Icon8888 Gossips About Stocks

(Icon) CI Holdings (2) - Explosive Earnings Growth

CIHB released Dec 2014 quarterly report yesterday, net profit grew by a massive 168% from RM0.846 mil to RM2.269 mil.

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit before Tax ('000) | Profit ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS | |

|---|---|---|---|---|---|---|---|---|---|

| 2015-06-30 | 2014-12-31 | 110,131 | 3,548 | 2,269 | 2,269 | 1.40 | - | 0.8500 |

|

| 2015-06-30 | 2014-09-30 | 87,543 | 1,343 | 846 | 846 | 0.52 | - | 0.8400 |

|

| 2014-06-30 | 2014-06-30 | 63,511 | 273 | -421 | -698 | -0.48 | - | 0.8300 |

|

| 2014-06-30 | 2014-03-31 | 9,593 | -2,105 | -2,145 | -2,145 | -1.51 | - | 0.8000 |

|

| 2014-06-30 | 2013-12-31 | 9,200 | 129 | 65 | 65 | 0.05 | - | 0.8200 |

|

| 2014-06-30 | 2013-09-30 | 9,953 | 327 | 216 | 216 | 0.15 | - | 0.8200 |

|

| 2013-06-30 | 2013-06-30 | 10,888 | 67 | -133 | -129 | -0.09 | - | - |

|

| 2013-06-30 | 2013-03-31 | 8,909 | -31 | -53 | -53 | -0.04 | - | 0.8200 |

|

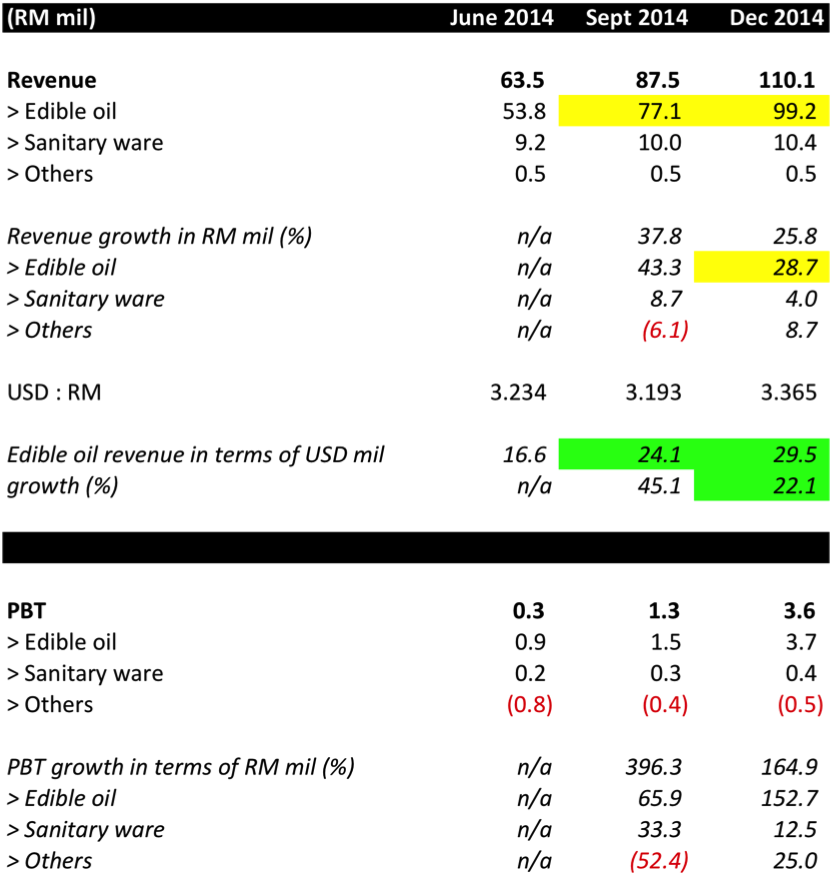

The driving force behind the growth is the edible oil packaging division. Its revenue grew by 28.7% q-o-q (from RM77.1 mil to RM99.2 mil).

However, the growth in revenue could be due to a combination of two factors :-

(a) volume growth; and

(b) weakening of RM against US dollar (every US dollar received by CIHB from oversea sales translates into more RM revenue).

In order to have a feel of the revenue growth without the effects of currency, I have divided the revenue by the average exchange rate during the relevant periods.

After making the adustments, it seemed that CIHB's edible oil packaging division grew its revenue from USD24.1 mil in September quarter to USD29.5 mil in December quarter.

The volume growth is a robust 22.1%.

Concluding Remarks

(a) After I first wrote about CIHB on 10 February 2015, I am pleasantly surprised one day later to see CIHB announced its quarterly result with robust growth in revenue and earnings.

(b) The revenue growth (and the correpsonding net profit growth) was mostly attributable to the edible oil packaging division, which sold 85% of its products overseas. Of course, the growth was aided by the stronger US dollar. However, upon closer inspection, it seemed that it is also successful in increasing its sales volume.

This is very important as the weak Ringgit will not be a permanent feature. The fact that the group is able to grow its sales volume is an indication of market acceptance of its products, which puts it in a position to further grow its business going forward.

(c) As mentioned in Part 1, CIHB's management team are experts in consumer products business. After selling off KFC stakes, they focused on distributing Pepsi Cola (through Permanis).

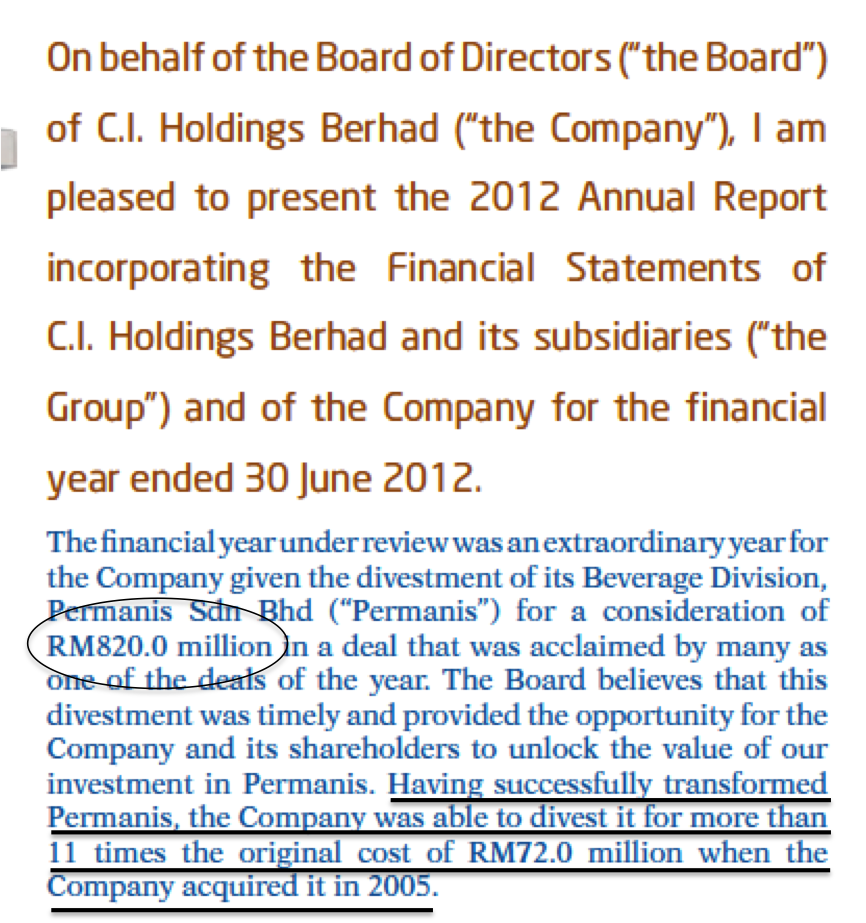

The Permanis business was initially not profitable, with only RM0.766 mil net profit in 2005. However, over the years, the management team (led by the major shareholders) successfully grew the business to report RM40 mil net profit in 2011.

They subsequently sold off Permanis to Japanese buyer for an astounding RM820 mil. They distributed the bulk of the cash back to shareholders and utilised the remaining proceeds to acquire the current edible oil packaging business.

With such profit track record and tentative signs that it now posseses a new platform that can potentially repeat the same success story, it makes sense to buy into CIHB now despite its high historical PE multiple.

====================================================

Appendix 1 - The company's track record :-

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | PE | DPS (Cent) | DY |

|---|---|---|---|---|---|---|

| TTM | 270,778 | 272 | -0.07 | - | 0.00 | - |

| 2014-06-30 | 92,257 | -2,562 | -1.76 | - | - | - |

| 2013-06-30 | 39,373 | -529 | -0.37 | - | - | - |

| 2012-06-30 | 40,842 | 658,651 | 463.84 | 0.26 | 460.00 | 383.33 |

| 2011-06-30 | 43,800 | 40,094 | 28.24 | 11.66 | 12.00 | 3.65 |

| 2010-06-30 | 516,401 | 38,528 | 27.13 | 10.03 | 11.00 | 4.04 |

| 2009-06-30 | 362,981 | 20,975 | 16.15 | 6.57 | 7.00 | 6.60 |

| 2008-06-30 | 290,451 | 14,544 | 11.22 | 9.54 | 4.00 | 3.74 |

| 2007-06-30 | 265,775 | 7,868 | 6.07 | 14.50 | - | - |

| 2006-06-30 | 222,160 | -3,764 | -2.90 | - | - | - |

| 2005-06-30 | 267,975 | 766 | 0.59 | 101.70 | - | - |

Appendix 2 - Chairman's statement as set out in FY2012 annual report :-

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-25 11:10:00

EMA 5

10 Mins

BUY

2024-11-25 11:10:00

ADX

10 Mins

BUY

2024-11-25 11:10:00

TURTLE SYSTEM 20

10 Mins

BUY

2024-11-25 11:10:00

EMA 5

5 Mins

BUY

2024-11-25 11:10:00

ADX

5 Mins

BUY

Apps

Top Articles

1

2

3

Good Articles to Share

4

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

johnny cash

TARGET PRICE ANYBODY PLEASE ???

2015-03-02 11:35