The dude series

Dude, what is up with Padini?

Padini is a both a brand and a counter that needs little introduction. The overall thesis of this article is that Padini has in the last 2-3 years suffered both in share price and profitability due to aggressive opening of new stores and offloading old stock at deep discounts due to the imminent GST, but starting from Q1 2016 (Sept), Padini has reached a turning point and the Group’s strategy is starting to bear fruit. This is why the share price is rallying in the past 2 months, and this article argues that if the turning point is legitimate, Padini will continue to rise to RM3.00.

As a caveat, I must first confess that I am but a desktop armchair amateur analyst guy. I do not have any professional qualifications in regards to investing (no CFA… for now?). I do have a CPA though (please don’t start stoning me saying that Accountants make bad investors), but am not a practicing accountant. I only hope to share and learn from everyone else.

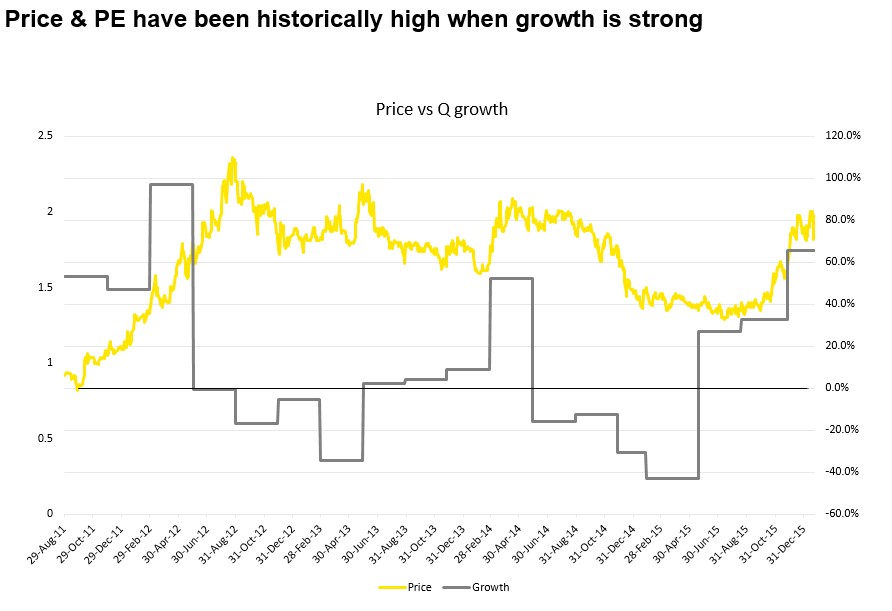

The above chart shows Padini’s 5 year share movement (dividend unadjusted). From 2011 – 2012, price rallied from roughly RM1 to RM2 in approximately 1 year. Subsequently, after a series of disappointing quarters, it was not able to surpass the RM2.40 level.

Padini holds a variety of reputable brands under their belt. Most of them are quite well known besides the fairly new Tizio brand. Padini segments their operations into five separate Sdn Bhd(s) as follows.

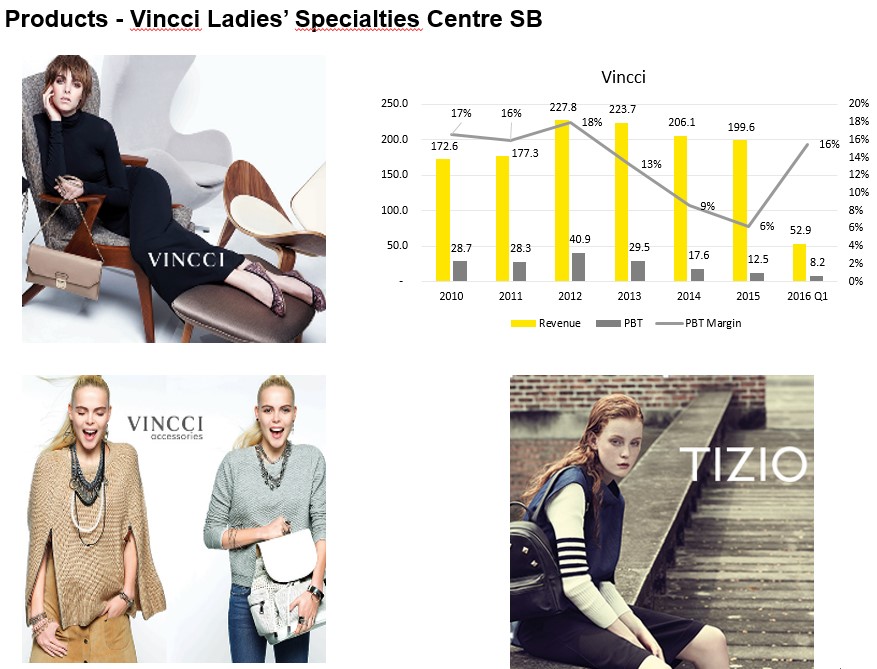

Vincci specializes in shoes and accessories and contributes 20% of total revenue and 12% of PBT to the Group. As at 30th June ’15, Vincci also has 64 foreign franchises. Total foreign franchise contribute approximately 5-6% of total Group revenue. No other brands have foreign exposure.

As you can see in the graph above, from 2010 – 2015, Vincci’s revenue has been flattish and PBT & PBT margin declining. However, looking at Q1 2016 (Sept Q), profit margins have rebounded strongly.

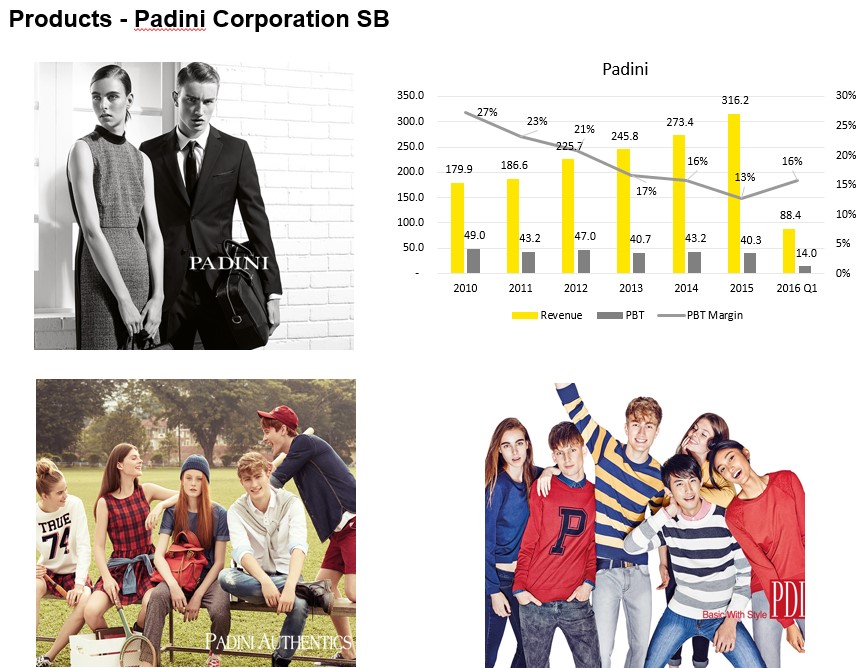

Padini Corp S/B holds the office, summer and casual wear. It contributes 32% of revenue and 39% of PBT for the Group.

However, unlike Vincci, revenue has been growing YOY. PBT however has been flattish with PBT margins declining. Similar to Vincci, PBT margins have reversed in Q1 of 2016.

Yee Fong Hung S/B (“YFH”) holds P&CO and the very popular Brands Outlet store. Unlike the other S/B in the group, YFH has shown tremendous revenue and PBT growth. PBT margin have also been at a steady mid to high teens. Revenue and profit contributions to the Group have grown from 11% and 7% in 2010 respectively to 32% and 43% in 2015.

Brands Outlet appeals to the mass market, delivering marginally less quality and design with significant discounts. This strategy has worked very well for them.

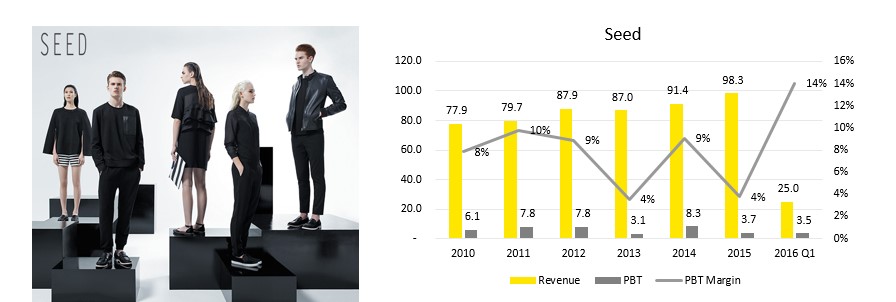

Seed contributes 10% revenue and 4% of PBT to the Group respectively. Margins have been at sub 10%, however in Q1 2016, this trend has reversed significantly.

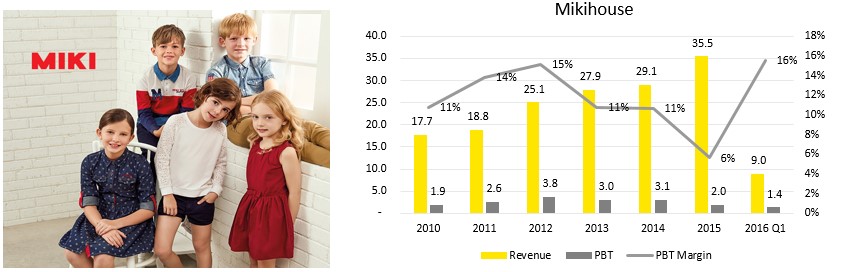

Miki Kids contributes 4% of revenue and 2% of PBT to the group. Revenue has been growing steadily, with PBT being stagnant. PBT margins have been decreasing, and similar to other S/B, PBT margins have been reversing in Q1 2016.

As you can quite easily see, across the board for all S/B, the downward PBT trend have been reversing. Let’s find out why.

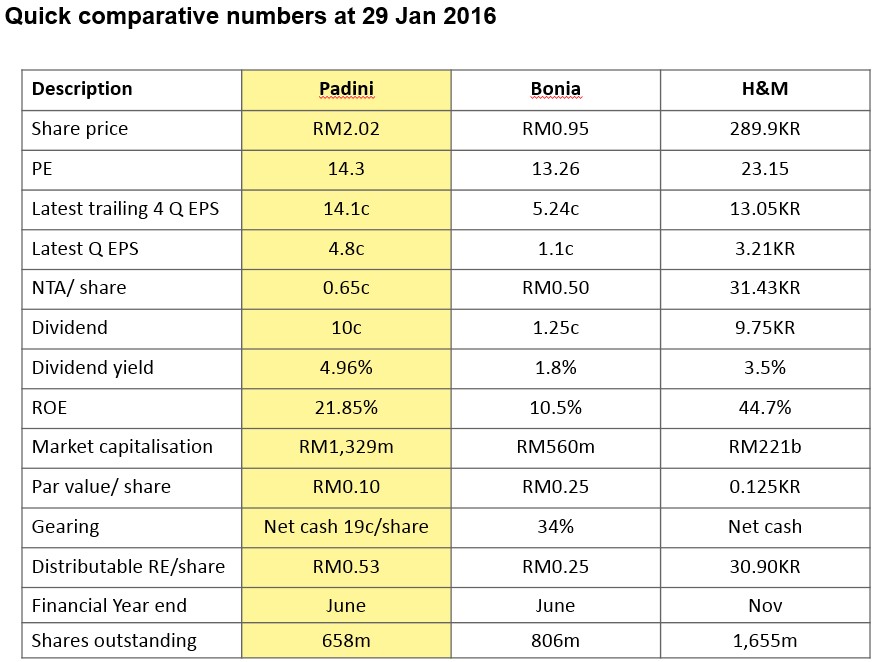

The above table compares Padini with Bonia and H&M. Most of the ratios should be quite familiar. At today’s price of RM2.02, the share is trading at a PE of 14.3 based on the rolling 4Q. Remember, this only accounts for one Q of Padini’s strong profits. Padini historically trades between 7 and 17 (refer to appendix), therefore a PE of 14 is not the highest Padini has seen.

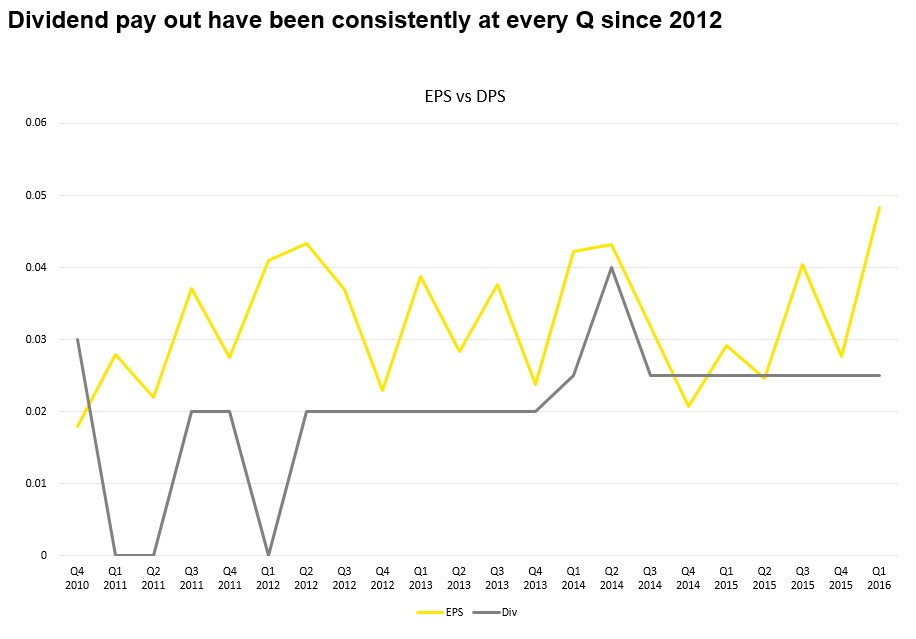

Dividend is at a decent 4.96%. Historically, dividend has ranged from as low as 2.5% to as high as 8.3% (ref to appendix). Usually, dividend is highest when the stock is being battered. Dividend has been consistently paid for the last 2 years (refer to appendix)

ROE is decent at 21.85%. However this figures is misguided as Padini has RM98mil of unit trust and RM174mil of cash. Stripping both and adding total debt, return on working capital yields a whopping 47%!!

(Note: BO: Brands outlet; PCS: Padini Concept Store)

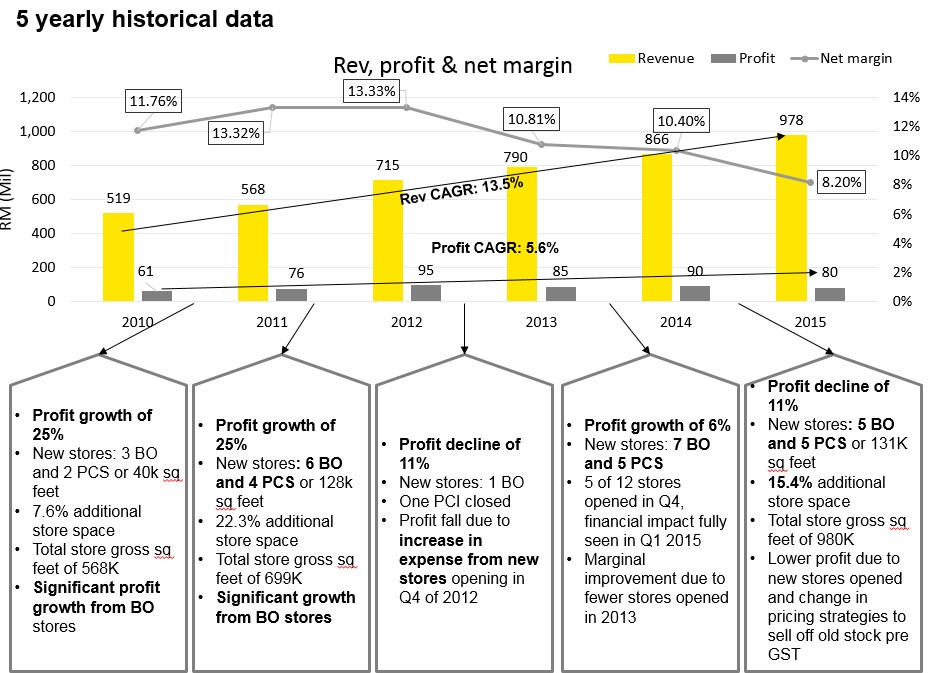

Revenue CAGR has been at a respectable 13.5% over the last 5 years. However, profit CAGR has not fared as well, at only 5.6%.

Profit decline in recent years were caused by declining profit from the opening of new stores. You must understand that every time Padini opens a new store, there will be two forms of cash outflow (thank you, CPA!). The money used to buy furniture and renovation are capitalized as assets. However there are pre-opening expenses such as cleaning, staff hired before the store is open, legal contracts, marketing expense (big), etc which are expensed immediately in the Q which the store opens. Therefore, whenever Padini opens new stores, especially in late 2011 and 2014, a PBT will suffer significantly in the first few Q after opening. Subsequently, the revenues will flow to cover the normal operating expense and profitability and margins will rise.

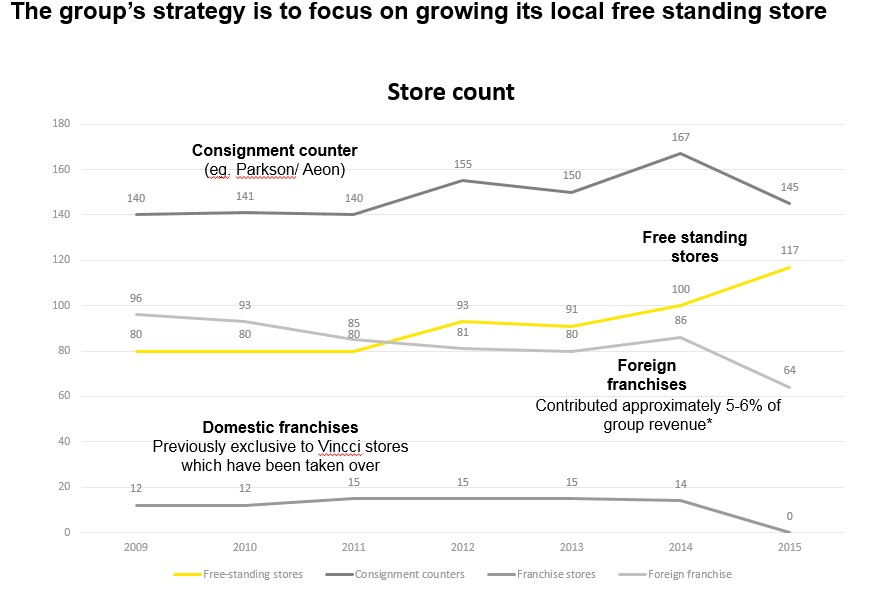

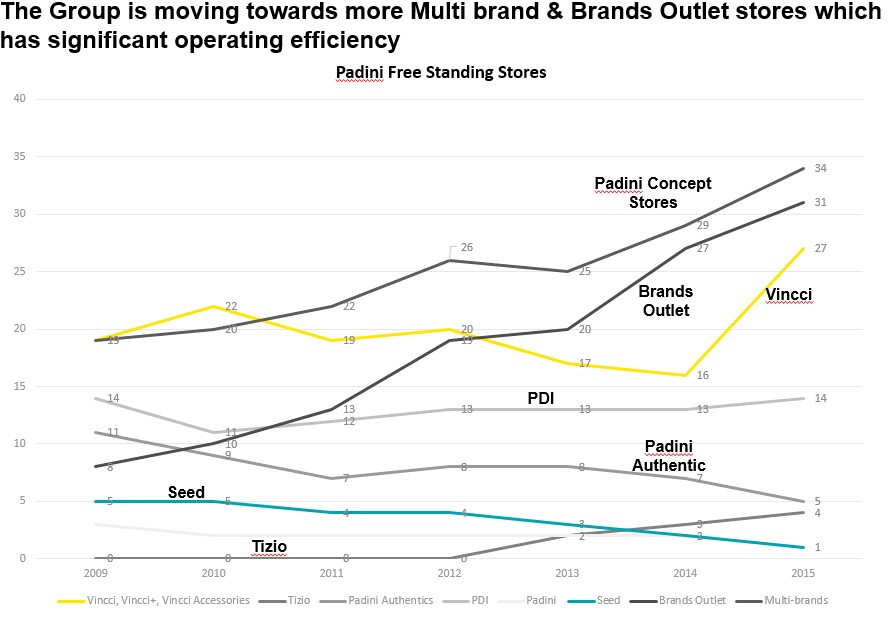

I must pause here for a little to highlight the group’s strategy of moving towards Padini Concept Store (“PCS”) and Brands Outlet (“BO”). PCS is a brilliant concept introduced at about 2003. While it may seem like a long time ago, Padini has actually existed since the 1970s. PCS combines all of Padini’s product offering under one roof. This is an excellent strategy as it gives Padini economies of scale leading to savings. Think lower rental PSF, contractor fees, shared support back end staff, etc. Also, it allows cross selling. Imagine, customers are looking to buy a pair of Vincci shoes and then “ooohh look at that cute top/ accessory/ sweater” (no, this isn’t me).

The group’s venture into BO is also a brilliant one which begun as recent as 2007 when it had its first BO store during the global financial crisis. As the middle class Malaysian gets squeezed from a weaker RM, higher cost of living and stagnant wages, being normal humans who still need to be clothed, BO provides the avenue for Malaysians to buy decent clothes (better than Aeon/ pasar malam [no offense]) at affordable prices. Therefore, the more you hear “weak consumer sentiment” or “weaker ringgit”, please think Brands Outlet.

The other reason margins and profit has been decreasing is due to the Group’s strategy to sell old inventory at deep discounts prior to the implementation of GST. This allows them to “throw” it away at low prices before 1 Apr 2015. The group’s strategy has been to remain affordable despite the GST. Market share first, profitability second.

Let’s zoom into 9 quarters and future projections. The reasons for the drop in net margins are explained above.

The main catalyst for Padini, which follows my thesis is that Sept Q 2015 is the start of margin recovery which will be sustained now that the effects of GST is normalized and the revenue from all the new stores are kicking in. As a side note, Padini has been very impressive, chalking up its strongest Q ever while consumer sentiment was at its weakest.

Looking at red dotted line box, I am projecting that adjusting for seasonal fluctuations, Padini will chalk up a record profit of RM135mil vs RM80mil for 2015 (68 %!!) or an EPS of 20.5c. At a forward PE of 15, this allows for a TP of RM3.07. If you want a DCF valuation, look up KCChong or LCChong (are they brothers??)

Is a PE of 15 fair? Today the PE is 14.3 which is not far from that target. If Padini is on a growth trajectory, then a PE of 15 under normal market conditions would not be a stretch.

Can we simply project that sales will continue to be strong? To be honest, I can’t tell for sure. What I do know is that the reason I started studying Padini was because I wanted to buy some clothes (for the first time in my life) and I went to Padini because my friend told me it had quality products at an affordable price. When I went to the store, it was PACKED. I am borrowing some pictures from a fellow blogger (I can’t reference him because my friend passed me his pictures through whatsapp. Sorry bro)

This was during the Christmas season. With lines as long as the Great Wall of China, I think sales will continue to be strong, at least for Dec Q 2015, which will be out in Feb ’16.

As a loose follower of OTB, the technical indicators of the stock has to be right as well. The stock began up trending as early as 26th Oct 2015, when volume and price picked up (possibly due to insiders buying before results). When the Group released its Sept Q results on 26 Nov, it displayed an up-gap the very next day opening at RM1.67.

Subsequently, the stock has been trending between RM1.80 and RM2.00 until 27 Jan ’16 when (pardon my French) shit was hitting the fan across markets, it broke the RM2.00 resistance line. Personally, I thought this was a strong sign because Padini continued to trend upwards while every other counter was dying. Technically, it is unlikely to close below this level of RM2.00 and is on an uptrend (remember, technical charting is a probability not a certainty).

Conclusion

With a 10c dividend yield, buying at about RM2 will give you a yield of about 5%. Think of this as a safety net.

The big question is if you believe that their strategy is finally bearing fruit and strong margins/ profitability is returning to them. Of course, nothing is certain (unless you have insider intel), so place your bets. If their strategy is really bearing fruit, you will be rewarded for betting long. If you want certainty, wait for the Q results. Of course by that time, you may be too late to pick it up (unless another big market slump comes along).

My bet is that they are finally getting the profits that they deserve, and Sept Q ’15 is the first of many strong Q. Could I be wrong? Of course. As OTB puts it, “I am not God.” However, if I am right for the next 3Q, RM3 is really not such a fantasy.

Happy investing/ trading ya’ll.

Cephas

Appendix:

SWOT analysis

Strategy

- Value for money quality clothing at affordable prices through Brands Outlet

- Grow multi-brand stores (Padini Concept Stores), which have significant operating efficiency of distributing multiple group products

- Single outlet with all brands under one roof

- Lower price/sq feet due to larger rental space

- Lower overheard cost/ revenue

- Quality products to price sensitive Malaysian consumers

Opportunity

- Increasing number of shopping malls in Malaysia

- Growing middle class which is being squeezed

- Price Control and Anti-Profiteering: 18 months from 01 January 2015 till 30 June 2016, traders and retailers are not allowed to increase their net profit – subsequent, may increase prices

Threat

- Online retailers (Lazada etc)

- Foreign multinational brands

- Local brands

Strength

- Strong branding presence – Padini, Brands Outlet

- High efficiency of working capital use

Weakness

- Purchase unit trust

- Depressed margins

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on The dude series

Discussions

15 people like this. Showing 34 of 34 comments

"I do have a CPA though (please don’t start stoning me saying that Accountants make bad investors)"

Where is the statistical significant data saying that accountants make bad investors? It is just a sweeping statement.

Accountants may not be the best investors, but having the knowledge of the business will certainly avoid losing big in the stock market.

Which is more important, making big or avoid losing big in the stock market?

I will definitely vote for the later. That should be the same for most retail investors.

2016-02-01 19:19

Accountants are not comfortable with concept stocks.

For concept stocks, one have to approach Marcus Chan CFA, CIMB.

2016-02-01 19:24

Thank you for a pains taking write up. In one sweep you have painted a picture of more than a thousand words. Your sharing is much appreciated. Salute.

2016-02-01 20:26

Wow, thanks for all the kind words and encouragement bracoli, kcchong, duitKWSP, KL foong, apini, pputeh and icon8888!!

I am honored!!

2016-02-01 20:38

"If you want a DCF valuation, look up KCChong or LCChong (are they brothers??)"

"Over the four seas, all are brothers"

KCChong has leaarned some DCFA from LCChong before.

2016-02-01 20:40

Very nice write up, a lot of effort has been put into this. Thank you! Hope to see more write up from you in the future!

2016-02-01 21:14

Thanks alpha, teck chuan, seius and maroken!

Will write the next piece after another thorough round of analysis!

2016-02-02 01:00

Look for capex last 5 years and ROIC. This will provide a better view on expansion plan and real return. I hv wrote about Padini many months back, I remember their capex was high (indicates expansion) and ROIC of 38%.

2016-02-02 08:29

cephasyu, great job!

I am investor of Padini too. I enjoy reading your article, hope to see more in future, keep up the good works.

Take care and thank you.

2016-02-02 08:40

Cephasyu. It was a pleasure reading your write-up. Nicely written with good informative pictures, graphs, comparisons and appendices. Please keep up the good work. Would like to see more of your write-ups which is really refreshing and enjoyable to read.

The following are my 2 cents opinion:

1. What do you think of the prospects of Padini venturing into the online business and how does this contribute to Group's topline and bottomline? Do you see this as an opportunity or a weakness versus existing competitors who are in that field?

2. What is the contribution to the Group's topline and bottomline for foreign sales transactions and how does the fluctuation in forex affect the Group?

3. On the comment for Price Control and Anti-Profiteering, I don't think this is relevant or even applicable to the Group. They are not in a position to raise their selling price significantly especially given a tonne of competition from both online and offline. Hence, they are sticking to their strategy/niche which has been clearly articulated in your write-up.

4. It would be good if you can show some information or graphs and comparisons from the cashflow perspective, especially on FCF and how well the funds have been used for working capital, organic growth/expansion and for dividend payouts to the shareholders.

2016-02-02 19:33

Wow thanks, I am so flattered by all these encouraging comments. Thanks winner, sosfinance, unclejoe, shinado, jason, insider and newbhere!

Speakup, I am not quite aware about Padini contemplating takeovers. I can only source publicly available information, and I have not stumbled upon any sort of news like that.

Newbhere, thanks for your questions. I will try to address some of them quickly, however I suspect that my answers may be a inadequate.

1. Online sales is a tricky distribution channel . Padini has mentioned that they are exploring this avenue. However I have seen brick & mortar business like Parkson try to venture into the online space and fail. I would actually prefer them to focus on what they're good at and excel at it. There are still plenty of Malaysians who prefer to shop in malls. I see the pressure of Padini to venture into the online space as a threat, really.

2. Foreign contributions as I mentioned is about 5-6%. I didn't find disclosures on effects on net profit. They have recognised some foreign gains in recent quarters but it's negligible to my overall thesis. My friend has asked me about the possibility of foreign expansion, and I think that while it is a possibility, Malaysia still has enough room to grow, and they are doing it well.

3. My investment mentor did tell me that the Anti-profiteering act may be irrelevant. You're right in pointing it out. I added that in because it could be a possibility (mentioned in their latest Annual Report), as unlikely as it may seem/ it may even be a bad idea.

4. Unfortunately, this exercise is a little tedious, and I decided against it in this article. I do appreciate DCF/ FCF analysis though, and thought that LC Chong has done a good job with it. I might dare to borrow his work instead.

http://klse.i3investor.com/blogs/kianweiaritcles/87393.jsp.

Overall though, I am grateful for your comments (: Thanks Newbhere!

2016-02-02 22:40

Oh lol Ian sorry the late reply.

Yes I did make all the charts myself (besides the Bloomberg ones/ commodity ones). Thanks for the compliment

My mentor is a low key dude. He's one of the biggest individual investors in nestle

2016-02-20 11:23

cephasyu Thanks for the nice charts. You have done a lot of work and this is much appreciated. For someone who is looking for a annual return of 15% or more for the next 5 years, what would be the buying price of Padini to get this return over the period?

2016-02-20 11:48

Hey 3iii. Thanks for the nice compliment :)

Unfortunately your question is a little too difficult for me. Projecting 9 months ahead is really difficult, even more so 5 years ahead. There could be a variety of factors which may swing padini's fate in the future. Online shopping could really pick up in Malaysia. Padini's over ambitious expansion could have a backlash at them when the economy takes a massive hit. I can't predict the future, I can only make bets.

What I can tell you is this is a high ROE (excluding unit trust/cash) company that has delivered and consistently paid dividends for the past 2 years. They have also been successful in building their brand and p I wouldn't mind holding it for the long run, but at the same time I would be diligently looking at Q results and annual reports whenever they are available to keep reassessing my buy/ hold call.

So I'm sorry I can't give you that sort of answer. If you want a hold and sleep type stock, I think maybe the only one I can think of is Berkshire Hathaway. But then again that's until that old man kicks the bucket

2016-02-20 21:51

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

THE INVESTMENT APPROACH OF CALVIN TAN

2

My Trading Adventure 2025

3

My Trading Adventure 2025

4

All Official Update

5

Bursa Stock Talk

6

Readers' Digest MY

Japan’s Telecommunication Boom: Innovation, Growth & the Future

7

My Trading Adventure 2025

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

bracoli

Best nye

2016-02-01 18:31