Icon8888 Gossips About Stocks

(Icon) Air Asia (13) - Clean Bill of Health

Originally, I have set aside few hours this afternoon to write about Air Asia's latest quarter result. It turned out that all it took was 15 minutes of my time - the result is so normal, clean and straight forward that there isn't much to comment about.

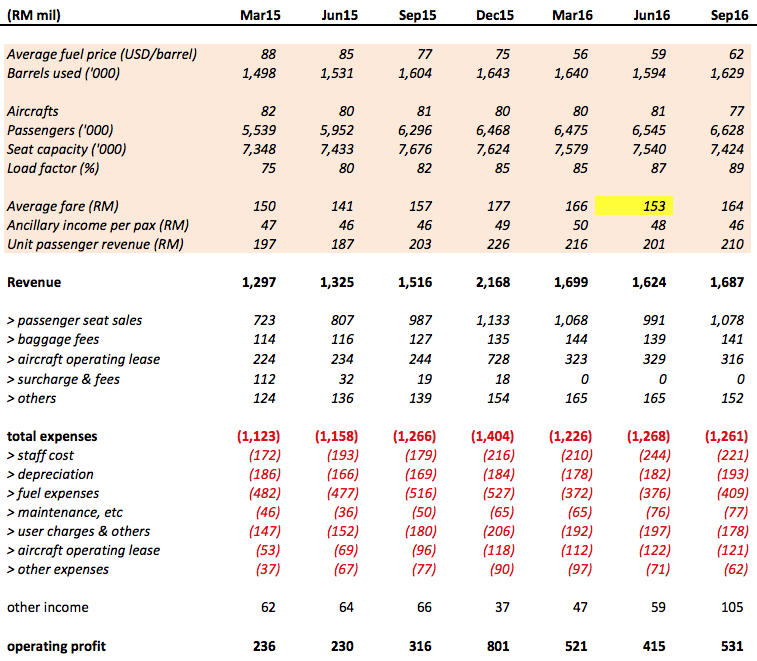

For me, one piece of information in the table that I paid most attention to is the average fare.

In the June 2016 quarter, average fare per passenger was only RM153, a big drop from RM166 and RM177 in previous two quarters. Coincidentally, my friends had also been telling me stories about how much freebies and discounts Malindo and MAS had been giving out recently to lure passengers. Putting all these information together, I was worried that a price war has developed and will drag everybody down.

Well, it turned out that my worry was unfounded. Yesterday's quarterly result showed that the June quarter's depressed average fare was due to low seasonal demand. The latest quarter's average fare per passenger has rebounced to RM164, an indication that the industry is still in good health.

I am pretty comfortable with next quarter's result. The final quarter is traditionally the strongest. There might be some margin pressure due to Ringgit depreciation, but I believe overall result should be not bad.

Tony Fernandes has also revealed that the offers for leasing unit Asia Aviation Capital is scheduled to come in in December (as many as 9 parties have shown interest). Positive new flows should provide support to share price in next one to two months.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

6 people like this. Showing 32 of 32 comments

Not clean at all

Depreciation

for last 4 quarters

184 + 178 + 182 + 193 = Rm737 million for Airplanes, property & equipment is just too little lah!

Now AirAsia has 170 A320 flying in the Sky. Total committed debt from Qr report is a Whopping Rm79 BILLION

So depreciation per year of Rm737 million over Rm79 BILLION = 0.009%?

AirCraft depreciation less than 1%?

Where got such accounting?

So AirAsia lease?

Under Aircraft operating lease

for last 4 quarters

118 + 112 + 122 + 121 =RM473 million

So add AirCraft (PPE) depreciation Rm737 Million + all leases Rm473 Million

= RM1.21 BILLION

Now divides by Rm79 BILLION (listed away from Main Balance sheet as Off Balance Sheet expenses)

= 1.5% Total depreciation plus operating lease cost?

Where in the whole world where car, plane, train or ship depreciates by only 1.5% per year?

This is hidden fraud accounting. Looks like the trick learnt from China listed companies?

25/11/2016 14:59

2016-11-25 15:00

We should poor our funds and sponsor calvin tan to some accounting lessons

2016-11-25 15:13

Aft Mr Calvin initiate sell call, AA direct drop?

Is Mr Calvin fund manager from Singapore?

2016-11-25 15:16

Problems created by i3-debts not always bad. See Puncak as example. Previously heavily indebted but profitable. Now cash rich but every qtr losing money.

2016-11-25 15:20

4th qtr have the strongest demand with higher load factor and average fare estimated will be achieved. Brighting things is Indonesia start to contribute profit. It remain Philippines, India. Indonesia success turnaround story soon will be realized on those losing money Associations. When the problems is less, it will be more focus attended with fast action will been addressed. Next qtr will be continue fly high. I am quite sure about this.

2016-11-25 15:20

well, ithk calvin just confuse the debt and Capital commitment outstanding. which mean the future order sign with airbus and GE.

2016-11-25 15:53

Why Calvin So free Geh ?

His Stock Picks are Bleeding Die.

I've made few ten K from HIBISCUS, in juz 1 hrs.

While, Calvin comments false infos in i3 .

http://klse.i3investor.com/servlets/forum/1100047695.jsp

2016-11-25 16:04

Calvin..just go buy a lot AA...wait the next agm n debate with management about ur depreciation theory...if the management not able to answer with reasonable answer...i pay u ten fold of ur AA share price..deal?

2016-11-25 17:23

Icon8888 sifu, thank you for the information, you are very experience in shares and provide accurate for the forum members, it is highly appreciated!

2016-11-25 19:51

This Calvin is the joker...he dont understand the debt and commitment...my maid also know but Calvin dunno...pity his wife and his children...I feel shame for his parent

2016-11-25 20:34

I can tell u Calvintan is the real person who told all the truth. Icon888 is paid to write the blog. I have readed all the blog of icon888, he told wat most people knew in the market and just window dressing it. But he didn't reveal the "secret" hiding behind the scene like wat calvintan. I salute to u Calvintan

2016-11-25 23:36

I can tell u airasia is at distributed stage. Don't waste ur money in this stock like wat have happened to puncak from 3.80++ (2.80++) felt until today 0.93.

2016-11-25 23:41

Airport tax will increase next year. Fuel price will hike soon. Accident. The risk is so high. Pay for 2.70++. Worth???

2016-11-25 23:44

calvin really don't know how to read financial statement.

Every stock is high risk, so better don't buy stock. You buy negative profit stock, possible go for more negative profit. Everything is high risk.

2016-11-25 23:52

Icon sifu, apparently the 9 bids for AAC comprised of 8 bids for a 100% stake and 1 bid for 80% stake; just to add to your comment of the 9 bids..

2016-11-26 01:31

One thing for sure, calvin is not a business minded person and he don't know business at all. Mike90 very kia shu~~ foreign fund selling but i tell u for sure they will come back very soon.

2016-11-26 09:31

Icon8888,based on Q3 results, AAC is carrying debt of ~RM2.1b. Once AAC is sold, this amount can be excluded from AA's current debt level of RM10.3b, am I correct?

2016-11-26 10:41

At least Calvin starts to use the word operating lease. We tried so hard to explain to this guy in his AAX airasia sitting on bomb thread. A

Unfortunately, he still doesn't understand capital commitment. I think he did not see the fine print that that is outstanding order in future.

I initially first time reply him and had respect to him as a person. Now, I just think he is so annoying and no more respect or whatsoever.

2016-11-26 10:44

Clean bill of health would not be clean bill of health if you believe Bloomberg reporter ....see my thread......that leasing income is not really leasing income but borrowings disguised as income.

2016-11-27 05:13

some of you just cannot see the forest for the trees. listen, there is no accounting gimmicks/shenanigans in aa's books.

2016-11-27 16:21

What CIMB Research say about "special dividend". Last time CIMB Research sent many to Holland by saying IFCA will reach Rm2.20. Today IFCA is only 29 cts.

So better learn to separate reality from fantasy!

I went in and took another look at AirAsia's balance sheet.

These two are RED FLAGS!!

1) Repayment of borrowings for Jan to June 2016 = Rm2.056 BILLION

Full year would be over Rm4 BILLION (So how could the total debt of AirAsia be around Rm10 BILLION?

AA is paying for Off Balance Sheet Debt of Rm79 BILLION!

Don't believe?

Well, look at year 2015 Jan to June figures

Rm2.199 BILLION (6 month). Annualized = Rm4.3 BILLION!!

2) CASH POSITION OF AIRASIA HAS DROPPED!!

(Refer to Balance Sheet again!)

Cash in the Beginning of Year = RM2.46 BILLION

Less Cash (RM929 MILLION)

Cash Position Now: RM1.533 BILLION

Cash Position has dropped by 39% to only Rm1.533 BILLION Only

SO CASH POSITION CANNOT COVER COMING BORROWING PAYMENT OF OVER RM2 BILLION For 2nd Half Year of 2016!!

This AAC can only cover Debt payment for 2nd half year of 2016

A little will be left for debt payment for Jan to June 2017 (Again Rm2 BILLION to be paid)

That's why Calvin Tan Research already stated clearly that

Airasia is sitting on a Time Debt Bomb!!

Forget about "special dividend" from AAC sale.

So don't be surprised that AirAsia will still need go a begging for more monies by selling other stuff or other tricks?

2016-11-27 16:26

My uncle koon never recommend airasia, so i will not touch this company, unless he ask me to buy

2016-11-27 21:45

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

All Official Update

3

My Trading Adventure 2025

4

Bursa Stock Talk

5

My Trading Adventure 2025

6

My Trading Adventure 2025

7

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

8

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

mike90

Foreign fund is selling !!!

2016-11-25 14:42