Investing theory 2 - IPO valuation

StoneCo's (NASDAQ:STNE) CEO Thiago Piau on Q4 2018 Results - Earnings Call Transcript

Philip ( buy what you understand)

Publish date: Tue, 19 Mar 2019, 09:08 PM

I am so impressed with the quality of transparency for NYSE and US based listed companies (I wished I had the same thing for my bursa companies, but I'm too lazy to transcript during AGM). They do everything they can to provide relevant information to future investors. Today is the announcement of the latest Q4 earnings conference call, which STNE has crushed (114% revenue growth YoY, and huge profits growth 660%). Yes, the premarket share price has gone up to USD43 per share. I see great things for this Berkshire Hathaway/Alibaba backed company, here is why:

StoneCo Ltd. (NASDAQ:STNE) Q4 2018 Earnings Conference Call March 18, 2019 5:00 PM ET

(https://investors.stone.co/static-files/734abc50-e5dc-468d-9968-2e4f7784848c) for supporting material

Company Participants

Rafael Martins – Investor Relations Executive Officer

Thiago Piau – Chief Executive Officer

Marcelo Baldin – Vice President-Finance

Lia Matos – Chief Strategy Officer

Conference Call Participants

Felipe Salomao – Citibank

Eduardo Rosman – BTG Pactual

Craig Maurer – Autonomous Research

Domingos Falavina – JPMorgan

Neha Agarwala – HSBC

Pierre Safa – Silver River Capital

Operator

Good afternoon, ladies and gentlemen. Thank you for standing by. Welcome to the StoneCo Fourth Quarter 2018 Earnings Conference Call. This conference is being recorded today Monday March 18, 2019. By now everyone should have accessed to our earnings release, the company also posted a presentation to go along with its call. All material can be found at www.stone.co on the Investor Relations section. To follow this conference call, the company will be presenting non-IFRS financial information including adjusted net income and adjusted free cash flow. These are important financial measures for the company, but not a financial measure as defined by IFRS. Reconciliations of the company’s non-IFRS financial information to the IFRS financial information appeared in today’s press release.

Finally before we begin our formal remarks, I would like to remind everyone that today’s discussion will include forward-looking statements. These forward-looking statements are not guarantees of future performance, and, therefore, you should not undue reliance on them. These statements are subject to numerous risk and uncertainties that could cause actual results to differ materially from what company’s expectations. Please refer to the forward-looking statements disclosure in the company’s earnings press release. In addition many of the risks regarding the business are disclosed on the company’s final prospectus for the initial public offering filed on Form 424B4 with the Securities and Exchange Commission which is available at www.sec.gov.

I would now like to turn the conference over to your host Rafael Martins, Investor Relations Executive Officer at Stone. Please proceed.

Rafael Martins

Good afternoon, everyone, and thank you for joining us today. Today, I have here with me Thiago Piau, our CEO; Marcelo Baldin, VP of Finance; and Lia Matos, Chief Strategy Officer. Before I comment on the fourth quarter and 2018 results, I would like to turn the call over to Thiago. Thiago?

Thiago Piau

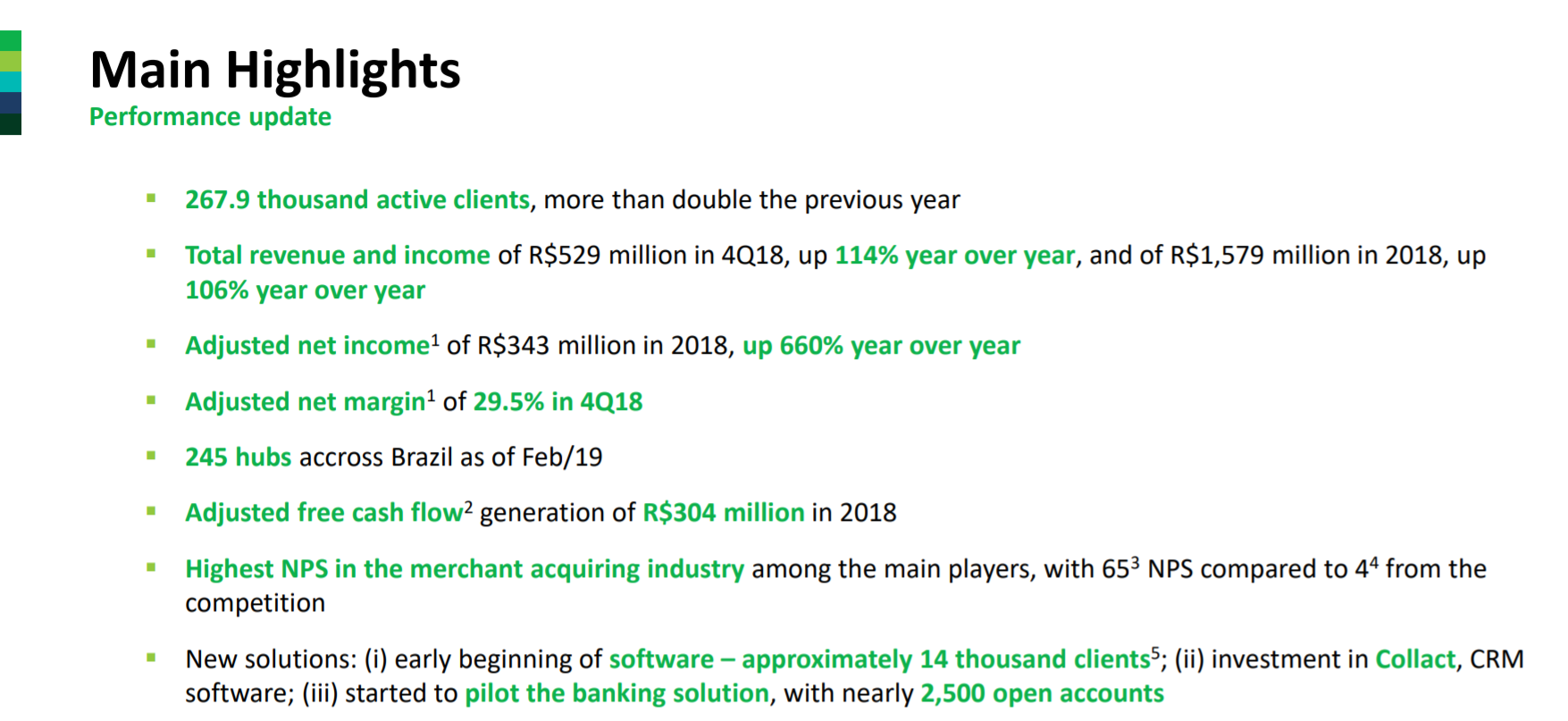

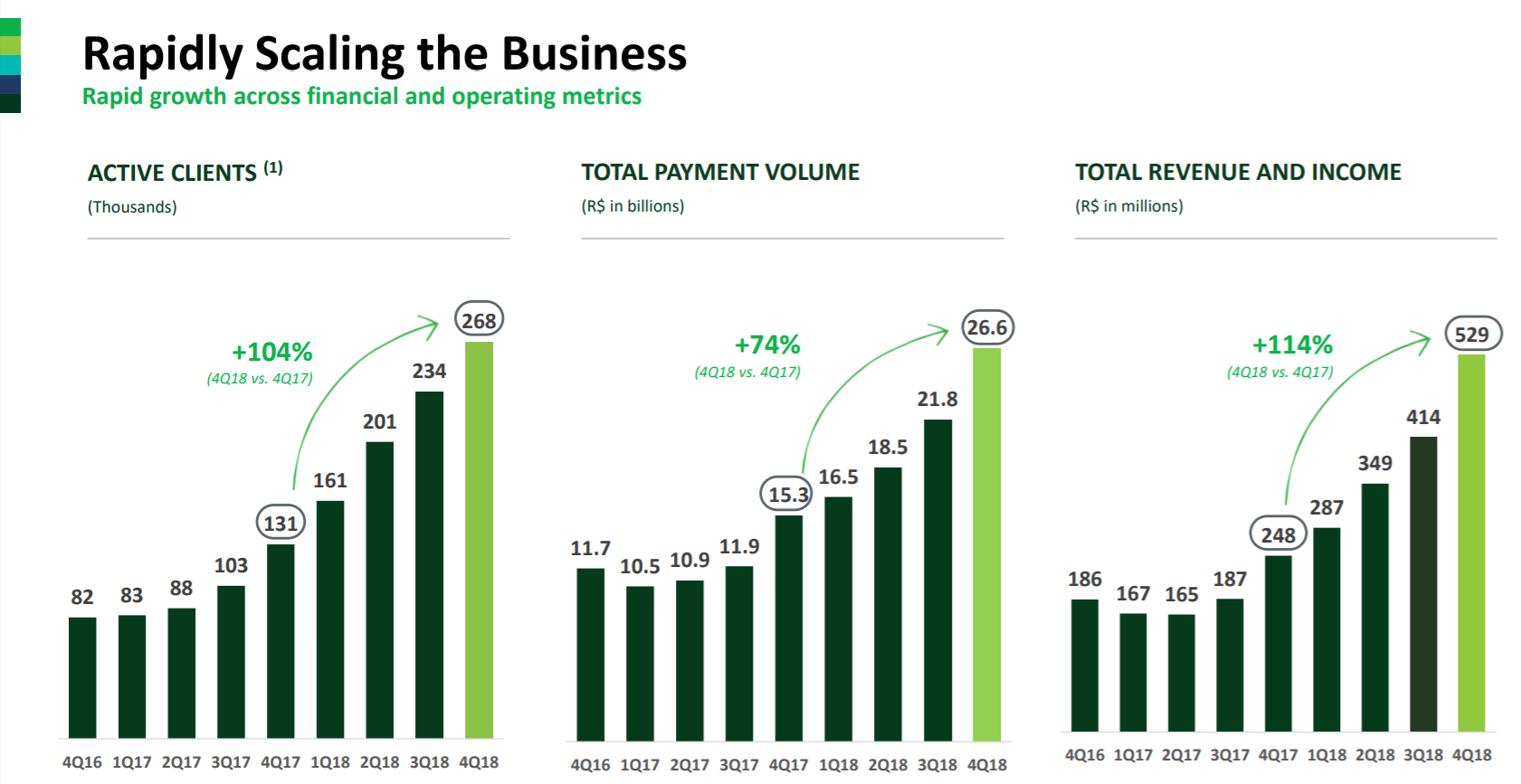

Thank you, Rafael. Good afternoon everyone and thanks for joining us for our fourth quarter and year-end 2018 earnings call. First, I would like to provide some highlights of our business performance. We believe that 2018 was a great year for us. We’re able to more than double our base of active clients, which increased by 104% to 268,000 by the end of 2018. We grew our revenue by over 100% both in the fourth quarter and in the year while at the same time significantly improving our margin with almost 30% adjusted net margin in the fourth quarter of 2018. We think this shows a combination of growth and profitability that is unique.

Continue with our strategy of hyper-local distribution, we currently have more than 245 active hubs across Brazil, covering around one third of Brazilian cities, which we think shows that there is still a fair amount of white space to reach. Despite our investments in the future of our business, we were able to generate more than R$300 million in adjusted free cash flow in the year. We remain focused on improving the client experience. Our NPS is 65; the best in the industry, compared to our competitors weighted average NPS of 4. Our results in 2018 highlight the success of our business model. However, we are still in the early stages of our mission, which is to serve merchants better, helping them sell more and become more productive.

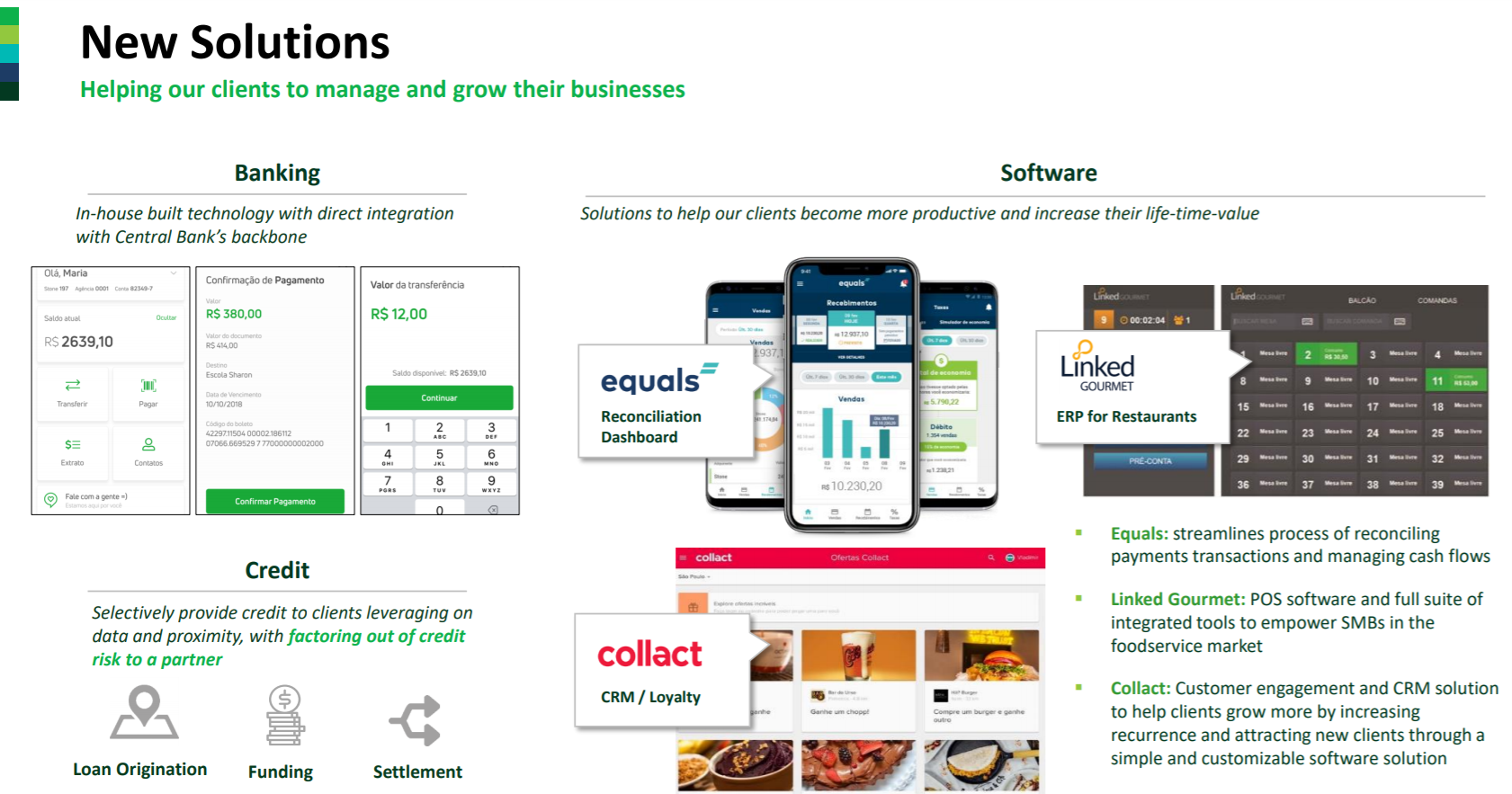

The overall company performance has improved throughout 2018. We saw our churn levels decreased in the second half of the year with churn rates in the fourth quarter decreasing by around 10% compared to the third quarter. This reflects a superior value proposition perceived by our clients, the best NPS in the industry, our client driven culture as well as proprietary technology that leverage on client data to prevent churn. Over the past few years, we've been consistently adding software capabilities to our platform to help our clients to manage their business better and sell more. This includes Equals our reconciliation software, Linked Gourmet, our ERP and POS solution focused on the foodservice vertical as well as online and offline gateways. More recently, this February, we also made a strategic investment in a company called Collact focused on CRM and loyalty, which enables merchants to increase their sales by improving recurrence while also leveraging on data.

The offering of software increased the lifetime value of the client, improving stickiness and giving us data to enhance our financial products. Nearly 14,000 clients already use at least one software offered by us and we have an objective to increase this number of clients in the future. A much larger number of clients use the client portal, dashboard and mobile app.

We expect to invest inorganically in additional software verticals over time. The main criteria for us to make new investments are: we have to find a passionate entrepreneur, who deeply understand the pain points of the clients, combined with our cloud-based technologies and an API-driven mindset of the technology team. We consider this set of characteristics essential to providing a complete and integrated client experience to our merchants.

Our strategy is to create a complete ecosystem combining payment software, which enables the company to access more data from clients and offer better financial projects with a fair price like banking services and credit. Regarding our banking solution, the pilot is performing in line with our expectations. There's a huge addressable market in that front and is very similar to the acquiring market when we began, variable services and high rates. We want to offer more friendly and convenient services at a fair price.

We now have nearly 2.5 thousand accounts in our pilots. We are still not making specific commitments with the timing of the full rollout of our banking products because we want to make all the necessary adjustments before that. In the medium and long-term, we really believe that these solutions will be very important for the company.

We started 2019 in line with our expectations and our business continued to improve. We remain committed to the execution of our growth strategies, which are based on high-quality products, the best client service in Brazil, a proprietary distribution channel and building of entrepreneurial and decentralized business culture with leaders that really think about the long-term.

We are also encouraged by the recent regulation in our industry and what that means for us and our clients. We look to grow in this market by executing our core strategy, opening more hubs, further penetrating our existing hubs, strengthening our digital strategy, increasing share of wallets and connecting to new integrated partners. We also look to continue to implement our disruptive model by upselling new products and solutions to merchants, multiplying our total addressable market.

As outlined in Slide 5 of our presentation, we still have a huge headwind to grow in the merchant-acquiring space in Brazil. We have only 6% market share in a market that has less than 30% card penetration. Besides, our future is certainly not only in merchant-acquiring. As Slide 6 shows, we estimate that the combined total addressable market of new solutions which are mainly banking, credit and software, is much larger than the merchant-acquiring addressable market.

Before I turn the call back over to Rafael, I wanted to say a big thank you to our team members at Stone. You're a huge part of what makes our company so special. With that said, I will turn the call back to Rafael.

Rafael Martins

Thank you, Thiago. As Thiago mentioned, we were able to more than double the number of active clients which grew 104% in December 2018, compared to December 2017 reaching 268,000 clients. This number does not include clients of Stone Mais, our solutions for micro-merchants. We haven't included this because in the fourth quarter, we were still in the test phase of the product. Beginning in the first quarter of 2019, we will include those clients in our reported number of active clients.

As we have mentioned in the past, this is not a strategic focus for our company but rather a complement to our current offerings. Total revenue and income increased by 114% to BRL 529 million in the fourth quarter of 2018, compared to BRL 248 million in the fourth quarter of 2017. This was mainly driven by a year-over-year increase of 109% in net revenue from transaction activities and other services, a 138% increase in net revenue from subscription services and equipment rental, and a 98% increase year-over-year in financial income.

Cost of services was BRL 101 million for the fourth quarter of 2018, an increase of 38% compared to the fourth quarter of 2017. Cost of services as a percentage of total revenue and income was 19.1% in the fourth quarter of 2018 and efficiency gain of more than 10 percentage points from 29.7% in the fourth quarter of 2017. This efficiency gain was seen in most lines especially transaction costs, deployment costs and personnel as the company dilutes the costs related to its proprietary platform and gains operating leverage in customer service and technology.

Administrative expenses in the fourth quarter of 2018, increased by 17% year-over-year to BRL 73 million. The increase in administrative expenses is primarily attributed to growth in personnel expenses and depreciation and amortization. Administrative expenses, as a percentage of total revenue and income was 13.9% in the fourth quarter of 2018 compared to 25.3% in the fourth quarter of 2017, an efficiency gain of 11.4 percentage points in the period.

Selling Expenses grew by 74% reaching R$59 million in the fourth quarter of 2018. This was primarily due to an increase of R$21 million from additional head counts in our sales team, in line with our strategy to grow in the hubs. Financial Expenses were R$75 million, 22% higher than the fourth quarter of 2017. This increase was primarily driven by an increasing funding of R$12.5 million due to higher prepayment volumes.

Financial Expenses as a percentage of financial income reduced from 47.6% in the fourth quarter of 2017 to 29.3% in the fourth quarter of 2018. This reduction is explained by a higher financial income and especially by lower cost of funds due to lower base rate, cheaper funding lines contracted by the Company and use of a higher amount of own cash to fund prepayment operations.

As a result, our adjusted net income was R$156 million in the fourth quarter of 2018 with a margin of 29.5% compared to R$20.9 million in 2017 and a margin of 8.4%. The main factors that contributed to the growth in adjusting net income were increased in total revenue and income, primarily due to higher TPV and focus on growing the Company’s base of SMB merchants; operating leverage in most lines, specially Cost of Services and Administrative Expenses; and reduced cost of funds, as the Company switches to cheaper funding and increases the use of own cash to fund the prepayment operation.

Overall, we have seen strong operating leverage. Our costs and expenses have decreased from 68.5% of total revenue in the fourth quarter of 2017 to 44% in the fourth quarter of 2018. Important to highlight that our P&L carries investments in selling expenses related to hubs that have not yet fully contributed with their revenue potential.

On Slide 10, we show how the operational leverage plays out when we look on a same hub analysis. Those charts show the evolution of revenue and salespeople for a fixed number of hubs, namely all of those that were active at the beginning of the fourth quarter of 2017. We believe that this is helpful to illustrate the healthy growth of older hubs as well as the operating leverage on a same hub perspective. Also in our hubs, we have seen continued ramp up in the number of clients as our hubs get more mature.

As you’ll see in our presentation in Slide 11, our hubs that have been open for nine quarters have more than seven times the number of clients, then the hubs that have been open for one quarter. And finally, the company generated R$304.2 million of adjusted free cash flow in 2018, compared to negative R$29.6 million in 2017. The main reason for that increase was an improvement in our adjusted net income from R$45 million in 2017 to R$343 million in 2018, despite the increase in non-cash depreciation and amortization expenses from R$57 million to R$92 military in 2018.

With that said, operator, we’ll open the call up to questions.

Question-and-Answer Session

Operator

Okay. At this time, we are going to open it up for question-and-answers. [Operator Instructions] The first question comes from Felipe Salomao with Citibank. You may proceed.

Felipe Salomao

Hi, Thiago, Rafael, and everyone else. Thanks for the opportunity of asking questions. I have just one question. And again, sorry to insist on this topic, but I guess this is the number one debate on the industry to-date. It’s about competition. So we recently met one of the large merchant acquirers in Brazil in terms of market share, and they mentioned that data from February and March in terms of net client adds is already showing somehow improvements.

So that said, I would kindly ask you guys to, if possible, to share an update on how the first Q2019 quarter looks like so far, in terms of, I mean churn net adds, TPV growth. I mean everything possible, of course, and then please don’t say anything you can’t. And that’s my question and by the way congratulations for very strong results, congratulations.

Thiago Piau

Hi Felipe, thank you very much for your question. It’s a great question. So regarding competition, we have not a new. I think that the dynamics is the same. The competitors are trying to push price, but we keep talking about value proposition with our clients. So let me talk to you about net new adds, take rates and churns. So first, I’m going to talk about net new adds in the fourth quarter of 2018. So in the fourth quarter, there was less working days, because of holidays and the fact that we gave collective vacation to the sales team in the last week of December and the first week of January. Also we were focused to higher quality clients as you can see by the average TPV per client. So we have added 4.8 billion in TPV in the fourth quarter 2018 versus 3.2 billion in the fourth quarter 2017. And with this we managed to keep net new ads at the same level of the third quarter 2018 with much more volume, which represents an increase in productivity of around 10% in the fourth quarter 2018 with better quality.

Regarding take rates, as we have discussed it previously, our price strategies defined by value proposition and not by competition. So in fourth quarter 2018, our take rates remain roughly stable. But talking about the short and medium strategy, we can reinvest take rates to increase lifetime value and create a better environment for our multi-product strategy. However, in the long run, we still expect overall take rates to increase given our strategy to offer new products and improve yields. Just talking about churn, we have seen a reduction in churn of around 10% in the fourth quarter 2018. So we are very confident that we are in the right track regarding the value proposition and the business model of the company.

Rafael Martins

Felipe, if I may add to what Thiago just said regarding the 2019 results. So what we see so far in the year is that we are performing according to our plans. So this is very important message. The company continue to improve in all areas and we are very happy to see that our results in the beginning of 2019, they will be reflected in our margins because the operating leverage still continues to be very strong, right. And regarding competition, we don't have nothing. We have nothing new to say. I mean, as Thiago mentioned, nothing that calls our attention that it's very different from one we expected.

So this is the basic message of 2019, we are not making specific comments about specific metrics in this quarter. We'll probably discuss them in the next earnings call. But I'd like to give that message in a simple way for you to see and have a view on how we started this year.

Felipe Salomao

Perfect. Rafael and Thiago. Thank you very much for the very clear answers and congratulations again in a very strong results.

Thiago Piau

Thank you very much.

Operator

Our next question comes from Eduardo Rosman, BTG Pactual. You may proceed.

Eduardo Rosman

Hi, guys. So congrats on the numbers. Two questions from my side. First on, how the business is structured in Brazil. Do fear anyhow, let's say, if your competitor start paying clients in D plus 2, do you think that this is a threat and this could change the industry. So it would be interesting to know your thoughts if you think that this is a possibility. And what this could mean for the acquiring industry in Brazil. And my second question is on let's say, how big you think you can be in Brazil on the acquiring market? And when do think you're going to feel comfortable in expanding to outside Brazil, what you've been learning the country. Thank you very much.

Rafael Martins

Hi, Rafael here. Thanks very much for your question Rosman. Regarding your first question, I think that D plus 2 discussion we have tapped this. And if you consider that the competitor may offer it for free. This is basically a discussion of price, right? Because both ourselves and our competitors, we already offer D plus 2 to many, many clients. And, regarding the pricing strategy of the competitors, we prefer not to comment on that. As Thiago mentioned, our pricing strategy is driven by value proposition, is not by the competitor. So I don't think that D plus 2 discussion, it's very relevant right now and I wouldn't comment on their strategy right.

Thiago Piau

Just to compliment Rafael, Rosman, it's Thiago here. I believe that the discussion regarding D plus 2 in terms of regulation, we have already moved this discussion as this is not good for society. So for us makes no sense to change a working capital structure based on an asset-backed security with the receivable in which the merchants use that to have a better rates in terms of working capital and put it within the price. We think that makes no sense to change it for in a structure in which the bank space up front and charge very high rates from the consumer.

And we have discussed about this with the regulator in a very technical way. So I think that in terms of regulation, there's some players, one player trying to be vocal about this, but that's not good for society. And I do not see at this time competitors paying D plus 2 without charging, we don't see rationale behind it. So I'm just going to pass back to Rafael to talk about market share and addressable market.

Rafael Martins

So to your second question of how big we can become. I think we see two things, right. So the first, the payments market, we still have only 6% market share to date. We see a huge headroom to grow in that market specifically a lot. When you look at the growth volumes in the whole industry, what we see is that we are taking about 20% to 30% of the incremental volumes and so – and as well as in the regions where we have present, we see also very strong market share.

So given that, we believe that, as we have previously mentioned, we can reach 25% to 30% market share. I mean, we believe that’s a very feasible objective, right? This is regarding the payments. And regarding the new solutions that we are just starting right now, we see that the total addressable market is really huge as we have shown in our presentation and that basically, when you see the addressable market of payments is less than 20% of the – all the markets that we are entering, so we see two headrooms to grow. First is payments and the second one is the additional solutions.

Thiago Piau

So just to complement on that, so to summarize, we have approximate 6% of the payment market and that represent less than 20% of the total addressable market that we are targeting. We are seeing a total addressable market of BRL 20 billion in acquiring, BRL 75 billion in credit, BRL 10 billion in banking and BRL 9 billion in software. So we really believe that in five years from now, our company will be completely different and this separation between payments, software and technology will be overcome and we will become the partner of choice of SMBs in all of their needs. So it’s still a lot of room to grow, both in payments and the other products.

Eduardo Rosman

Perfect, guys. Thanks a lot for all the details.

Operator

Our next question comes from Craig Maurer with Autonomous Research. Please you may proceed.

Craig Maurer

Yes, hi. Thanks for taking my questions. First, I hate to ask you to do this, but would you repeat your commentary regarding how you started first quarter 2019? But beyond that, I wanted to ask you a little more qualitatively about the competitors, about the incumbents. Obviously, they were quite loud in their intentions to cut price, take back market share late in the year, but from your estimation, what’s gone wrong? I mean, I understand your discussion of leading with value, but at some point price does matter. And so I think the stock is reacting the way it is because people are genuinely surprised that the incumbents have failed so badly to this point to slow your growth. Thanks.

Thiago Piau

Hi, Craig. Thank you very much for your question. So first, regarding the first quarter highlights, what we have to say that we started 2019 according to our plans and the company continued to improve in all areas. So we are very happy to see results in first quarter. We are very happy to see that the operational leverage is increasing and that should be reflected in the margins of the quarter.

Regarding competition, as we said, it’s only based on price. We decided not to engage in price war. I cannot comment what is happening on the competitors. We don’t want to talk about the competitors. They have to talk about it, but what we can see is no change in terms of business model. So we are used to competition since day one. Since the early beginnings, our broad client base were taken from the incumbents. So we learned how to deal with that. We decided to bake our company based on customer advocacy and value proposition. So we will not engage in any type of price war mainly because we do not need to do this. We believe that there is a very huge opportunity to put much more products for the same clients and create value over time.

So with that said, I just would like to pass the word to Lia just to say a little – a few words about strategy and new products. Lia, please.

Lia Matos

Hi, Craig. Thanks, Thiago. Just to mention and emphasize what Thiago just said before regarding our strategy, we believe that we really developed a strong set of proprietary assets, which is our own distribution, our technology platform and our service model, that puts us in a unique position to really become the partner of choice to provide multiple solutions to SMBs. And we think that with this we can capture many future growth opportunities. We develop these proprietary assets by first offering payments and we’re now focusing on complementing the software with software banking and credits.

And we are now really increasing the speed of rollout of our software solutions, because we think that this can really increase lifetime value, provide more stickiness and also to us, provide more data to be able to be more assertive in offering our financial products and we are continuously exploring new investment opportunities and software. In parallel to software within financial products, we’ve seen very encouraging early results in banking and we think that banking and credit will really be the next frontier growth and improve yields for us.

Like we said before, we’re still in pilot mode in banking with two and a half thousand clients, but we are really encouraged by the early results. We don’t want to rush to roll out until we really assure that we have the perfect offering and we’re also very happy with our very early understanding of the opportunities in credit.

Thiago Piau

So, in summary, Craig, I think that we respect competition a lot. We are very humble to learn continuously about how the market evolves and the strategies of the competitors, but we decided to keep our mind – our mind and our heart in our clients to really understand their needs and evolve our solution over time to continue to delight customers. So that’s our strategy.

Craig Maurer

Thanks. That’s all. Very helpful. Just one addition to that, if you could elaborate on the decision to pursue the micro-merchant market, that would be helpful.

Thiago Piau

Great. Regarding the micro-merchant, we saw that the lifetime value to cost of acquisition ratio is much different than our business model, which is mainly focused on SMBs. So, we decided to be a specialist and the main partner for SMBs with different products. So, we feel how the lifetime value to cap ratio of around stem and we are investing our capital in channel – in distribution channels.

We see that in the SMBs, the gain is all about growing the lifetime value. While in the micro-merchant space, the game is all about driving down the cost of acquisition. So, it’s a different kind of needs, different kind of aberration. So, we decided not to invest heavily on that. We have the product as an obligation on ourselves, because we have to protect our brand in some hubs. But we decided not to target this market and we will try to keep focused on SMBs, because she will have a lot of things with the focus that we have.

Craig Maurer

Okay. So, the products available, but you’re not actively pushing it very aggressively?

Thiago Piau

Yes. Okay. Thank you very much. Thank you, Craig.

Operator

Next question comes from Domingos Falavina, JPMorgan.

Domingos Falavina

Hi, thank you guys also for taking the question. Apologize if I haven’t said on the cell phone. I’m visiting resident clients and I would like to also chime in the same question as before, but I don’t know, like I’m a little lost, because I’m getting also discrepant inflammation between what I’ve been hearing here from locals and the message. So, if you could even qualitatively mention specifically churn. So, you gave very good quality date on the 4Q, churn has decreased and it stood around 10%, Q1 to 4Q.

First Q1 – first month and second month, January and February, what are you seeing net addition decelerate within SMBs or how is churn behaving versus the 4Q? Because at least like most of the locals have been visiting a year, they’ve been – the local news here is that the churn would have increased within your clients and the incumbents would have been able to capture some of those clients. So, if you could elaborate even qualitatively, January and February, exits off clients, vis-à-vis what you saw in the 4Q?

Rafael Martins

Hi, Domingos, Rafael here. Thank you very much for the question. So, regarding the first quarter, just to be clear, we aren’t seeing our growth plans, and I mean, be hindered by competition. We are not making specific comments on any metric of the first quarter. But what I can tell is that the first quarter started strong with our growth plans on track with our operational metrics on track and that’s why we don’t see any relevant news, anything on that – on that regard. So, I’m just going to have to be disciplined here not to comment any specific metric, but that’s our comment. That’s all we have.

Thiago Piau

Just to compliment that Domingos. So, as we said, a churns in the fourth quarter compared to third quarter decreased 10%. in first quarter, we are very happy to see the operational metrics that we have. And the most important thing is that – the way that we measure our productivity, it’s basically number of active clients added by sales personnel per working day. So keep in mind that in the fourth quarter, you have holidays with Christmas and New Year’s Eve and we did collective vocation to our sales force in the last week of December and first week of January mainly, because that’s the least productivity time of the year. So, when we adjust the net new wedge per work today. We see that our productivity went up by almost 10% in the fourth quarter of 2018. and we keep within our plans regarding growth for first quarter. So, we are very confident with the results of first quarter.

Domingos Falavina

Okay. So good to hear. And just on the revenue opportunity on the bank side, I mean, we do see some risk in current account fees and it seems the strategy of most player like in their bank and some others has been offering free accounts, which – when you compare an addressable market, it looks seek on the bank side in terms of randomly generated. But once you try to convert them to you, you wouldn’t imply in offering some level of discounts and plus banks do have a substantial number of individual clients. So, my question is like what kind of package are you planning on offering your clients? Is it going to be a free current account or you’re planning on charging for that as well? Just so that we start having an assessment of – if you have 300,000, 400,000 clients, what kind of revenues we could see with banking related products?

Thiago Piau

Great, Domingos. great question. So, in terms of banking, our strategy just keep your mind is targeting only solutions for merchants. And on that, we are targeting transactional activities such as wide transfer, bullet reissuance, bill payments, tax payments, payroll solution that really helped merchants to manage their operation better. So, we see that when you take into account the incumbent banks. there’s a huge prop regarding the transactional activity and that’s what we are targeting.

So, the plan here is basically not charging for the accounts. We’re charging for the transaction of the creditors. So, we see a huge opportunity to be the only one provider for merchants with software banking and payments. So, we are targeted the transactional activities that if you break now the P&L of the big banks, then you take the transactional activities for merchant, you’ll see this addressable market, offer around R$10 billion that we are showing here in our presentation.

Marcelo Baldin

Domingos, even if you’ll see the P&L of the bank, so you’ll see over R$30 million in revenue. But this is not all of those is the focus of our company. So that’s why we only sold R$10 billion here.

Domingos Falavina

Now, so good to hear. Congrats on the quarter and thank you.

Thiago Piau

Pretty much, Domingos

Marcelo Baldin

Thank you.

Operator

Next question comes from Felipe Salomão, Citibank.

Felipe Salomão

Hi guys. Thank you again for the opportunity to ask another question. I would like to ask if you could share an update on the debate regarding the new banking lock rule. the Central Bank postponed and the implementation of the new rule by roughly 100 days and according to local press, there has been a lot of debates – of debates, if there’ll be just one, let’s say infrastructure behind the banking locks, which will both be FGC or why are other players prefer to have more than one infrastructure behind the way, the new banking lock agreement would work. So, there’s a lot of moving parts is even difficult to summarize. But if you could, if possible, give us an update on how the debates have evolved about how the new banking lock system will work, and the opportunities that this new model could bring to you that, that will be great. Thank you.

Thiago Piau

Great Felipe, great question. Thank you for the opportunity to talk about this new regulation regarding what we are calling the new SCG, right. So we believe that it will be net positive for us. As competitors, we're always able to access our client base with bundle offer of credit plus payment, but we couldn’t offer payments to their clients with credit, mainly because if we did it, the banks immediately require their clients to pay down those loans creating big hassle for them.

So for that reason, we lost several growth opportunities in the past, but now it will be easier for Stone’s onboard clients with big loans, even that the banks cannot have great relationship on a discretionary manner. We will be able to prepay all merchant receivables, even those with credit as they can – and they can use those funds to pay back their loans and further fund their operation with prepayments.

So there would be a big competition between prepayments and credit that could not happen before. As you can see by market data, prepayment fees are significantly lower than credit fees and therefore we believe prepayments will actually gain share over credit in the market. So as a result, we believe that this will be net positive for our company.

Felipe Salomão

Okay. Thank you. Thank you for the explanation.

A – Rafael Martins

Thank you Felipe.

Operator

Next question from Neha Agarwala, HSBC.

Neha Agarwala

Hi. Thank you for taking my question. Congratulations on the strong results. I wanted to follow up on Domingo's question regarding the credit business. Is it fair to say that in the initial months or probably years of operation, you would look more transactional towards more transactional activities and the actual revenue generation from opening new accounts and on boarding more clients would be limited, so the contribution to the earnings will be limited from the credit pay-out that is my first question?

My second question is more operational related. Could you give us an idea of what is the total number of employees that you presently have? I understand that you have about 245 hubs currently what is the plan for the coming year and in the coming three years how many hubs would you like to have? Thank you so much.

A – Rafael Martins

Hi Neha, Rafael here. Thank you very much for the question. So regarding your question in banking, our idea is to generate revenue in that market mainly regarding transaction activities and not monthly fees for their accounts. The client should not pay a fee for having the account open. So as Thiago mentioned, payroll wire transfers, valid reasons and so on, we should drop charge on a transaction basis. So that's why that addressable market that we put here, we include only those check-in accounts transactions, we don't include other services and fees that banks usually charge at merchants. So that’s to your first question.

To your second question, we are currently around 4,000 people. We will have probably the exact number soon in our 20-F, so that's the ballpark number of current employees. Regarding the hubs, we still see a lot of room to grow in the hubs. So we feel – you'll see today our hubs cover around one-third of Brazilian cities still. So we see a lot of headroom there. We don't provide specific guidance regarding the number of hubs, but what we see is that there's still a lot of white space in the country for us to took over, right, a lot of potential.

Neha Agarwala

And one more question among your competitors, which one would you – if you can point out if there's anyone specifically that you see as more aggressive or who mostly do you consider as your competition?

Rafael Martins

I think we would prefer not to comment on any specific player Neha, we see the market dynamics over time over the past years that sometimes there's a specific competitor does more aggressive sometimes the other one. So this may change over time. We wouldn't comment on a specific competitor that is being more aggressive because this may change over time. So it’s very seasonal.

Neha Agarwala

Thank you so much.

Operator

[Operator Instructions] Our next question comes from Pierre Safa, Silver River Capital. You may proceed.

Pierre Safa

Yes, hi. Thank you very much for taking my question and congratulations on the fantastic results. So just going back to a statement you make on the prepayment fees or the prepayment costs being significantly lower than credit. How sustainable do you view that to be because effectively the financial institution providing credit to the customer is taking all of the risk and you're not? So how do you foresee effectively this evolving and the sustainability of a model where you're providing capital, but see effectively limited or no risk, right? So I understand the value you're playing here, but I'd like to hear a little bit of your views here. Thank you very much.

Rafael Martins

Hi, thank you very much for your question, Rafael here. I think when we look at the prepayment rates, we have seen in the – that the prepayment rates they have already undergone some pricing pressure in the past with an entrance of new players. Debt repayment rate is still a much lower than credit opportunities that the merchants have. Usually, the way you have to look as sort of the – the opportunity costs of the merchants, right, and today we see that with the new regulation and everything that we see on the field is that probably prepayment would grow its share of funding in the society overall, especially for those SMBs. So it's very difficult for us to comment on the very long-term future and how things we play out, but that's what we have seen so far, right. So we don't see a reason for merchants to not use prepayments to try to compete with more expensive credit that they have to fund working capital for example.

Thiago Piau

And just – Pierre, it’s Thiago here, just an additional comment. We are in the very early beginnings of this credit strategy, so we are studying a lot about how the market works. We believe that this will be a new frontier of competition and the level of assets that we have with the distribution, the technology and the service, what is in the best position possible to compete against incumbents, but it's too very soon to say about credits over time on a quarter-by-quarter basis. We will give you more update and color about how we are going to evolve on that front.

Operator

[Operator Instructions] There are no questions at this time. This concludes the question-and-answer session. I will now turn over to Mr. Rafael Martins for final considerations.

Rafael Martins

Thank you. First, I would like to thank everyone for participating on our call. We are very happy with our results. Very enthusiastic about the future opportunities that we have in front of us. Thank you very much for your time and see you next quarter.

Operator

This concludes The Stone’s today presentation. You may disconnect your lines now. Thank you.

>>>>>

Full disclosure: I am an investor in STNE since January 2019, and bought 200,000 shares@USD19

More articles on Investing theory 2 - IPO valuation

HOW TO BUY BREAD - AND LESSONS TO LEARN FROM CATHIE WOODS

Created by Philip ( buy what you understand) | Jan 12, 2023

My open letter to Lim brothers - my thoughts on Senheng IPO

Created by Philip ( buy what you understand) | Jan 30, 2022

Why I invested in Serba Dinamik, Kpowers and SCIB

Created by Philip ( buy what you understand) | Sep 02, 2020

THE PERFECT PHONE FOR OLD MEN LIKE HARRISON FORD.

Created by Philip ( buy what you understand) | Feb 25, 2019

Discussions

1 person likes this. Showing 17 of 17 comments

Once again, i am deeply and humbly impressed by Philip sharing this counter in Jan.

2019-03-19 21:49

Imagine if you were an opensys or alipay or GHL which is a simple payment or services faciliator. If one day Bank Negara decided to give you a banking license, how would you go about it?

Would you do it the traditional way with long queues, a branch where people take numbers and wait their turn and a hassle-full filling of duplicates, hard copies, information and slow approvals from KL, and old legacy systems which fills up rooms upon rooms of files.

Or would you think deep on how to upend the existing encumbants like HL, Public Bank, Maybank with a system that is catered to the online connected future today, where you no longer need physical locations and everything can be done and verified online automatically with a automated process. And you freed all the legacy backend staff with a mobile team of connected sales staff all with cloud connections, and all doing outbound work directly at your customers office, instead of sitting in a desk in an bank branch somewhere.

As a client, who would you rather talk to? the bank guy drinking coffee with you in your own office, cafe or business? or that grumpy old lady in the bank teller telling you to fill in physical forms?

>>>>>>

Our strategy is to create a complete ecosystem combining payment software, which enables the company to access more data from clients and offer better financial projects with a fair price like banking services and credit. Regarding our banking solution, the pilot is performing in line with our expectations. There's a huge addressable market in that front and is very similar to the acquiring market when we began, variable services and high rates. We want to offer more friendly and convenient services at a fair price.

We now have nearly 2.5 thousand accounts in our pilots. We are still not making specific commitments with the timing of the full rollout of our banking products because we want to make all the necessary adjustments before that. In the medium and long-term, we really believe that these solutions will be very important for the company.

2019-03-19 22:28

I find that in the future, majority of bank interactions can be done online. And those that are more tricky and problematic, I want them right here right now in my office telling me how to solve it.

When credit ratings, customer database is fully online, do you really need to visit your bank anymore?

2019-03-19 22:33

For some light reading of my previous analysis of this company.

https://klse.i3investor.com/blogs/philip2/191042.jsp

2019-03-19 22:56

Philip....Pchem when will jump like that?

very impressive performance - congrats!

2019-03-19 23:27

CORRECTLOH JUST LOOK AT GENERAL RAIDER CALL ON SAPNRG VERY TRUE MAH...!!

U NEED TO BE SMART AND HAVE SPECIAL HARDWORKING TRAINING IN ORDER TO BE SUCCESSFUL LOH....!!

Lessons from – “The Five Rules for Successful Stock Investing” by Pat Dorsey. Pat Dorsey is the Director of Stock Analysis at Morningstar.

· Picking individual stocks requires hard work,discipline and an investment of time (and money). SAPNRG IS NOT CHINCHAI MAH..IT IS MONTHS AND MONTHS OF INTENSIVE RESEARCH DONE VERY CAREFULLY TO GUARANTEE GREAT SUCCESSFUL BUY LOH...!!

· You need patience, an understanding of accounting and competitive strategy and a healthy dose of skepticism . THIS TRUE LOH...RAIDER CAN ASK U TO BUY RM O.30 AND THEN ASK YOU TO SELL RM 0.365 WITHIN 1 MTH AND MAKE 20%, BUT RAIDER DON DO THAT BCOS RAIDER KNOW SUCCESSFUL MAJOR KILLING IN STOCK MARKET, NEED TIME TO DEVELOP, THATS WHY RAIDER ASK U TO KEEP LONG TERM AT LEAST 3 YRS AND 3 MTHS.

· Buying stock means part ownership in a business .YES SAPNRG U ARE OWNING AN OIL N GAS BUSINESS, ALOT OF PRODUCTS NEED THIS RAW MATERIAL INPUT LOH....THUS DEMAND IS CONFIRMED LOH...!!

· Courage of conviction. U JUST LOOK AT RAIDER BOLD CONVICTION AND SAILANG CONVICTION WITH TP POTENTIAL 3.00, AND HOLD LONGTERM WITHOUT WAVERING EVEN MKT SELLDOWN...U WILL UNDERSTAND WHAT IS COURAGE & CONVICTION ABOUT LOH.

· Companies with most conflict of opinion are often best investments ( think contrarian). CORFRECTLOH ALOT OF PEOPLE ARGUE AND BELITTLE RAIDER SAPNRG PICK, BUT RAIDER JUST STANDBY WITH THE GREAT CONVICTION OF SAPNRG SUREWIN, WITHOUT ANY FEAR....BCOS RAIDER KNOW....THIS IS THE BEST PICK U CAN EVER FIND MAH..!!

EXACTLY SIMILIAR TO RAIDER MARGIN OF SAFETY APPROACH

Core principles of investing

o Doing your homework

o Finding companies with strong competitive advantages

o Having a margin of safety

o Holding for the long term

o Knowing when to sell

2019-03-19 23:46

if want to spam thread at least don't capslock la. So low class hardsell, I dont need to follow you to hardsell every thread convincing ikan bilis to buy. I just use long term profits and share price increase to show you how investing really works long term.

>>>>

PUTTING CONVICTION INTO ANALYSIS WITH BIG SUMS OF MONEY OVER LONG TERM HOLDING. FYI STNE ALREADY TURN INTO A 44 BILLION RINGGIT COMPANY LO. NO NEED WAIT 3 YEARS 3 MONTHS. USD19 INTO USD43, ANY QUESTIONS? 114% revenue growth YoY, 660% earnings growth YoY.

stockraider For So long Mr Long trying to equate stoneco to QL....i thought it is same type of business...but now it is found out totally irrelevant loh...!!

One QL with pe 50x is old type of commodities business another is payment system platform settlement PE 24x Stoneco loh...!!

I m wondering What QL got to do with stoneco, other than Mr long bought n own both of it loh...???

>>>>>>

YOU READ. BUT YOU DONT UNDERSTAND. OFFICE BOY MENTALITY. ALWAYS THINK THEY ARE THE SMARTEST IN THE WORLD.

stockraider What so special of buying into stoneco leh ??

U mean Warren Buffet give a call to Mr long & says koh kohchai i m buy into stoneco ah....!!

I read Warren Buffet buying into Petrolchina long time ago, what happen to petrolchina now leh ??

>>>>>>>

YES DO TELL ME ABOUT PE AGAIN, IF YOU LOOK TO THE PAST, YOU WILL NEVER REALISE A 660% INCREASE IN EARNINGS YEAR OVER YEAR.

stockraider Yes loh....this is precisely how greater fool theory works loh...!!

If u follow margin of safety principle disciplinary u will never buy gdex at PE 100x mah....!!

2019-03-19 23:52

Prmomotion of msia great oil company SAPE...mah...!!

Buy local company campaign mah....!!

Posted by (70B-SAPNRG-3Yrs) Philip > Mar 19, 2019 11:52 PM | Report Abuse

if want to spam thread at least don't capslock la. So low class hardsell, I dont need to follow you to hardsell every thread convincing ikan bilis to buy. I just use long term profits and share price increase to show you how investing really works long term.

>>>>

PUTTING CONVICTION INTO ANALYSIS WITH BIG SUMS OF MONEY OVER LONG TERM HOLDING. FYI STNE ALREADY TURN INTO A 44 BILLION RINGGIT COMPANY LO. NO NEED WAIT 3 YEARS 3 MONTHS. USD19 INTO USD43, ANY QUESTIONS? 114% revenue growth YoY, 660% earnings growth YoY.

stockraider For So long Mr Long trying to equate stoneco to QL....i thought it is same type of business...but now it is found out totally irrelevant loh...!!

One QL with pe 50x is old type of commodities business another is payment system platform settlement PE 24x Stoneco loh...!!

I m wondering What QL got to do with stoneco, other than Mr long bought n own both of it loh...???

>>>>>>

YOU READ. BUT YOU DONT UNDERSTAND. OFFICE BOY MENTALITY. ALWAYS THINK THEY ARE THE SMARTEST IN THE WORLD.

stockraider What so special of buying into stoneco leh ??

U mean Warren Buffet give a call to Mr long & says koh kohchai i m buy into stoneco ah....!!

I read Warren Buffet buying into Petrolchina long time ago, what happen to petrolchina now leh ??

>>>>>>>

YES DO TELL ME ABOUT PE AGAIN, IF YOU LOOK TO THE PAST, YOU WILL NEVER REALISE A 660% INCREASE IN EARNINGS YEAR OVER YEAR.

stockraider Yes loh....this is precisely how greater fool theory works loh...!!

If u follow margin of safety principle disciplinary u will never buy gdex at PE 100x mah....!!

2019-03-20 00:00

There are many great co in msia loh....like for example SAPE 1000% gain in 3 yrs 3 mths loh....!!

Do not listen to naysayer Philip loh....!!

What he says is not true loh...he just bad mouth msia co loh....!!

SAPE will perform very well...why waste time in STONE CO in brazil, when u don understand their system...u get conned u also don know mah..!!

Stick to msia..!!

Stick to SAPE loh..!!..

2019-03-20 00:05

Thanks for the update. I won't pay PE 40 for Stoneco, but I've already found a proxy to them at EV/EBIT 2.9. A lot more palatable than Stoneco. Thanks for sharing.

2019-03-20 08:09

Ok sape is the best company of 2021, rm3 incoming. You sailang all your money inside, wonderful.

Can stop spamming now? Stick to the topic I put, which is discussing and learning more about STNE earnings call.

IF YOU WANT TO SPAM AND PROMOTE ON YOUR SAPE, PLEASE START YOUR OWN THREAD. THIS IS THREAD IS NOT FOR THAT PURPOSE.

2019-03-20 08:38

One thing I've realized about market disruptors and tech companies in NASDAQ, it is really hard to use simple metrics like PE to evaluate them ( especially if a company can grow 114% it's revenues and 660% is earnings in a year). A of companies have begin to use more specific metrics to value their company growth ( churn rate, total number of users, expected revenues per user etc), and looking at STNE results, frankly I do agree to a certain extent.

For me I'm also Looking at multiple metrics to evaluate companies. Especially for STNE I find that total payment volume tpv as a measure

The size of microtransactions they earn, and the number of SMB as a measure of their Target market (6% currently of a 8.8 million small medium business customer base)

>>>>>>

Thanks for the update. I won't pay PE 40 for Stoneco, but I've already found a proxy to them at EV/EBIT 2.9. A lot more palatable than Stoneco. Thanks for sharing.

2019-03-20 13:24

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

save malaysia!

2

MQ Market Updates

3

BFM Podcast

4

BFM Podcast

5

M+ Online Research Articles

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

(70B-SAPNRG-3Yrs) Philip

I think that the dynamics is the same. The competitors are trying to push price, but we keep talking about value proposition with our clients.

This is how you build market share. This is a once in a lifetime kind of company.

2019-03-19 21:28