Icon8888 Gossips About Stocks

(Icon) CIMB (2) - CIMB Niaga Profit Up 74%. Buy Lah, Wait For What ?

1. Introduction

Yesterday, CIMB Niaga released its June 2016 quarterly report. There was marked improvement in results. Net profit increased by 74% Q-o-Q.

(Press release spinned it as 318% increase Y-o-Y. However, I think Q-o-Q is more reflective of its latest earning momentum)

2. Results Analysis

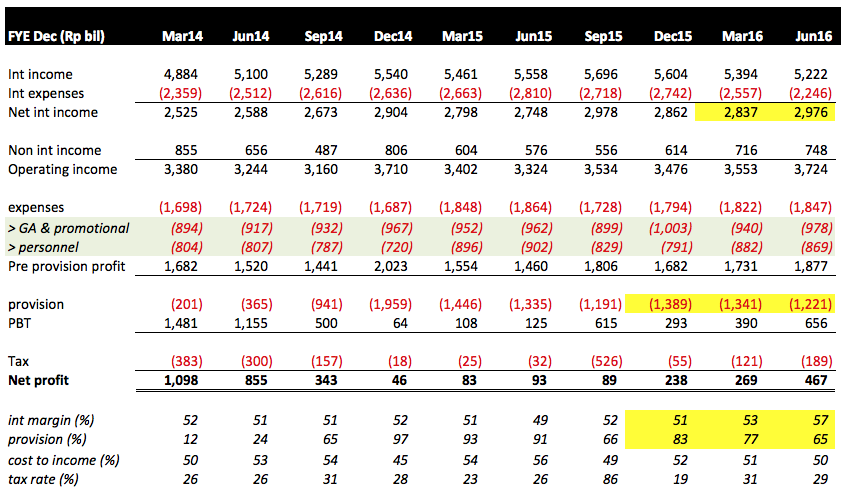

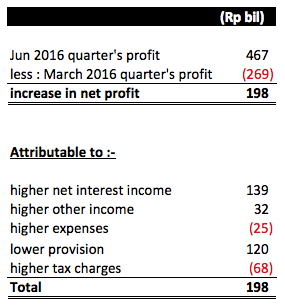

(a) Compared with previous quater, net profit increased by 74% to Rp467 bil.

(b) One of the major positive contributor is Net Interest Income, which increased by Rp139 bil compared to previous quarter. The increase is mostly due to decline in interest expenses from Rp2,552 bil in previous Q to Rp2,246 bil (decline of Rp306 bil), mostly due to increase in Current Account Deposit. Net interest margin improved from 53% to 57%. Well done !!!

(c) The other major contributor is lower impaired loans provision, which resulted in saving of Rp120 bil. This is the second consecutive month of decline, after peaking in December 2015 quarter.

Provision is expected to continue to decline in coming quarters as CIMB CEO hinted in a recent interview that he expects second half of 2016 to perform better. Please refer to my previous article for details.

(d) Operating expenses increased by Rp25 bil. This was a negative surprise. After the mid 2015 Mutual Seperation Scheme, I expect cost to come down, not go up. Anyway, it is not a big issue as the increase is not really that big.

3. Earning Forecast

In my previous article, I have guarded feelings for the CIMB Group. I sensed that they are turning around, but was not sure when the recovery will actually take place. However, with CIMB Niaga announcing a reasonably good set of results yesterday, I have turned much more positive towards the group.

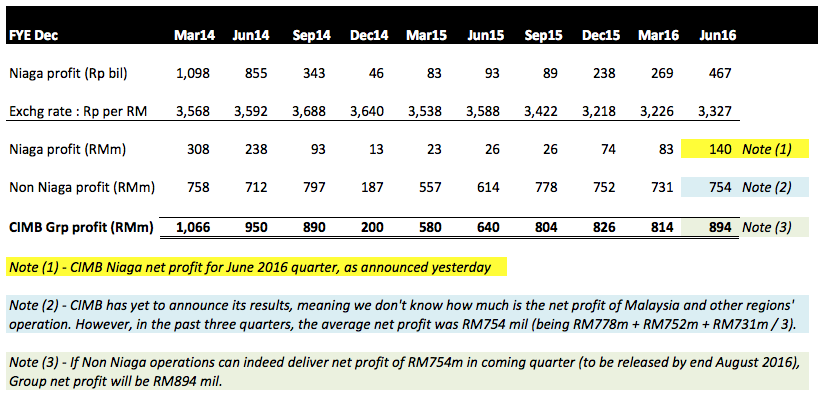

Armed with this new piece of information, I set up a financial model to try to feel the CIMB Group's coming quarter result.

Many people frown upon building financial model to predict future earning. Garbage in garbage out, if you get your assumptions wrong, your prediction will be way off.

However, in this particular case, there is sufficient ground for making such an attempt - the performance of CIMB's non Niaga operation has been fairly stable. In the past three quarters, it has generated net profit of RM778 mil, RM752 mil and RM732 mil respectively. I believe there is reasonable chance that the coming quarter will be more or less the same.

By putting together the above information, the model estimates that coming quarter net profit will be approximately RM894 mil.

But how should we interprete this figure ? What is the implication on valuation ? In other words, what should be the Target Price ?

4. Target Price

I previously set a Target Price of RM5.20 for the stock. That was plucked from the air based on my entry cost of RM4.29 and expected return of 20%.

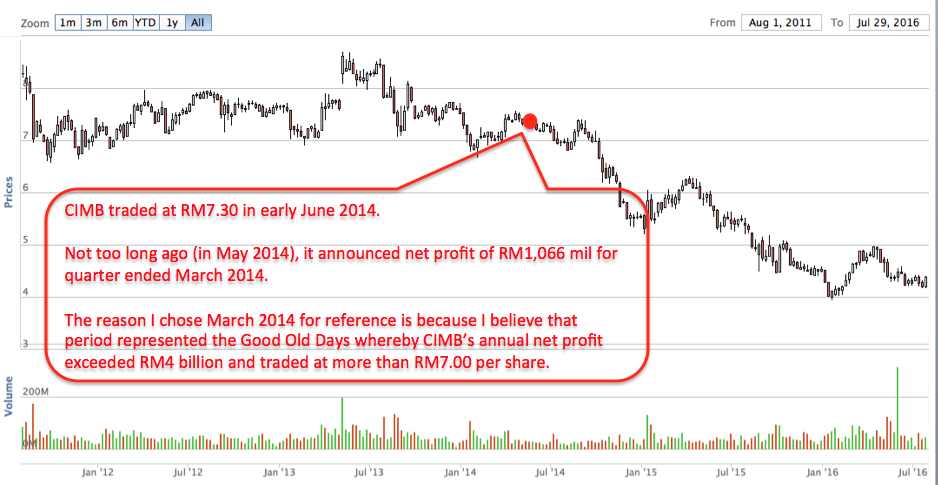

However, now that I have a better feel of the Group's positive momentum, I am happy to revise it upwards. For inspiration and guidance, I looked back to early 2014 when CIMB was still doing well.

As shown in the diagram above, CIMB traded at RM7.30 based on quarterly profit of RM1.066 bil in March 2014. The coming quarter of RM894 mil predicted net profit, if materialised, will be approxmimately 84% of its March 2014 quarter profit.

By applying 16% discount to RM7.30, I arrived at revised Target Price of RM6.13 for CIMB over the next 12 months.

This represents potential upside of 40% over latest closing price of RM4.39.

5. Concluding Remarks

(a) Among all the banking stocks, I believe CIMB has the best long term growth potential. This is because of the relatively high weightage of its Indonesian operations. Indonesia's GDP per capita is still low and its population is huge. The country will conitnue to grow at a brisk pace for many years to come, dragging CIMB along with it.

(b) The Group's past 12 months performance was disastrous. Its exposure to Indonesia became a big liability, dragging down its overall profitability as Indonesia floundered under the tremendous downward pressure caused by collapse of commodity prices.

(c) However, this weakness has now become its strength. From investing point of view, CIMB has bigger upside potential compared to other banking stocks such as AFG, Public Bank, Hong Leong Bank, BIMB, etc, which have done reasonably well operationally.

(d) With the Indonesian economy now gaining strength, I believe we have reached an inflexion point for CIMB. The risk and reward ratio going forward looked favorable. It is time to stop sitting on the fence.

Buy lah, wait for what ?

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

6 people like this. Showing 27 of 27 comments

If the concluding remarks are true, then we should all buy CIMB NIAGA. But now through CIMB, we can get some first.

2016-07-30 15:44

I like the difficult reforms Jokowi has pushed through, and it appears that Indon may outgrow Malaysia in the future. The tax amnesty it undertook will bring in a flood of money, and if Jokowi plays his cards right, all these money will go to fund infrastructures that Indonesia badly needs. Banking as a bellwether of the economy will likely benefit.

2016-07-30 18:33

hi,i m newbie...hope can learn some investment skills here.....CIMB will be my first stock....

2016-07-30 18:54

Am bank also almost better than cimb

Exclude the public bank , hong leong , MAYBANK

2016-07-31 09:52

Icon, oil prices are falling. Will there be more provisions? I bet so.

2016-07-31 13:13

But its a good price to enter if you can hold for 5 years, not 5 months. Just my 2 cents.

2016-07-31 13:15

Investment must now capitalize on those countries that have potential of high GDP such as Philipines and Indonesia and Vietnam etc..Public Bank, CIMB and Maybank are supposed to be considered as they have branches there.

2016-07-31 20:44

Thus there is no doubt Maybank and CIMB subsidiaries in Indonesia are doing very well from the recent announced quarter results for instance. The trend could be continue for many years to come.

2016-07-31 20:48

CIMB is definitely worthy to be take note. Personally, I am more bullish on its upcoming 2Q but less bullish on its target price. If you look in details, their non-interest income dip a lot (almost Rm200m) compared to previous quarters due to trading losses but still their profit is stable. If all else maintain, non-interest income back to normal plus Indon, I think Rm1 bil is reasonable. But I think its price should trade between RM4.85-RM5.40 for the next 6 months mainly bcos the ROE has came down a lot since their good days and sentiment on the banking industry is not great

2016-08-01 08:51

AmBank has a much better valuation than CIMB and also low exposure to Indonesia & Thailand. Poor yields in O&G, Plantation & Coal mines will continue to affect banks in general for next few qtrs...

2016-08-01 09:44

Thanks Icon for your sharing again...

But I see 2 potential risks which may be quite averse to CIMB:

1) Non-Niaga net profit has been deteriorating since the past 3 quarters, from 778million to 752millions and then to 731millions. 3 consecutive quarters of poorer results. So it may not be correct to use the average of previous 3 quarters to arrive at 754million net profit. You see each quarter the net profit reduced by 21-26milions. So I expect non-niaga profit for Q2 maybe 731-(21-26million) = 705-710million instead of 754millions.

2) Yes, Niaga net profit has improved over the past 3 quarters. But the weightage is around 83/731=11% for the whole CIMB group... even if Niaga profit increases by 50million, it can be easily wiped out by non-Niaga profit that is reducing.

Conclusion: recent cut of OPR will definitely reduce profitability for banks (including CIMB) so i expect poorer net profit in Malaysia... and since non-Niaga profit is still a doubt (and has a high chance of getting worse), i dun see how Niaga profit (with small weightage) will help improve the overall CIMB group's profit...

just my 2 cents and I could be wrong...

enjoy investing though, cheers...

2016-08-01 11:22

buy when morgan give up cimb, what make u think u can pro than morgan analysis the futures

2016-08-01 11:46

next quarter if result bad how? Higher provision etc.???? hehe. Sell again ah? at loss ah?

2016-08-01 13:24

Post a Comment

Featured Posts

Apps

Top Articles

1

AmInvest Research Reports

2

TA Sector Research

3

4

save malaysia!

5

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Icon8888

Thanks fortunebullz for your input

2016-07-30 14:51