The Edge - Insider Asia’s Stock Of The Day

Insider Asia’s Stock Of The Day: SUPERMX (15/12/2015)

This article first appeared in The Edge Financial Daily, on December 15, 2015.

Supermax Corporation Bhd

![]()

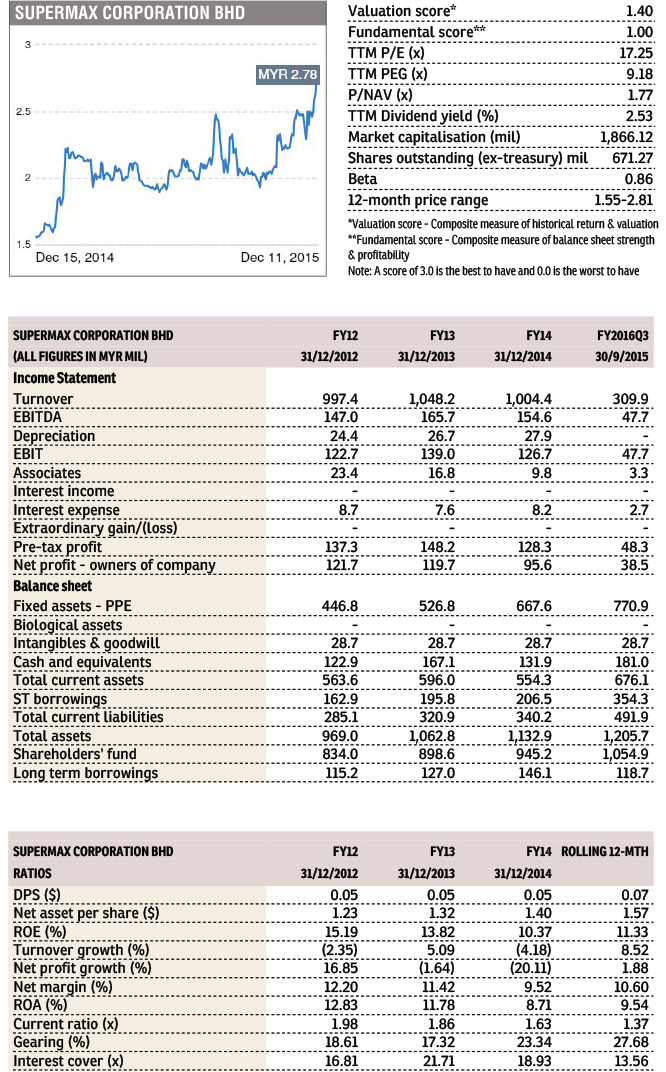

WE continue to favour Supermax (Fundamental: 1.0/3, Valuation: 1.4/3) for its comparatively undemanding valuations and strong growth potential. Its peers Hartalega, TopGlove and Kossan are trading at trailing 12-month P/E of 25.2-40.8 times and 4.3-6.5 times book. In comparison, Supermax is trading at 30-50% discount with trailing P/E of only 17.2 times and 1.8 times book.

The stock has been a laggard for the past one year (+47.5% year-to-date) compared to the other Big Four glovemakers (+62.2-146.9%). This was partly due to repeated delays in commissioning its new plants, which affected its financial performance. However, we believe Supermax has largely overcome the issue, judging from its latest quarter results.

For the quarter ended September 2015 (change in FYE to June from December, starting FYJune2016), revenue grew 11.3% y-y to RM309.9 million, thanks to higher output from the new production lines and efficiency gains. Net profit surged 38.3% to RM38.5 million, boosted by increased sales of higher-margin nitrile glove and the stronger USD.

Going forward, we expect Supermax to continue its strong double-digit growth momentum, underpinned by the two new plants in Meru, Klang, which has started production in batches since early 2015. The plants will have a total of 40 production lines with installed capacity of 600 million pieces of nitrile gloves per month.

When fully commissioned at end-2015, total production capacity will increase by 40% to 25 billion gloves per year. Higher-value nitrile gloves will then account for 53% of its total installed capacity.

Supermax was recently awarded one of the licenses to supply medical gloves to the UK’s National Health Service (NHS) for the next four years. The NHS, which covers all hospitals in the UK, consumes approximately GBP50 million (about RM327.6 million) of medical gloves per year. Assuming a conservative 25% market share, this contract alone would contribute an additional 8% to its topline, starting FY2017.

http://www.theedgemarkets.com/my/article/insider-asia%E2%80%99s-stock-day-supermax

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on The Edge - Insider Asia’s Stock Of The Day

Discussions

1 person likes this. Showing 4 of 4 comments

A co unfairly bullied and sold down on instruction .gods great .Allow other funds to collect and participate the growth of a well managed blue chip. The wind is blowing ur direction Let the share fly .Show them!!!!!!

2015-12-24 21:36

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

https://dividendguy67.blogspot.com

3

4

Good Articles to Share

Could Kamala Harris beat Donald Trump in November's presidential race?

5

Good Articles to Share

Iranian warship capsizes during repairs in port of Bandar Abbas

6

Good Articles to Share

7

Good Articles to Share

Jonathan Turley unveils exciting new book 'Free Speech in the Age of Rage'

8

Good Articles to Share

Why Impossible Foods signed hot dog-eating legend Joey Chestnut #yahoofinance #youtubeshorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

elixir

With fact10and11ready capacity wud be further boosted .being a laggard catch up game to reflect industry norm esp pe multiples gives the co lots of catch up game to do .With new UK contracts and improved revenue and weak rm profit bottom line shld improve .with top glv selling at fwd pe of 25 times spmax shld follow suit and expected to hit rm5 soon

2015-12-22 23:55