to get such a low cost from such poor grade ore. Good luck. Just remember ya, to get 1 gram of gold from an ore grade of 0.3 g/t, you need to leach more than 3 tons of ore. That's a humongous load of dirt for a pitiful amount of gold. The management can choose to front load the higher grade ore first, those that are above 1 g/t, in which 874.2 kg can be extracted. But watch out if the company does that because when the higher quality ore are exhausted the cost increases dramatically.

19/07/2016 20:31

2016-07-22 14:13

simple conclusion right, why write so long. is not viable to mine. company wasting high cost to do exploration paying geologies, an all the experts.

2016-07-22 16:26

I kind of agree with what soojinhou wrote... please note that when Bornoil mines, they have to payout a certain % to the state government and the original grant owner... that is also a cost incurred.. if this mining business is so profitable, why would the 1st hand grant owner lease it out to Bornoil? ok, you can say that this "alibaba" is lazy, he wants to get easy money by not doing anything..(that could be part of the reasons)... but, if you know this is a hugely profitable project, will u lease it out to 3rd party for a small portion of %? I will not... and I also doubt if Bornoil is using the hundreds of millions (from right issues) in a legal way... i have seen many directors purposely place big purchase orders/procurement and pocket in some of $$$ (under table deal with the vendors)... that is why I have been cautious with this company)... frankly speaking, Transmile in the making is not impossible..

Bornoil's directors may think (i say "may", haha): I don't care if this mining business is profitable or not... I just know that buying a lot of machines with my "brother-brother" vendors is a profitable business to myself.. haha...

2016-07-25 11:34

This already explained earlier by the management that they secure this leasing agreement during the bearish gold environment, that why they can get it at very low n cheap price to make this mining activity profitable.

2016-07-25 23:32

Here's an estimate on how much is the Bukit Ibam Gold project worth. It is just a vague estimate with many unknown variables, so please don't screw me if my estimates are wrong.

Knowns:

Profitable ore grade, 28,107 oz @ 1g/t from 874,228 tons of ore. 0.3g/t grade is excluded from calculation because it is significantly below global average ore grade which is 1.01 g/t, taken from here: http://www.visualcapitalist.com/global-gold-mine-and-deposit-rankings-2013/

Initial capex = RM2.5m

Heap leach capacity = 7k tons per cycle.

Unknowns:

Cost per oz. So assumed USD 700/oz, a bit higher than CNMC's USD 500/ oz because Bornoil is using a method called "Earth Gold" which I am totally unfamiliar with, and presumably more expensive because it uses no sodium cyanide. Also CNMC's average ore grade is better at 1.4 g/t.

The amount of leach days per cycle. So I assumed 10 days per cycle, around the same as CNMC's, which I believe is around 2 weeks.

Average gold price. So I assumed USD 1,300/oz, the present spot price.

Processing capacity per annum = 7,000 tons per cycle * 365 days per year / 10 days per cycle = 255,500 tons of ore per annum

Amount of gold produced = 255,500 tons * 1 g/t ore grade = 255,500 grams per annum or 8,215 oz per annum

Annual profit = 8,215 oz per annum * (USD 1,300/oz spot price - USD 700/oz all-in-cost) = USD 4,929m per year = RM 19,716m per year

Assume no tax, and that Bornoil will be able to get tax concession for capex spent

EPS=RM 19,716m / 2,842,000,000 number of shares = 0.69 cents per share

Remember, cost is unknown, days per cycle is unknown also. Also, ore reserve is not set in stone, as exploration proceeds, ore reserve will expand. I don't know why is the company busy buying back shares. Maybe they hit a jackpot somewhere they didn't disclose. I dunno.

2016-07-28 18:30

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-23 14:30:00

EMA 5

5 Mins

SELL

2024-07-23 14:30:00

ADX

5 Mins

SELL

2024-07-23 14:30:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-23 14:30:00

EMA 5

30 Mins

SELL

2024-07-23 14:30:00

EMA 5

10 Mins

SELL

Apps

Top Articles

1

BFM Podcast

2

Koon Yew Yin's Blog

3

CGS-CIMB Research

Genting Plantations - Proposed Land Acquisition in Indonesia

5

save malaysia!

6

Koon Yew Yin's Blog

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

ImCK

yes net cash company + goldmine

2016-07-21 10:33