Choivo Capital

(CHOIVO CAPITAL) AEON Credit Service (M) Berhad (AEONCR: 5139): Much Ado About Accounting Standards

Choivo Capital

Publish date: Sat, 21 Dec 2019, 05:58 PM

For a copy with better formatting, go here, its alot easier on the eyes.

AEON Credit Service (M) Berhad (AEONCR: 5139): Much Ado About Accounting Standards

===================================================================

Well, it’s been awhile. There are a few reasons, but I’m not here to talk about that.

One of the companies I’ve always admired was AEON Credit Service (M) Berhad (“AEONCR”). I have never done too deep an analysis on this company before, however, its performance and the economics of the business always impressed me.

I remember when I first read the accounts in 2016, my first thought was:

“This company is probably a scam”

Yes, i was that stupid.

It was the first time I had read the “Statement of Cashflows” of a Non Deposit Taking Financial Institution, or that of a financial institution, period. And the constant drawdown of borrowings made me think this company was borrowing money to pay dividends.

I could not have been more wrong.

After a couple hours, I’ve understood it better, and it became the first stock I made a profit of more than 10% on. Unfortunately, due to a temporary suspension of intelligence, I did not hold for long, and instead constantly bought and sold it at increasingly higher prices and paid the transaction fees along the way.

From 2018 onward, due to my deeper understanding of value investing (or perhaps, just my sheer incompetence and lack of talent when it comes to trading), I bought a small position of 1.3% to hold as the valuation was just a bit too rich for me compared to what was available (for the record, it wasn’t really), however, I wanted to keep it around to remind myself to never forget to check again.

A month back, a friend told me the current price of AEONCR and I was quite happily surprised. I did some research, and given my immaculate timing, increased my position to 2% on 25 September 2019, the day before the release of the Q2.

Thank god I knew enough of my own weakness, that I learnt how to size my investments purchases.

I’m writing and sharing this because, I’m currently considering making AEONCR a significant portion of my portfolio. However, this is one of those companies, where despite reading every single annual report, investor presentation and recent analyst pieces, I just can’t seem to shake the feeling that there is something I don’t quite understand about the company.

As an intelligent, honest but abrasive friend told me recently when I asked him about this company, “I’m now certain that you know absolutely nothing about financial institutions or AEONCR”.

Well, I hope to be educated by the people here.

Enough Grandmother story, lets begin.

AEON Credit Services (M) Berhad (AEONCR: 5139)

Introduction

Just for a bit of background, 2 years back, I’ve written a little on how to value financial institutions,

The Valuation of Financial Institutions

I’m sharing the link, so that those who are interested, can understand a portion of the perspective I will be analyzing from.

AEONCR is a non-deposit taking financial institution (“NBFC”), that focuses mainly on various forms of personal lending. They consist of the following divisions:

- Personal Financing (Personal Loans)

- Car Financing

- Motorcycle Financing (Both Kapchais and Superbikes)

- General Easy Payment (But a TV on installment plan for example)

- SME Financing (Quite Small)

- Credit Cards

They have the third highest “Return On Asset” among all the financial institutions, at around 5.5% before tax. The highest is Elk-Desa Resources Sdn Bhd at roughly 6.2% and the second, RCE Capital Berhad at around 5.7%-5.8%. Most banks have ROA around 1%-1.3% with the best bank in Malaysia (and probably South East Asia), Public Bank, having ROA of around 1.7%.

Having said that, as most banks typically aim for much “safer” lending, and are able to take deposits, and on average, leverage up around 10 times. While for NBFC’s, due to the fact they cannot take deposits, and will typically face impairment rates triple that of most banks during a recession, can usually only leverage up 5 times or so safely.

As most are likely aware, the financial performance of this company since its listing on 2008, have been nothing short than extraordinary, as we can see in the table below.

The Business

AEONCR started with “General Easy Payment” or as they now call it “Objective Financing” as its bread and butter. This consist of things like installment payments for television, electrical appliances etc.

However, the growth rate (it actually registered a decline from 2016 to 2019) of this segment lagged far behind those of “Personal Financing/ Personal Loans”, “Car Easy Payments”, “Motorcycle Easy Payments” and to some extent Consumer Products/Credit Cards, resulting it in going from 30% of the portfolio in 2009 to only 4% of the portfolio in 2019.

On a compounding basis, these divisions have grown at,

From 2009 to 2019

Personal Financing: 43.53% Per Annum

Vehicle (Cars and Bikes) Easy Payment: 28.93% Per Annum

Consumer Products: 16.89% Per Annum

From 2013 to 2019

Car Easy Payment: 55.56% Per Annum

Motorcycle Easy Payment: 22.53% Per Annum

And this is with profitability increasing roughly in line. So why is this the case?

The first reason is structural gains.

Secondhand cars and motorcycles are an under-served market segment.

Most banks do not offer financing for motorcycles beyond personal loans, whose rates can go as high as 18%. In addition, motorcycles are quite simply by far the cheapest mode of travel. A Honda EX5 can travel 100km on just 1.8 liters, compared to the best-selling budget car Proton Saga, which requires 5.6 liters.

In addition, an EX5 cost less than RM5,000, while a Proton Saga cost more than RM32,800. To top it off, when travelling via motorcycles, you have no need whatsoever to pay tolls.

A recent Khazanah study showed that, on average, the B40 (Bottom 40% income earners in Malaysia by Household) of Malaysia are able to save just RM76 per month, a fall from RM124 in 2014.

Given such a tiny margin of safety, it’s a no brainer that motorcycles have become the only economically viable mode of transport for the B40 and parts of the M40.

This has resulted in motorcycle sales increasing by 20% YOY for 2019. In addition, in terms of motorcycles sales in the world, Malaysia is ranked number 13, despite a small population of less than 30 million.

As for secondhand cars, many banks have stopped providing hire purchase financing for cars older than 3-4 years. However, it is not as great as a business as the motorcycle loans, as they are still many competitors in it. Having said that, this is mostly due to how amazing the motorcycle loan business is in comparison.

As you can see based on the above chart, their “Car Easy Payment” records a negative Differential (“Share of Income %” – “Share of Receivable %”), ie its share of income is negatively disproportional to the size of the receivables. However, income yields are is still around 12%, and with interest cost of around 4.9%, its still one hell of a business.

Of course, it also helps that AEONCR typically targets B40 and lower half of M40 loans. According to a study, in terms of financial literacy, Malaysia ranks number 66 in with a score of 36/100, slightly below the global average score of 36.58.

However, as many would be aware, the above are all industry economics, that say very little about AEONCR’s edge.

So what is their edge?

The AEONCR Edge

AEONCR’s real edge lies in the sheer quality of their credit assessment and discipline in ensuring good quality assets, the management and their incredible collection processes.

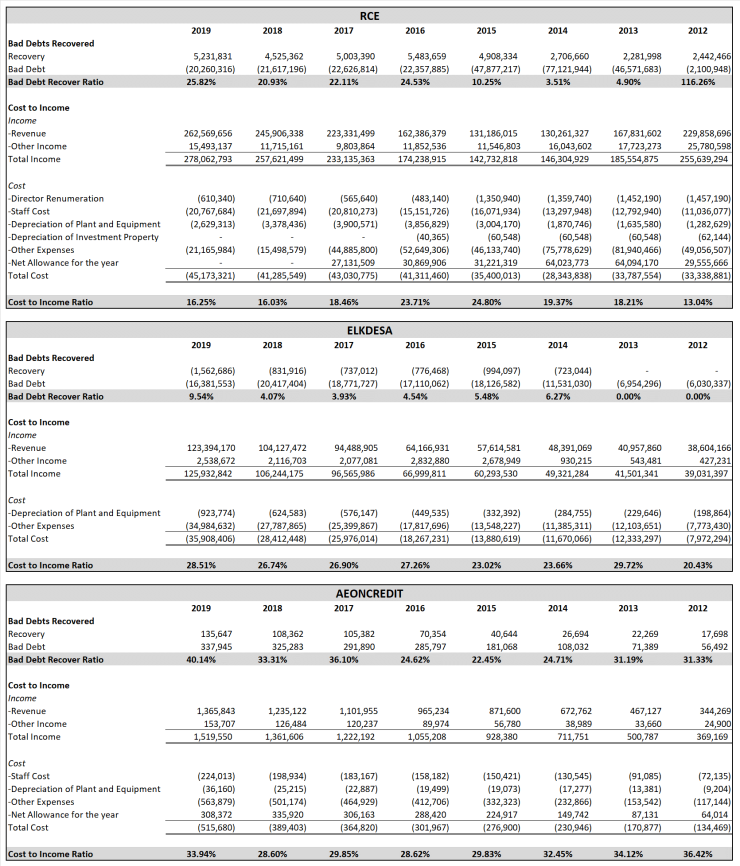

Over the years, despite the large increase in revenue and receivables size, asset quality has largely maintained even or improved with Non-Performing Loan (“NPL”) ratio still holding steady at 2% and have in fact improved over the last 5 years. Since 2007, their NPL have averaged a mere 2.1%.

For the record, Maybank’s NPL is 1.75%, and RCE Capital’s (which obtain repayments via direct salary deduction) is about 4%. As for ELK Desa’s insane NPL of a mere 1%, well, if someone would care to enlighten me as to the reason why this is even possible, i would be incredibly grateful.

In addition, collections ratio of receivables past due for 2-3 months have also increased from 62.73% in 2014 to 71.24% 2019.

The most eye catching of these statistics is their Bad Debts Recovery % (a ratio I derived in order to judge the effectiveness of the collections teams, it’s not perfect, if you have a better one, I’m all ears). This consist of (Bad Debt Recovered / Bad Debt Written Off During The Year).

Thinking about it, it might be better for it to be, (Bad Debt Recovered / Bad Debt Written Off In The Previous Year), but well, i’m a little lazy, and i don’t think it affects the essence of the point i’m trying to make (except make AEONCR’s numbers look a little better and more consistent).

Their Bad Debts Recovery %, has increased steadily over the years from 6.81% in 2007 to 40.14% in 2019.

This is honestly quite an incredible statistic, considering that these are all mostly unsecured loans given to low income earners.

Much of this is due to the sheer quality of the management and their collections team.

And thus, the big question, how do they compare against their competitors, ie other non-deposit taking financial institutes, such as RCECAP and ELKDESA?

As you can see from the numbers above, AEONCR’s Bad Debt Ratio of (40.14%) in 2019, far exceeds that of RCE Capital (25.82%) and ELK Desa (9.54%). And this is despite companies like RCE Capital having the benefits such as guarantor requirements and direct deductions. Utterly incredible.

And interestingly, this does not come at the cost of overly high cost to income ratio. AEONCR’s cost to income ratio is like that of ELKDESA despite having multiple product lines and far more outlets, with normalized percentage being roughly 29%.

The increase in 2019 to 34% is mainly due to additional marketing expenses for the credit card business and to improve cross selling.

RCECAP has an extremely low Cost to Income ratio of 16% or so, due to the fact they only have one product line, and very little outlets, with most sales done through agents.

If one were to visit the Glassdoor and Jobstreet, and look at the comments by both current and resigned members of the collections team, we can comments by them complaining how the targets are always to high, as well as their bonus being satisfactory. Well, you get what you incentivize for.

Interesting, non profit making cost centers such as accounting etc, complain about the lack of bonuses for the past few years.

Quite interesting, does not sound like the place i want to work at (since i’m in financial reporting), but definitely sounds like the kind of company whose stock i want to purchase.

Much Ado About Accounting

As many would have noticed by now, for the last 2-3 quarters, AEONCR have been reporting relatively lackluster results.

Before we talk about it, we first need to understand the new accounting standards being implemented.

Previously the loan book held by AEONCR was recognized based on the accounting standard called IFRS 139. This has been replaced with IFRS 9 for the most recent financial year ended 28 February 2019.

The difference between these two accounting standards are as follows,

| IFRS 139 | IFRS 9 | |

| Nature | Incurred | Expected |

| Timing of Allowance | Upon Trigger Point | At Inception |

| Type of Allowance | One Off |

Stage 1, 2 & 3

(12 month and lifetime Expected Credit Loss) |

IFRS 9 was a new method of recognizing Financial Instruments that was born after the 2008 Financial Crisis. One of the biggest complaints about the crisis then, was that the recognition of credit losses was too little too late.

The previous accounting standard, IFRS 139 used for recognizing credit losses is commonly referred to as an “incurred loss model” as it requires the recording of credit losses that have been incurred as of the balance sheet date, rather than of probable future losses.

This did not allow banks and financial institutions to provision appropriately for credit losses likely to arise from emerging risks prior to the crisis, as it required a trigger point.

And this lack of provisioning effected regulatory capital levels, thus contributing to pro-cyclicality by spurring excessive lending during the boom and forcing a sharp reduction in the subsequent bust.

The reason for this was that loss identification IFRS139 requires a “triggering” events supported by observable evidence (eg borrower loss of employment, decrease in collateral values, past-due status) combined with expert judgment, ie a “Trigger Point” before an allowance or provision can be made.

Under IFRS139, upon the occurrence of a triggering event, the allowance is calculated as such,

Allowance: “Exposure at Default” X “Loss at Default %”

IFRS 9 on the other hand replaces this with a more forward-looking approach that emphasizes shifts to the probability of future credit losses, even if no such triggering events have yet occurred.

Therefore, under IFRS 9, an “Expected Credit Loss” is made upon inception of the financial instrument, as and classified “Stage 1”. And upon any deterioration of the quality of the asset, it is further classified as “Stage 2” and “Stage 3”, and is calculated as such upon inception.

Expected Credit Losses = “Exposure At Default” X “Probability Of Default %” X “Loss Given Default %”

Now, do note that the ”Probability Of Default %” and “Loss Given Default %” changes depending if 12 months is used (Stage 1) or Lifetime is used (Stage 2 & 3).

So, for example,

AEONCR borrows out RM100,000. The probability of default events in the next 12 months is 3%. And in the event of default, they will lose 50%. Therefore

ECL= RM100,000 X 3% X 50%

ECL= RM1,500

Now, the interesting thing to note here is, the “Probability of Default” involves very significant assumptions, one of which is forward looking macroeconomic data.

So, for example, if AEONCR thinks that an economic slowdown is going to occur in the next twelve months, the “Probability of Default” and “Loss Given Default” may very well increase to 5% and 70%, despite no drop in the quality of the loans, resulting in higher allowances.

ECL= RM100,000 X 5% X 70%

ECL= RM3,500

Case in point, in the 2018 accounts, for receivables not past due of RM6.5 billion, an allowance of RM8 million was provided.

While for 2019, for receivables not past due of RM7.8 billion, an allowance of RM203 million was provided. This is despite there being a DECREASE in Non-Performing Loan % from 2.33% to 2.04%.

When investing, one of the things we have to be aware of, is that what is “True and Fair” under the accounting standards, does not necessarily reflect the real economic reality of the company.

For example, Nestle have to spend a huge amount of marketing expenses this year, one can argue that this a capital expenditure for the sake of their Brand name, but this does not change the fact that under accounting standards, it cannot be capitalized, and that the value of their brand, as recorded in the financial statements have not changed since god knows when.

And for good reason, if we could, the numbers would be far worse.

When it comes to accounting standards, it needs to be unfair and inaccurate for a few people, for the betterment of the majority.

As investors, we need to be aware of these differences.

Risk and Downsides

-

Defaults during Recessions.

For unsecured loans (I don’t consider cars, motorcycles and fridges an asset), defaults during recessions are typically significantly higher than secured loans. The question is if the higher interest rates charged (reward) is higher than the cost of the risk assumed.

I would think so.

Looking at their numbers from 2007 to 2009, AEONCR were not affected by the crisis and in fact grew and made more money each year.

And since then, their operations have seen a massive improvement of loan quality, and collections processes. I think they would be able to handle any recessions very well.

Of course, past performance is no indicator of future performance.

-

Bullet Loans

For AEONCR, their loans are structured by way of bullet payments. Ie, the principal needs to paid in full during the end of the tenure with no principal payments in between. Typically, they don’t repay it but instead roll it forward.

In times of crisis, if the loan were to mature during that same year, it may make it difficult to roll it forward then. Things would be quite interesting in that case.

This would be the case for most banks as they usually use the same structure.

Having said it, unless your loan book is rubbish (which its not), you should be fine.

-

Big Banks Giving Loans For Secondhand Cars and Motorcycles etc

Well, they can, and i’m sure that AEONCR will not longer be as profitable. However, Banks typically have rubbish collections teams, or outsource them. Thus AEONCR’s edge should still largely prevail.

As long as one did not overpay, it should be fine.

Conclusion

Personally, I’m quite unsatisfied with this article, and I think it may be due to the fact I don’t understand the business as well as I would like. In addition, the words do not flow as easily, or as well as I would like, probably due to the fact I stopped writing for quite a few months.

My main worry now is if the lower savings rate of the B40 going to affect repayments (it will) in the event of a crisis, and how much?

What is the exact model used to calculate their ECL allowances, and how much of it differs from their previous ones?

Having said that, given the competence and longevity of the senior management (beyond the MD that changes every 5 years or so, as they are not local), such as Ms Lee Tyan Jen who went from Head Of Credit Assessment to Chief Operating Officer.

The focused way of which the management of AEONCR go about in allocating capital (while paying out any excess) efficiently and in a focused manner, without straying far from their circle of competence gives me confidence.

To buy or not to buy?

You decide lah, judge it against the current opportunities you have at hand make your own decision.

In addition, do note that prices and accounting profit may continue to fall for another 2-3 quarters, resulting in potentially more discounts.

Fair value of the company? Currently, its probably somewhat below fair value. However the real value in this company, is that its a great business, and i love business that let me forget about thinking about when to sell.

As always, do let me know if you think differently or feel I have missed out elsewhere.

Disclaimers: Refer here.

====================================================================

Facebook: Choivo Capital

Website: www.choivocapital.com

Email: choivocapital@gmail.com

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Choivo Capital

(CHOIVO CAPITAL) MYNEWS (5275) – Dr CU in da house. 66% Upside

Created by Choivo Capital | Dec 09, 2020

(CHOIVO CAPITAL) WCE (3565) – When the roads align. 562% Upside.

Created by Choivo Capital | Dec 05, 2020

(CHOIVO CAPITAL) BAT (4162) - Budget 2021 (The Dark Knight Rises)

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) LIONIND (4235) - Budget 2021, Rising Steel Prices

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) KRONO (0176) - Is it Alibaba (Alibaba Cloud)? (SUMMARY)

Created by Choivo Capital | Nov 03, 2020

Discussions

1 person likes this. Showing 15 of 15 comments

I quite like the business. The one thing about that co that is not so good was that the management did not leverage up as they should (since its a financial institution they are running) and instead decided to do non stop rights issue.

Recently the management have decided that they would like to leverage up. So that is a good thing.

Second part is that, the payees can't direct transfer in the payments, but have to go to the counter to make payment, which i find very odd.

Of course, this could very well be an edge, if your entire customer base is under banked, but its odd.

===

hpcp Hi Choivo, thanks for the article. What do you think of elkdesa, which has better NPL ratio and business has been growing consistently

21/12/2019 7:32 PM

2019-12-21 21:10

Sslee,

https://choivocapital.com/2018/11/28/the-art-of-valuing-insurance-companies-and-why-teh-hong-piow-is-a-god-lpi/

The problem with Tunepro for me is,

1) They tried to go into general insurance, which is not their edge, travel insurance division is incredibly profitable.

2) Their fund management for the investment is quite bad, some of it is in unit trust, which are just stupid and inefficient. If you dont know what to do, put it in the S&P500 index or smtg. The rest are in MGS.

3) Everyone sells car insurance online now. But health, life, savings plan etc those are usually not sold online. TUNEPRO is not doing anything in trying to do that. If they did, they can cut the 6% first year, 4% second year commission and cost, giving them a huge edge. But they are not. So..

I recently re-buy some at 0.570, but very small position, mainly because its cheap.

Its not about the visionary of the management, but the economics of the business first. Unless they actually know how to run an investment fund on their own and do general insurance, i find it hard to see their edge.

2019-12-21 21:15

Dear Choivo,

Thank you. Will attend next Tunepro AGM and let them know

about your suggestion.

2019-12-21 22:31

when you copy

you do not understand

just copy blindly with no understanding

monkey see

monkey do

monkey see man slaughtering cow

monkey take baby and chop baby head off

monkey see WB buy something

monkey also buy

2019-12-21 22:37

Hmmm interesting ...

But there are so many other cheaper stocks in Bursa ...

Maybe I will consider adding a bit to my portfolio if it falls to RM8 ...

2019-12-21 23:57

True. It may very well get to that price if the QR's are matched with a financial crisis.

That would be very interesting.

2019-12-21 23:58

Lending to poor people and charge exceptionally high interest rate

This is exactly the kind of stock that you can’t lock it up for five years and throw away the keys

Not touching it even with a ten foot pole unless somebody can explain to me how they can be so good at collection and debt recovery

When something defies nature, it makes me uncomfortable

2019-12-22 01:42

these are sold online without medical checkup

////health, life, savings plan etc those are usually not sold online.///

2019-12-22 08:39

Hahahaha,

Choivo already forget about his defination on wonderful company that must seek to benefit society at large.

2019-12-22 12:13

My preference is wonderful company, but price matters, as well as my own circle of competence.

Very hard to find wonderful company at good or fair price.

Tsmc is pretty decent lah

2019-12-22 14:31

Haha Choivo,

Just pulling your leg as I appreciate your intention of explaining the previous accounting standard IFRS 139 and current IFRS 9 emphasizes shifts to the probability of future credit losses, even if no such triggering events have yet occurred thus affect the reporting of profit.

But I take offend of your sentence, “Quite interesting, does not sound like the place i want to work at (since i’m in financial reporting), but definitely sounds like the kind of company whose stock i want to purchase”

Any good company should place customers first, employees second and shareholders third because

1. With happy customers, you will get more customers and thus your business will prosper.

2. With happy employees, they will produce more and be more efficient.

3. With business continuously growing, shareholders will be rewarded with high premium of PE 25 to 50 to 100 and beyond.

I am lucky to work in a company that believes we are blissful to be in an industry that benefits all our stakeholders. It is this believes that drive us to do our best, to be the best and prepare to walk an extra mile for our customers.

Thank you

2019-12-22 18:47

Haha my petron is easily 5-6 times the size of my aeoncr position. Just bought a bit more that day, and im honestly a bit itchy to buy more.

2019-12-24 15:52

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-26 16:20:00

EMA 5

5 Mins

BUY

2024-07-26 16:00:00

EMA 5

5 Mins

SELL

2024-07-26 15:30:00

EMA 5

5 Mins

BUY

2024-07-26 11:35:00

VOLUME BREAKOUT

5 Mins

BUY

2024-07-26 10:45:00

OBV

5 Mins

SELL

Apps

Top Articles

1

2

BFM Podcast

3

MQ Market Updates

4

TA Sector Research

5

BFM Podcast

6

BFM Podcast

7

PublicInvest Research

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

hpcp

Hi Choivo, thanks for the article. What do you think of elkdesa, which has better NPL ratio and business has been growing consistently

2019-12-21 19:32