Ultimate undervalue club

Why Sam? (TP:RM10.15) - Order book increased to RM4.5 billion, quarter result and AGM update

itjustabouttheprofit

Publish date: Sat, 05 Sep 2015, 12:21 AM

EPS estimation : 13.70+18.25+15.71+20

(estimated) = 67.66sen

PE ratio : 15 (higher PE ratio due to stable

income in the next 5 years, pure cash

company with no debt, high dividend yield,

high barrier of entry and etc)

Target price : RM10.15 (3 to 6 months) -

will be higher for long term

I am here to ANSWER a simple question.

Why SAM? (Updated version)

1) Total order books of RM4.5 billion for

the company (Aerospace+Equipment

Manufacturing+Precision Engineering)

2) Recover in Equiment Manufacturing

sector

3) Appreciation in US dollar

4) Strong balance sheet of RM116million

cash with zero borrowing, dividend yield of

6.5%

5) AGM update

1) Total order books of RM4.5 billion for

the company (Aerospace+Equipment

Manufacturing+Precision Engineering)

As per annual report pages 8, the company have RM3 billion order book in aerospace product. On 28 Aug 2015, the company website have announced that the company have secured another RM520million contract in aerospace product.

http://www.sam-malaysia.com/wp-content/uploads/2015/08/Latest-News_28-Aug-2015.pdf

Also, from the information from chief executive officer by attending Annual General Meeting, the company have another RM1 billion in equipment manufacturing and precision engineering sector. The breakdown are as below:

Calculations are as follows:

| RM | |

| Total order book as per annual report 2015 | 3,000,000,000 |

| Order book from equipment manufacutring and precision engineering (information from AGM) | 1,000,000,000 |

| New contracts on 28/08/2015 | 520,000,000 |

| Total order book as per 28/08/2015 |

4,520,000,000 |

With the RM4.52 billion order book, the company will able to maintain revenue for the latest quarter, which is RM134million for 8 years!!! (32quarters x 134 = RM4.288 billion)

2) Recover in Equiment Manufacturing

sector

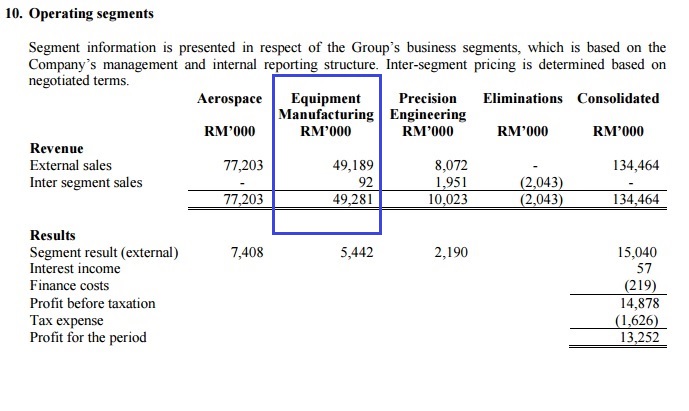

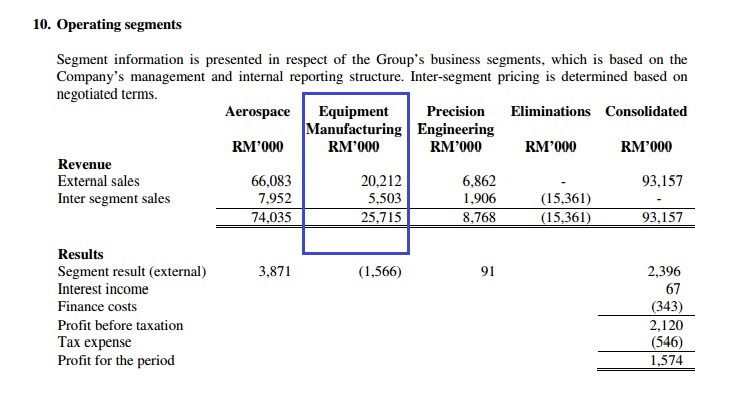

From the AGM, chief executive officer, Mr Jeffrey Goh Wee Keng have highlighted that the equipment manufacturing sector have been recovered from downturn. As mention by him, equipment manufacturing sector have faced downturn during financial year 2013 and 2014 due to flood incurred on Thailand on 2011. On 2012, the company received huge order on equipment sector. It caused the company's earning spiked during Mar 2012 and June 2012.

With the huge order in Mar 2012 and June 2012, the equipment sector have incurred downturn during 2013 and 2014. According to Mr Jeffrey, the equipment started to recover during 2015. It have reflected in latest quarter result.

30 June 2015

30 June 2014

As per quarter result above, we have noticed that the equipment manufacturing sector have jumped doubled on 30 June 2015.

3) Appreciation in US dollar

Refer to Q4 FY2014 and Q1 FY2015, exchange rate traded between USD1= RM3.5 to RM3.75. For Q2 FY2015, the USD spike up to USD1 = RM3.75 to RM4.25.

As the selling price determined in US dollar, the increased in currency rate will further improved the revenue and earning for the company as most of the business trading in US dollar.

4) Strong balance sheet of RM116million

cash with zero borrowing, dividend yield of

6.4%

Currently, the company stood at RM116million cash which is RM1.37!! Also the company did not have any borrowing. Also the company rewarded the shareholders with 6.4% or 33.2sen dividend to shareholders during last financial year.

5) AGM update

Here is some of the useful information getting from attending the AGM:

1) The management planned to expand the production by building another factory at Batu Kawan. The factory expected to start operation during 2017.

2) The new factory expected to reach full capacity in 2020.

3) SAM is currently stood at 30% market share in engine casing industry in the world. SAM have 3 competitior. One from France, one from South Korean and another one from Taiwan.

4) The second largest shareholders have higlighted the illiquidity of the share. He proposed the company to have bonus issue and share split to increase the number of shares of SAM. Management said they will consider on the proposal.

5) The second largest shareholders also concern as the company holding too much cash. The management replied that the company will used the cash for acquisition of new business, growing of business and buying raw material.

6) The second largest shareholders to ask to reward the employees as the employees are skilled employees. He also suggested to the management to split the dividend in 2 times.

7) The management forecast that the company are able to archieve RM550million revenue this year.

8) The company will invest USD50million between 2015 to 2020 for the purchase of fixed assets.

9) The company hired more staffs during the year compare to last year as equipment manufacturing sector recovered during 2015.

10) Most of the cash are kept in US dollar as most of the transaction traded in US dollar.

After the AGM, the management have arranged factory tour for shareholders of the company for aerospace factory. Due to the employees not allowed us to take photo inside the production line, hence I am unable to take any photo inside the factory. These is some of the picture I am able to snap during the factory tour.

This engine costs around USD400,000 per pieces according to one of the employees (right side). Hence we walked with extra care during the factory tour to make sure the engine case did not suffer any scratches or damages.

Trade at your own risk!!! Do research before any investment decision!! Happy trading :-)

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Ultimate undervalue club

Why MMCCORP? Undervalue world Top 10 port operator with 2 listed subsidiary company

Created by itjustabouttheprofit | Dec 08, 2020

Why Genetec? Another alternative to investors who miss Dufu (HDD company) - PE6.27

Created by itjustabouttheprofit | Sep 04, 2018

Why Cscstel? Pure cash steel manufacturing company (281% increase in profit)

Created by itjustabouttheprofit | Aug 28, 2016

Why KESM (RM4.81)? Stunning quarter result, net cash company with high NTA (RM6.52)

Created by itjustabouttheprofit | Jun 05, 2016

Why AAX? Low cost carrier benefited from weakening of USD dollar (TP:??)

Created by itjustabouttheprofit | Apr 16, 2016

Discussions

7 people like this. Showing 40 of 40 comments

he is assuming us dollar remains strong for 8 years

he assumes eps at least 20 sen per quarter for the coming 32 quarters

he assign PE of 15

base on the carrent price of 5.2, EV about 600M and EBIT about 53M do you think it is still cheap to buy under current market sentiment with plentiful of lelong buys ? learn from KC, though you may miss the best but far from wrong.

2015-09-05 11:49

My opinion: Now USD currency stood at USD4.30 as per yesterday. Do you think that the currency rate against will be recovered in the next few month or even years with the increase in interest rate in US? I assuming 20sen for the next quarter and even higher for the next years as US dollar expected to be more stronger after the interest rate increased. The order book is real and cannot be cancelled so easily. This share is for long term investor. If u wan to play for short term, please ignore this share and move to other more speculative share. Thank you

2015-09-05 12:02

my opinion:

there also many similar real as you as you said, now is buyers' market. who want to pay more for long term investment? please look at the time frame for the forecated TP, 3 to 6 months , isn't it the writer himself encourage short term play.

2015-09-05 12:19

Put a TP is encouraging short term play? Haha. Ok you win. I wont reply your point as it is a flame and the discussion will never end or end with both part do not happy with each other. I will only reply to the discussion about the fundamental part of the business. Thank you.

2015-09-05 12:45

it is not the matter who win who lose,

we are talking about valuation

why do you need to think of win or lose

why just can not be share of different opinion?

2015-09-05 12:47

pisanggoreng...

u have any stocks to recommend

any TP..long term / short term

and how does it compare with SAM?

I see when we comment something either bad / good..logical/illogical

is all relative...

so..unless you give us something to compare..

your comments not valid leh..;)

2015-09-05 13:12

Keyword = its all relative...

unless we have a reference point to compare

all direction/argument/opinion given are useless = no meaning :(

2015-09-05 13:14

relative in term of what ?

not valid? before I am given a chance to share.

Posted by Probability > Sep 5, 2015 01:12 PM | Report Abuse

I see when we comment something either bad / good..logical/illogical

is all relative...

so..unless you give us something to compare..

your comments not valid leh..;)

2015-09-05 13:24

ok fine pisanggoreng...

I think the essence of this article in terms of relative valuation is PE lorr..

but I do feel PE=15 is high side...but balance sheet and all luks superb, perhaps it deserve it.

which one you recommend leh? what the EPS and PE..balance sheet superb?

2015-09-05 13:29

probbility,

my key word is not PE

neither it is balance sheet

my key word is " value buy"

if PE is your focus then do you need me to recommend

if PE + balance sheet is your focus, I believe, with your knowledge , you also need not have my recommendation,

why so difficult to have my recommendation?

just browse through my past comment you will get everything you want.

right?

share with me

I am willing to learn from my mistake

2015-09-05 13:40

I have a feeling you are probably pointing towards GADANG...

but I am very very scared with property counters..

PE can be very low and sell way below NTA..

but never move up! People already have some phobia with properties..

:(

2015-09-05 13:54

But I really haven't investigate on Gadang..

if its future earning visibility is there like SAM

I think its really selling cheap.

2015-09-05 14:01

generally you are right. people scare of property counters

do you think , isn't it now is the time for most of us to have a look at the property counter after quite a long time of phobia...

who know it may turn out weakening ringgit can be a blessing to this sectors..

nothing is certain, we only can act on what we think right may not be the best.

2015-09-05 14:07

gadang is a well diversified company, construction is still the main contributor to its profit, earning visibility for the coming year is unquestionable, further than that we better ask the fortune teller

2015-09-05 14:11

most important , now it is selling at unbelievable cheap price, with its net market worth not more than 3 time its PBT whereas sam is almost 12times.

what I can say with condident, as some sifu had said "if win you win big , if lose you lose less"

2015-09-05 14:15

Noted...worth to investigate. Its last dividend had improved.

Really strange why it has been dipping.

K..thanks pisang..bye

2015-09-05 14:15

To answer your question why i put PE15. First it is a pure cash company. Second it paid a huge sum of dividend. Just for the last year, the company already paid 80 to 90 percent of the earning of the company. 3rd huge contract sum that can secured for at least 8years. How many companies in Malaysia got a huge order book that can last for 8years time? 4th huge market share of 30percent in aerospace engine case. 5th good reputable client. If u notice the client of the company, they also having a very clean balance sheet. Somemore if u calculated the trade debtor turnover days, it is less than one months. 6th the company is growing. Usually the company with high grow will have a better PE ratio. 7th the profit have been quite stable for the last 3 quarter. The profit not changing much for the last 3 quarter. So why not worth putting PE15?

2015-09-05 15:12

itjustabouttheprofit,

oh.. you are the writer.

good work, thanks

using your principle of all work well condition, you please calculate and compare the return in next 12 months, with gadang 12 (cp 1.17) and sam 15 (cp 5.2), you will see what I mean by value buy.

2015-09-05 15:43

I dun know about Gadang and I do not do any research on Gadang. Sorry to say that I hate to comment on the share I did not do research. Usually I need at least 1 week to do a detail research and I only believe in myself as I done my own homework before make any comment. I write this because i understand on SAM. I attended that AGM and do alot of research on it.

Also, the drop in oil price will encourage more people to travel as the ticket price of airline will be drop. Hence more aeroplane will be order by airline company. It is a good news for SAM as the company is one of the indirect beneficial company for low oil price

For me, like others, I dun have any plan to invest in any construction/property/ palm oil/oil industry as this sector will not perform well in this few years.

What I know about Gadang is a construction, property, palm oil company. I dun like construction as the profit margin will go down because they need to import material from oversea. No additional contract value will be added for the contract which sign long long time ago but u still need to perform the contact although your company suffer loss on the contract. For property, the volume of transaction for property sector have significant gone down after government implementing RPGT and GST. To avoid risk, I am avoiding to invest in any property and construction sector.

For palm oil, the price of palm oil are not enough attractive to enter as the profit margin for palm oil is quite low for now.

The detail of Gadang I also not sure. How many debt, cash, trade debtor turnover, quality of trade debtor, dividend yield, whether the management is good or lier, director contribution and other stuff. This is my other concern before i bought the shares. As per reason mention above, I wont do any research on it as I will not buy the shares as I need to utilize my time for the research for other company.

I suggest you to write an article regarding on Gadang to explain on the company then maybe I will comment on it.

Thank you :)

2015-09-05 16:14

For the return part, it will depend on the market view on that particular sector. As you can see for oil company, previously most of the oil related company trading in around PE20. As of now, you can see alot of oil company which trading around PE5-8. For me, when the sector is doing well, the PE ratio will jumped. If not doing well, I will go down. Same applied to the property company now. Just my opinion.

2015-09-05 16:19

Ya, concentrate on individual counters, not current general mkt trend and remember ""anytime is a good time to invest"".

2015-09-05 19:18

itjustaboutprofit,

there are a few things that I wish to straighten here

1. I know you had done a lot of research about sam and spent a lot of time in your hardwork, but that does not mean or guarantee you conclusion is accurate or correct and accepted by the market

2. I am more realistic, I do not interested to know what is going to happen from now till 8 years later. I am more interested in what is going to happen in the coming 1 year

3. I do not like to discuss with you based on common sense or beautiful future things, I prefer to use real data to assess whether a company is worthwhile at the current price for me to put in my money. can you tell me what is the enterprise value multiple of SAM as compare with gadang?

4. as you have said you do not know gadang, then how do you know her construction and property sector are not going to do well? base on common sense? or your friends told you? as you said cheaper oil more airplane order, if this is the case, then more houses will be built as there are more people getting married, and also more airport got to be built to accommodate more aeroplanes flying in the air.

5. you do not know gadang does not mean she is not better than sam in term of valuation.

6. you do not know gadang , does not mean she is not making more and more money from both construction and property, please check your fact before you comment on gadang that you have claimed many times that you are not interested.

let me go for my dinner first before i come back to you, bye

2015-09-05 19:36

I bet you havent finish reading my article then comment. Opps... See 2nd point?Talking about 8 years later? *Facepalm* 3rd point USD? 8 years later rate? *Facepalm* 4th point the balance sheet 8 years later? Another *Facepalm*.

One more thing, you comparing difference industry. Gadang not same with SAM while SAM not same with Gadang. If you wan to compare, please compare to other property company such as huayang, matrik, mahsing, spsetia, ecoworld and etc. If like that I also can compare Apple. PE ratio way more higher than SAM.

Keep in mind that please respect on the place that I written my article. "DO NOT PROMOTE YOUR OWN SHARE IN OTHER PEOPLE ARTICLE. I AM NOT INTERESTED TO KNOW ABOUT GADANG." As i mention just now, I talked about the industry in general not about GADANG. It is my general view on the industry on oil palm, oil industry, property and construction. I thought you just wan to know my view. Am i talking about GADANG? I just talking about the industry involved for GADANG. I AM NOT INTERESTING IN ATTACKING YOUR NOR TALK ANYTHING BAD ABOUT GADANG.

THIS IS MY LAST REPLY ON YOU. I AM NOT INTEREST TO REPLY YOU ANYMORE. YOU REALLY DID NOT READ BEFORE REPLYING ANYTHING.

2015-09-05 20:05

Anyway thank you for making my article become top3 article in i3vestor... Thank you for doing free promotion on me. Cheers... I will disappear in your view..

2015-09-05 20:06

very good counter to invest in long term. itjustabouttheprofit do you factor in ICULS for EPS calculation?

2015-09-05 20:35

SAM is a value buy. I doubt spectacular growth is coming but the huge order book is a good anchor for investment.Buffet is making the same bet on aircraft industry as well.Strong cash flow is another plus.

However, current eps should only be around 40 cent.

The dilution of la need to be taken into consideration.

2015-09-05 21:44

1. PE15 is something that you assign thinking that it is 'fair' and the market will agree with you, at the end of the day, you have to rely on the market to agree with you.

2. PE15 is anchored on profit/earnings not revenue. And this PE15 and TP thesis can only survive if profit increase in lock step with revenue, which i think is a bit too simplistic or straight forward. Think of it this way, if this is a software company that gets awarded for more contracts, the marginal cost is minimal, because it is software. Now you are looking at a company that manufacture highly precise equipement for aerospace. In order to handle those contracts, well you will need more highly skilled workers, inventories, manufacturing sites, raw materials, all of them goes into working capital and require high capex. Maybe they can improve their margin or maybe not, not you get my point.

2015-09-06 08:42

Another thing i like to add is your EPS estimation. This is everyone preference, some think it is essential to do EPS estimation some doesnt. But i do like to raise something that you need to be careful of. No doubts you are a person looking for undervalued counter, but i do find that when it comes to EPS estimation, your estimation is close to overly optimistic.

I read back your blog post about Supermax back in Aug 2014. You estimate their EPS starting 2Q2014 all the way to 4Q2015 as below

2Q2014 - 4.5cents

3Q2014 - 6

4Q2014 - 7

1Q2015 - 8

2Q2015 - 8

3Q2015 - 8

4Q2015 - 8

So how did it turn out?

2Q2014 - 3.93cents

3Q2014 - 4.09

4Q2014 - 2.95

1Q2015 - 3.67

2Q2015 - 3.64

3Q2015 - Yet to come

4Q2015 - Yet to come

You overestimate EPS on average every quarter by 14% to 119%, and in total your estimate is 33.5cents, while actual EPS is 18.28cents. And that is something you need to be weary of, and i did warn you back then about your EPS estimation. It is good now you can go back and evaluate how did you come up with such a sky high EPS estimation, or else you going to make all the same mistake on Magni, SAM etc.

2015-09-06 09:11

Did you ask management what is time frame of the delivery for those awarded contracts ? What is their plant current utilization rate ?

2015-09-06 11:33

Sam's world class business portfolio in aerospace part manufacturing is with high barrier of entry. Gadang is in construction industry which you can find thousands of industry players in the same league. So, it is totally different and you can compared a world class manufacturer with local construction players.

2015-09-07 17:02

yes, sound management team, solid major shareholder natural of the their business form qualitative part of the company's value u can't count it through figures! maybe in numbers gadang is more value buy than sam but when u look at qualitative parts u know the answer

2015-09-08 00:44

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return

Latest Videos

Apps

Top Articles

1

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

2

南洋行家论股

4

RHB Investment Research Reports

5

The Alpha Trader

6

7

Koon Yew Yin's Blog

8

How to become a resilient trader

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Probability

very nice..colorful presentation...

I am confused between Magni and Sam..which is to invest more now..

2015-09-05 00:33