Road to Success

AWC Berhad - MYR700m 10-year’s government concession income & reinstatement of dividend payments

RicheHo

Publish date: Mon, 04 Apr 2016, 11:58 AM

AWC Berhad (“AWC”)

Background

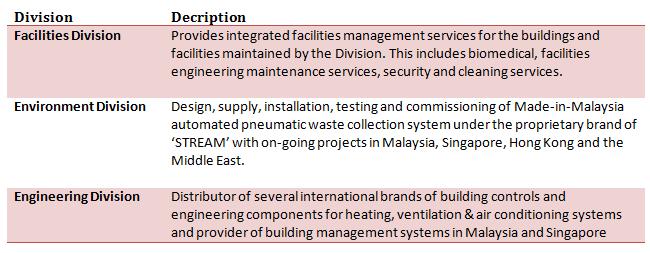

AWC is the premier provider of total asset management and provides “one stop” integrated facilities management services to building owners. The purpose is to achieve optimum operational, environmental and financial efficiencies in building management.

Its principal activities are divided into three division:

Financial Highlight

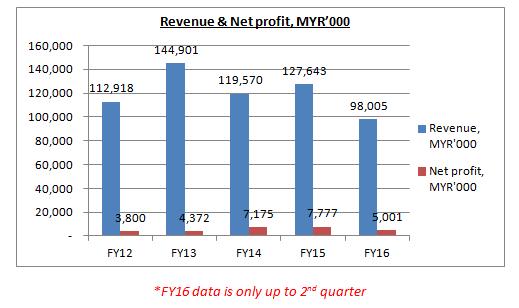

AWC revenue is mainly depending on awarded project. Its net profit had improved 3 years consecutively, from MYR3.8m in FY12 to MYR7.8m in FY15 even though its revenue doesn’t have too much difference.

However, in FY16, AWC had delivered an excellent result in first two quarters. It had achieved MYR98m revenue, which is already 76.8% of its FY15 full year revenue!

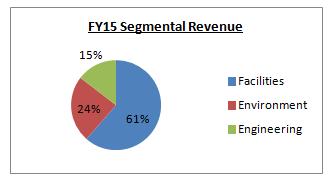

AWC FY15 revenue is mainly derived from facilities division which is up to 61%, followed by environment division 24% and engineering division 15%.

Facilities Division

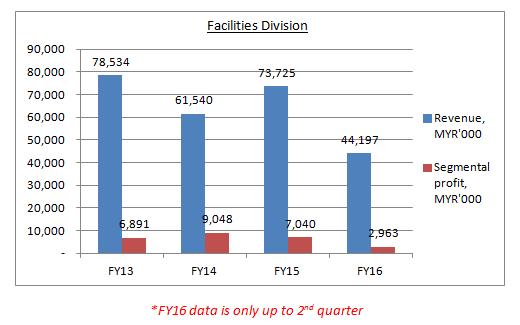

In facilities division, its revenue for FY16 had shown a significant improvement, contributed by the securing of several new contracts in the commercial segment during the year. FYI, the facilities division can be further break down into commercial and non-commercial segment.

These new contracts include Bank Negara Malaysia (from January 2015), Celcom Axiata Berhad (July 2014) and Herriot Watt University (August 2014). It will drive continues into the subsequent financial year with the commencement of other new contracts under the Commercial segment.

Under the concession segment, an interim agreement for the provision of Facility Management Services will be sign to all buildings covered under the Concession. This includes Federal Government buildings and facilities in the Southern Region (states of Negeri Sembilan, Melaka and Johor) and in the state of Sarawak under the Concession segment. This interim agreement for 3 months will be signed in continuance of the earlier interim agreement after expired. It is for the maintenance of all Federal Government buildings and facilities in respective zones.

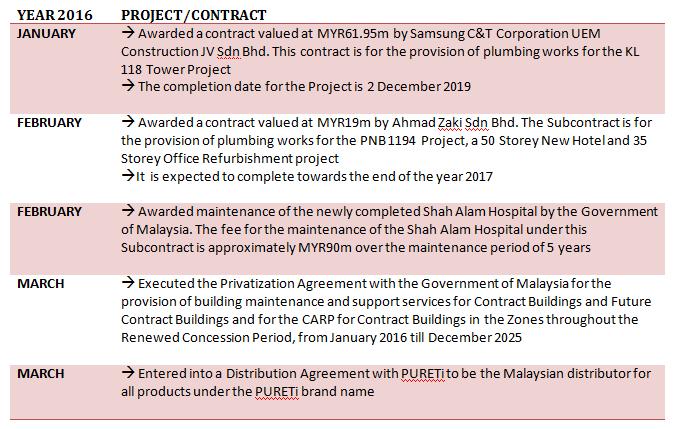

The Healthcare division relates to buildings and facilities under the Healthcare segment in the Facilities Division. In February 2016, AWC had been awarded the contract to maintain Hospital Shah Alam for a period of 5 years commencing Mar 2016 for approximately MYR90m. This new contract will contribute positively to AWC financial performance once it kicks off.

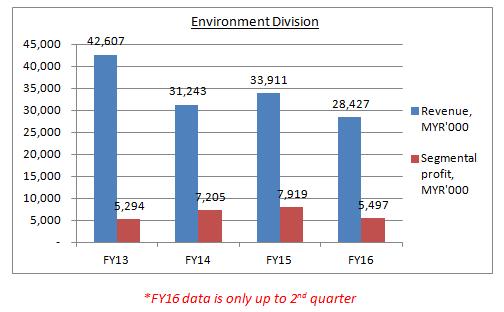

Environment Division

In environment division, AWC had delivered excellent financial result in FY16. Its revenue achieved in first two quarters was 83.8% of its FY15 full year revenue.

During FY15, AWC had completed several significant projects, as below

- The Icon Residences project for the Mah Sing Group in Kuala Lumpur

- The Puteri Harbour by UEM in Johor

- The Tropez project by Tropicana, both high end residential developments, in Johor

- Installation of Waste and Laundry Collection System in Changi General Hospital, Singapore

- Completion of Automated Waste Collection System (“AWCS”) for the H2O Residences and the Meyerise Condominium developments

In FY15, AWC had been awarded another Terminal Building for Changi Airport, for the new Terminal 4. The Housing Development Board in Singapore has also kicked off with securing the Tampines North project where AWC will install the AWCS for the entire residential complex. It is expected to contribute to AWC upcoming quarter.

In the Middle East, AWC is still in the process of carrying out work in the Al Raha Beach project for Aldar, to complete the new InPlot projects. AWC had also recently awarded with the Phase 2 works for the Infrastructure Design as well as for the installation of four AWCS modules to bring to seven, the total number of modules serving this large prestigious development.

AWC exposure into airports and supporting infrastructure continues with the award to STREAM for the implementation of the AWCS for the Cathay Pacific Catering Centre Phase 2 in Hong Kong. This project announces its presence in Hong Kong, and gives AWC a launch pad for STREAM products into China’s rapidly growing market.

Furthermore, AWC has increased its recurring income base with the securing of the Operations and Maintenance (“O&M”) for the majority of the projects that it has delivered.

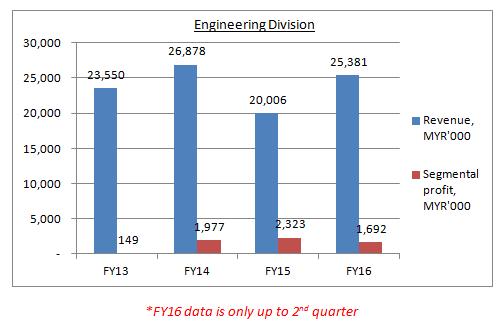

Engineering Division

In engineering division, AWC had shown a significant improvement in term of revenue and it had surpassed its FY15 full year revenue with only two quarters.

The excellent results are mainly contributed from the acquisition of QUDOTECH and DDT (will be discuss below). The results of its two new subsidiaries had consolidated into AWC result.

AWC had taken on a new air conditioning projects in FY15. Under these projects, AWC is responsible for all air conditioning works therein.

In April 2015, it undertook the Xiamen University project in Dengkil, Selangor. It also recently accepted the award of an air conditioning project for the Capital 21 project in the state of Johor, which will commence during the final quarter of the calendar year 2015. In both these projects we are responsible for all matters to do with the air conditioning systems.

Besides, in January 2016, QUDOTECH had secured the contracts for the plumbing works for the KL118 Tower and the MAS Building refurbishment and construction, for MYR61.95m and MYR19m respectively. Both of these contracts will contribute positively to the Group FY16 result.

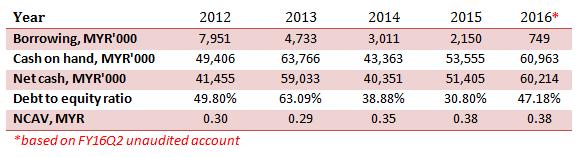

Financial Strength

AWC is a cash rich company with almost zero borrowing. Its latest net cash on hand is up to MYR60m! Even though its debt to equity ratio had increased to 47.18% in the latest quarter as compared to 30.80% in FY15, AWC is still very healthy in term of financial strength.

Its high NCAV also proof that AWC current asset is very sufficient to clear off all its liabilities.

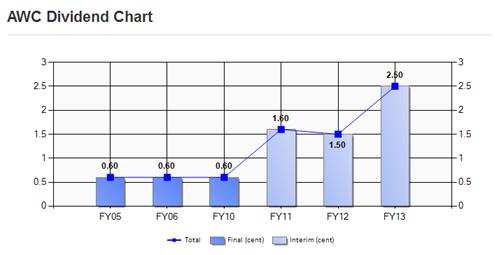

AWC had not recommended any payment of dividend in FY14 and FY15. AWC’s management had guided at the last AGM that due to the renewal of the Government Concession not being signed yet, it had temporarily held back dividends as the CAPEX requirements are unknown yet.

Currently, the concession amount had signed off by the Government at MYR700m over 10 years, it is very likely that dividend will be reinstated.

If we based on its current financial strength and contribution from its new acquired subsidiaries, AWC definitely have the ability to declare attractive dividend.

AWC currently have 256.01m outstanding shares. Let assume it is willing to declare 2.5 cent in FY16, it only needs to give out MYR6.4m. Based on its current share price MYR0.45, the dividend yield is up to 5.56%, which is very attractive.

It is possible as AWC definitely will perform better in FY16 as compared with is previous few financial years.

Acquisition of Qudotech & DD Techniche

On July 2015, AWC had proposed to acquire 100% equity interest in Qudotech Sdn Bhd (“QUDOTECH”) and DD Techniche Sdn Bhd (“DDT”).

The total consideration is MYR26.5m to be satisfied by a combination of cash amounting to MYR14.85m and issuance of 30.66m new AWC shares at an issue price of MYR0.38. The addition new AWC shares represented up to 15% of the issued and paid up share capital.

FYI, QUDOTECH is principally involved in mechanical and electrical (“M&E”) engineering works, specifically in all manners of plumbing works, while DDT is principally involved in the contracting for mechanical engineering works, the design of piping and systems for rainwater harvesting products and trading of specialized water tanks and rainwater harvesting products.

Besides, QUDOTECH had recorded a profit after tax of MYR1.72m for the financial year ended December 31, 2014 while DDT had recorded a profit after tax MYR0.45m for the financial year ended July 31, 2014.

Other than that, QUDOTECH had also secured contracts totaling approximately MYR66.1m, where the unbilled amount recognizable as revenue stands at approximately MYR44.9m. The contracts are expected to provide earnings visibility up to June 2017.

In this acquisition, there will be a profit guarantee for AWC, profit after tax of MYR7.8m in the first two financial year, with MYR3.9m each.

Current Ongoing Projects

From the business segment review, a current ongoing project list which is expected to contribute to AWC upcoming few quarters result had summarized as below. This list had excluded awarded contracts/projects in year 2016.

- Facilities

- The provision of Facility Management Services to all buildings under the Concession

- A new contract under the Healthcare segment relates to buildings and facilities

- Environment

- Installation in Terminal Building for Changi Airport, for the new Terminal 4.

- Tampines North project where AWC will install the AWCS for the entire residential complex

- Engineering

- The Al Raha Beach project for Aldar, to complete the new InPlot projects.

- Phase 2 works for the Infrastructure Design as well as for the installation of four AWCS modules, in Al Raha Beach project

- Air conditioning project for Xiamen University project in Dengkil Selangor

- Air conditioning project for the Capital 21 project in Johor

In March 2016, AWC had secured a 10-year renewal of its concession to maintain government buildings as well as a new contract for critical asset refurbishment worth a total of MYR700m!

The renewal of its concession to maintain and provide support services for relevant government buildings in Malacca, Negeri Sembilan, Johor and Sarawak is worth MYR555m.

The fee for the first five years is MYR52m per year, after which it is to be revised to MYR59m per year for the remaining five years.

For the new 10-year Carp contract, AWC will undertake the refurbishment of critical assets currently deployed in the same buildings. It will earn MYR14.5m per year on this contract, worth MYR145m over the contract period. The fees from the Carp represent a new revenue stream for AWC.

It is expected to contribute positively to the earnings of the AWC Group for the current financial year as well as over the next 10 years.

Under this new contract, AWC will have revenue of MYR66.5m every year in the first 5 years and MYR73.5m in the remaining 5 years.

Technical Chart

Based on technical analysis, AWC currently rides on its uptrend line. It had been consolidated for a month since end of February. It seems that AWC had rested enough and it is ready to continue its journey to another price region.

I anticipated that AWC will shoot up with a bull engulfing candle soon. If AWC is able to breakout from 0.47 with volume, it is expected to test 0.50 followed by 0.53.

Conclusion

In year 2016, AWC had secured few projects included KL118 Tower project, renewal of concession and become a distributor for PURETi. In addition with its previous project, AWC has a very strong book orders. The new concession is expected to contribute approximately 40% of the Group revenue and it is for a term of 10 years with stable income!

Let’s have a brief calculation on how much AWC worth after take into account of the full contribution from QUDOTECH and DDT. Assume AWC own business is able to deliver MYR8m net profit in FY16. After take into account of the profit guarantee of MYR3.9m, its net profit in FY16 is up to MYR11.9m, which equivalent to EPS of 4.65 cent (based on 256.01m number of shares).

With an estimated PE of 12, AWC is worth up to 55 cent per share. Besides, with its solid contract and current earnings power, AWC is definitely able to formulate a stable dividend policy.

Overall, AWC is expected to deliver an excellent result from FY16 onwards. Sooner, it will transform to become a strong fundamental company.

Hey guys, I am writing stock analysis report to earn some pocket money. For more information, you may email me at richeho_92@hotmail.com

For any enquiry, you may contact me as well. Sharing is caring.

Happy investing!

Cheers!

More articles on Road to Success

(RICHE HO ) Y.S.P. Southeast Asia - Boring Counter with Strong Track Record

Created by RicheHo | Mar 18, 2017

(RICHE HO) Latitude Tree Holdings Berhad - Earnings Recovery in FY17

Created by RicheHo | Feb 19, 2017

(RICHE HO) Ajiya Berhad - Green IBS Provider, Benefited from PR1MA project

Created by RicheHo | Feb 16, 2017

(RICHE HO) Benalec Holdings Berhad - Strong Earnings from Tanjung Piai & Pengerang MIP

Created by RicheHo | Jan 08, 2017

Discussions

4 people like this. Showing 15 of 15 comments

Genetec & McClean became obsolete weeks after recommendations. Now another small cap AWC. Takut eh

2016-04-04 20:07

Good analysis, though lack certain financial data. Not necessary to buy straight away. Wait for the right price to get in. I have given him a like. Keep it up Riche.

2016-04-04 21:41

pingdan, I am just writing and sharing my own study. You had the rights to comment anything, but I don't see the point of doing this. You can filter whatever I wrote and carry out your own homework. I did not ask you to buy as well, do I? :)

by the way, since when I recommend GENETEC is a good counter? please re-read the content again.

2016-04-05 09:02

haha what a shame. please learn some manners from this 24-years old young man Sir Pingdan. I like reading your analysis because u present plain facts and figures and theres nothing wrong with it. keep it up boy.

2016-04-05 11:38

Common Pingdan, dun be too harsh, can see this this junior is using his heart to write the article and he has the potential.

Remember Icon888初出道 he followed kyy and wrote alot of plantation counters?

But he nvr gave up, he continues to write write write until now become famous dy.

Richeho, gambateh

2016-04-05 14:31

Richeho: i learn from you only. I still rmb u atking me last time. Just that u show a good manners in your post. Remember this when u treat ppl bad, ppl will treat u bad

2016-04-05 18:26

I still remember u posted genetec part 1 when it reached rm0.29. What is the price now?

2016-04-05 18:27

RicheHo has my 100% support. He can count on me to subscribe for research until he is 65 years old

p/s : pingdan my friend too. Hope you guys don't quarrel.

Cheers

2016-04-05 18:33

24 years old can write so well... Thumb up. When I was 24 years old, I don't even know what is minority interest

2016-04-05 18:34

Stock: [AIRASIA]: AIRASIA BHD

Apr 1, 2016 09:01 PM | Report Abuse

Posted by Icon8888 > Apr 1, 2016 01:20 PM | Report Abuse

btw, I don't believe that Tony is forking out money to increase his shareholding to 30% (by way of placement)

no tycoon will do that in real life

tycoon like to make big money with small capital (for example : on hind sight, Gamuda issues WE because they anticipate securing huge contract soon).

Tony is not young, he will be stupid to commit so much capital at this stage of his life. If he wants to benefit from the up cycle, he would have tried to do it by warrants (for example : issue new warrants and try to swing a block to himself)

This i copy bulat, bulat icon punya comments. See!!hahzhahahahaha

2016-04-05 22:22

Hi pingdan,

1. http://klse.i3investor.com/blogs/rhinvest/87456.jsp

2. http://klse.i3investor.com/blogs/rhinvest/92036.jsp

This is both of my articles on GENETEC. I just express my point of view on this company and I never mentioned this company is good for invest.Please re-read.

By the way, I had no idea when I attack with you before. Are you sure it is me? I am sorry if there is any misunderstanding. Cheers

2016-04-06 08:48

RicheHo, to cover the "possible" declaration of dividend, it would be nice if you also cover the FCF part.

Anyway, a very good write up ~

2016-04-06 18:07

Post a Comment

Featured Posts

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

4

BFM Podcast

5

6

7

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

pingdan

Yeelee written on 25/3/2016 - RM2.18 (price before open), current RM2.17

(Loss RM0.01)

Mclean written on 28/2/2016 - RM0.20 (price before open), current RM0.16

(Loss RM0.04)

Genetec written on 26/2/2016 - RM0.165 (price before open), current RM0.135

(Loss RM0.03)

Tropicana written on 21/2/2016 - RM1.14 (price before open), current RM1.03

(Loss RM0.11)

Pentamaster written on 5/2/2016 - RM0.71 (price before open), current RM0.58

(Loss RM0.13)

Pantech written on 26/1/2016 - RM0.56 (price before open), current RM0.575

(Gain RM0.015)

History spoken. Other than pantech, all others couunters loss. Still follow him for "road to success" or "road to holland"? See historical record then you will know either he is good or not

2016-04-04 13:28