The Edge - Insider Asia’s Stock Of The Day

Insider Asia’s Stock Of The Day: MAGNI (18/08/2015)

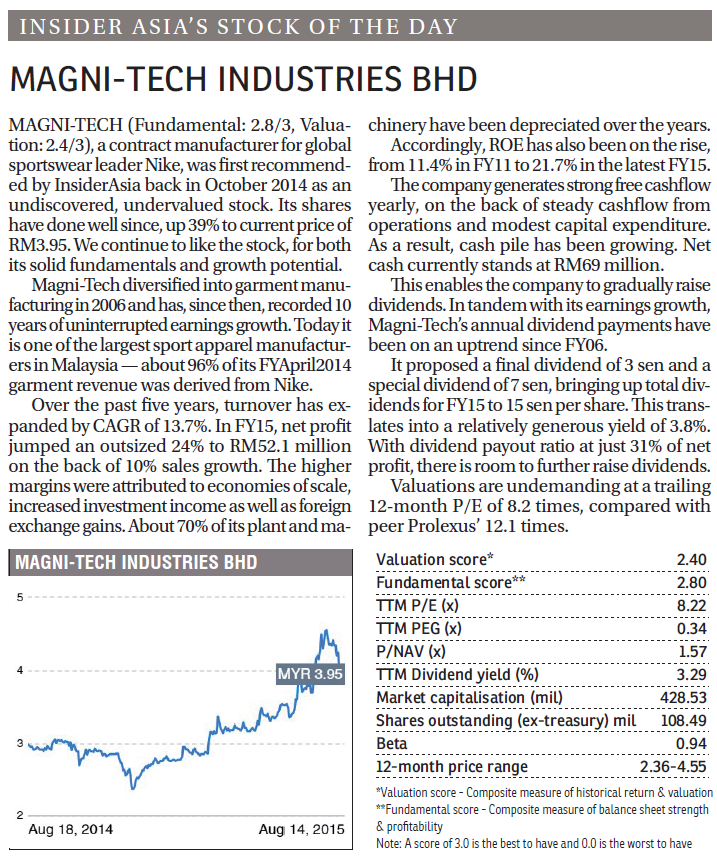

MAGNI-TECH (Fundamental: 2.8/3, Valuation: 2.4/3), a contract manufacturer for global sportswear leader Nike, was first recommended by InsiderAsia back in October 2014 as an undiscovered, undervalued stock. Its shares have done well since, up 39% to current price of RM3.95. We continue to like the stock, for both its solid fundamentals and growth potential.

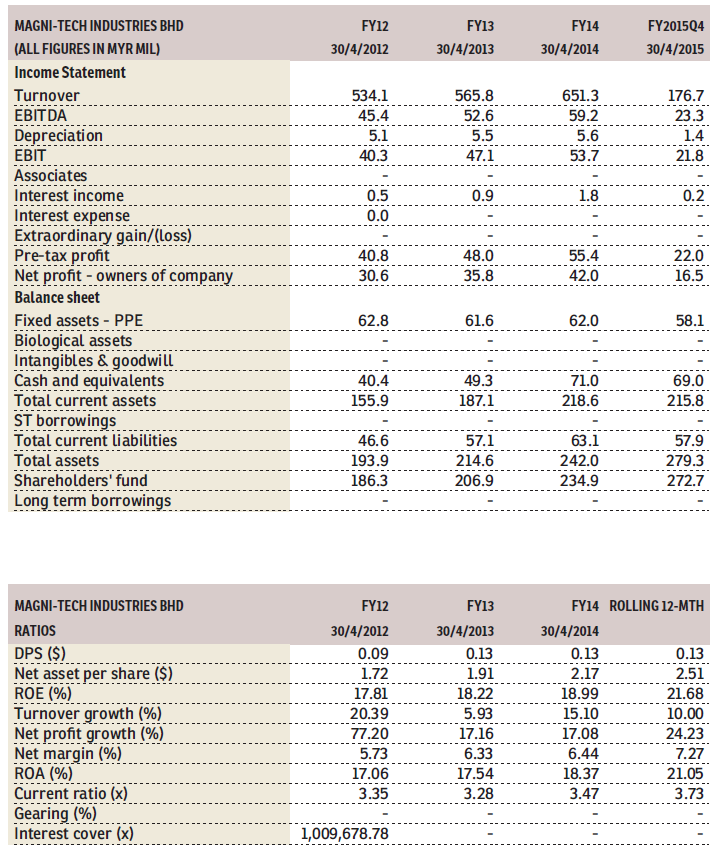

Magni-Tech diversified into garment manufacturing in 2006 and has, since then, recorded 10 years of uninterrupted earnings growth. Today it is one of the largest sport apparel manufacturers in Malaysia — about 96% of its FYApril2014 garment revenue was derived from Nike.

Over the past five years, turnover has expanded by CAGR of 13.7%. In FY15, net profit jumped an outsized 24% to RM52.1 million on the back of 10% sales growth. The higher margins were attributed to economies of scale, increased investment income as well as foreign exchange gains. About 70% of its plant and machinery have been depreciated over the years.

Accordingly, ROE has also been on the rise, from 11.4% in FY11 to 21.7% in the latest FY15.

The company generates strong free cashflow yearly, on the back of steady cashflow from operations and modest capital expenditure. As a result, cash pile has been growing. Net cash currently stands at RM69 million.

This enables the company to gradually raise dividends. In tandem with its earnings growth, Magni-Tech’s annual dividend payments have been on an uptrend since FY06.

It proposed a final dividend of 3 sen and a special dividend of 7 sen, bringing up total dividends for FY15 to 15 sen per share. This translates into a relatively generous yield of 3.8%. With dividend payout ratio at just 31% of net profit, there is room to further raise dividends.

Valuations are undemanding at a trailing 12-month P/E of 8.2 times, compared with peer Prolexus’ 12.1 times.

This article first appeared in digitaledge Daily, on August 18, 2015.

Insider Asia’s Stock Of The Day: MAGNI (18/08/2015)

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on The Edge - Insider Asia’s Stock Of The Day

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

https://dividendguy67.blogspot.com

3

4

Good Articles to Share

Could Kamala Harris beat Donald Trump in November's presidential race?

5

Good Articles to Share

Iranian warship capsizes during repairs in port of Bandar Abbas

6

Good Articles to Share

7

Good Articles to Share

Jonathan Turley unveils exciting new book 'Free Speech in the Age of Rage'

8

Good Articles to Share

Why Impossible Foods signed hot dog-eating legend Joey Chestnut #yahoofinance #youtubeshorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....