Wealth Creation

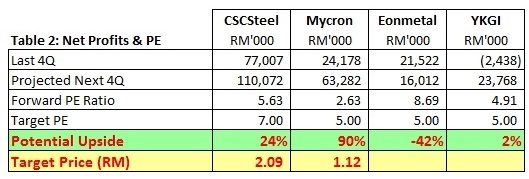

Huge Potential Upside for CRC Steel Producers: CSCSteel (+24%) & Mycron (+90%) (Part 2)

WealthWizard

Publish date: Tue, 06 Sep 2016, 09:33 AM

WealthWizard

0 9

All the working, calculation & assumptions are presented based on my personal own judgement & findings, and are for sharing purposes only.

I never think I can move anything unless the thing want to move by itself.

Do your homework, read all news/reports, make your best judged assumptions & understand the business before invest any company.

Invest with FREE money only, using emergency fund to invest is gambling, crazy & suicide act.

My email: wealthwizard.invest@gmail.com

I never think I can move anything unless the thing want to move by itself.

Do your homework, read all news/reports, make your best judged assumptions & understand the business before invest any company.

Invest with FREE money only, using emergency fund to invest is gambling, crazy & suicide act.

My email: wealthwizard.invest@gmail.com

Part 1: Bright Future for CRC Steel Producers: CSCSteel, Mycron, Eonmetal & YKGI

Part 2: Huge Potential Upside for CRC Steel Producers: CSCSteel (+24%) & Mycron (+90%)

Part 3: Flying CRC Steel Producers: Fantastic Business Outlook & Insider's Look

This article focus on the comparison among 4 major CRC Producers in Malaysia purely based their financial results & cash flows performance.

The 4 CRC producers' yearly production capacity:

1. CSC Steel Bhd (620,000 tonnes)

2. Mycron Steel Bhd (260,000 Tonnes)

3. YKGI Bhd (220,000 Tonnes)

4. EonMetal Group Bhd (120,000 tonnes)

4. EonMetal Group Bhd (120,000 tonnes)

And the utilisation of the capacity are as follows:

1. CSC Steel Bhd (64.5%)

2. Mycron Steel Bhd (78.1%)

3. YKGI Bhd (54.5%)

4. EonMetal Group Bhd (20.8%)

4. EonMetal Group Bhd (20.8%)

To know respective CRC companies' utilisation of the production capacity, please read page 7 of the following report: http://cdn1.i3investor.com/my/files/dfgs88n/2015/11/06/1483789631--639706738.pdf

MYCRON IS CLEARLY UNDERVALUED, EVEN AT THIS PRICE!!!

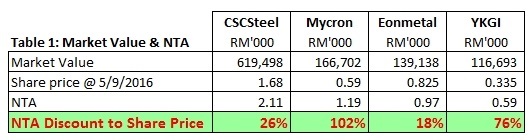

Mycron's share price is having huge discount to NTA among all CRC producers:

Mycron's forward PE is the lowest among all CRC producers:

Important Notes:

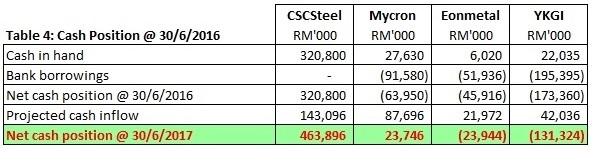

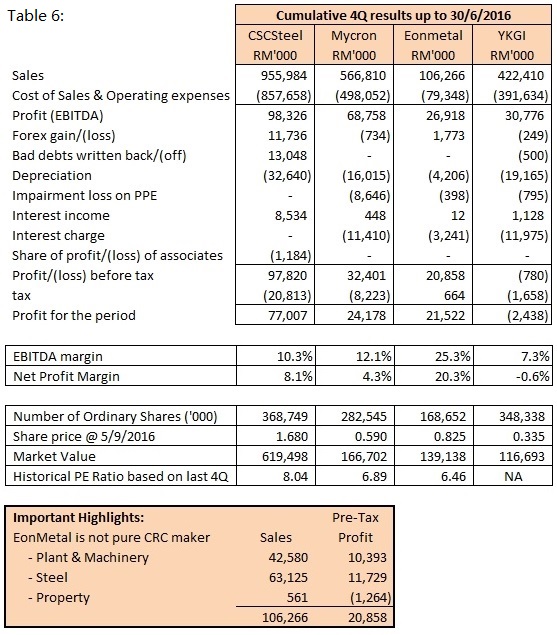

CSCSteel is the largest CRC producer in Malaysia, having strong balance sheet with huge cash in hand amounted to RM320.8m (refer to Table 4) and consistent high dividend yields & payout for the past 10 years. It's like Public Bank in bank sector.

EonMetal is not pure CRC producer and it involves in manufacturing of plant & machinery where it command huge profit margin, so the PE should not just compared purely that way.

Mycron is having the highest Cash Flow to Market Value ratio among all producers:

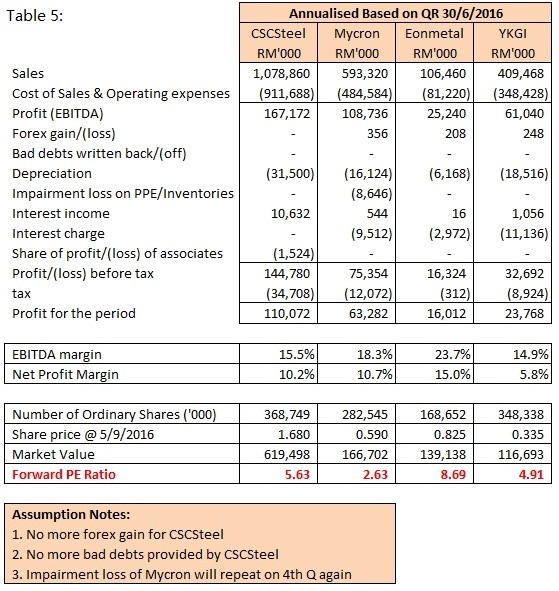

Table 5 illustrate the projection of next 12 months financial performance of 4 companies:

Table 6 illustrate the cumulative last 4 quarters financial performance of the 4 CRC companies:

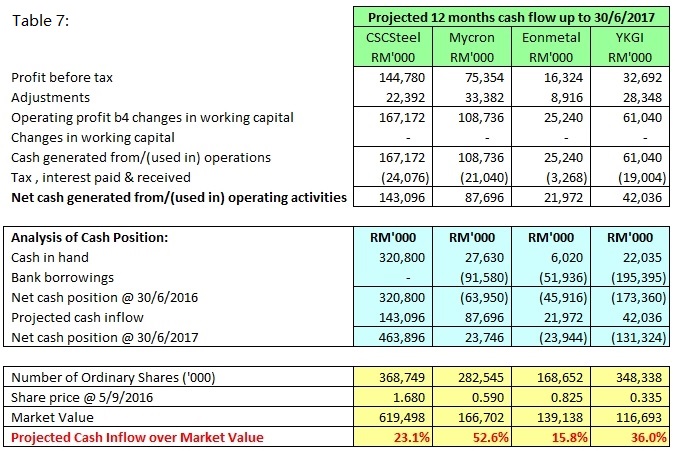

Based on the projected financial performance illustrated in Table 6, the cash flows of the respective companies are illustrusted in the Table 7, with the assumption that there will have no changes in working capital:

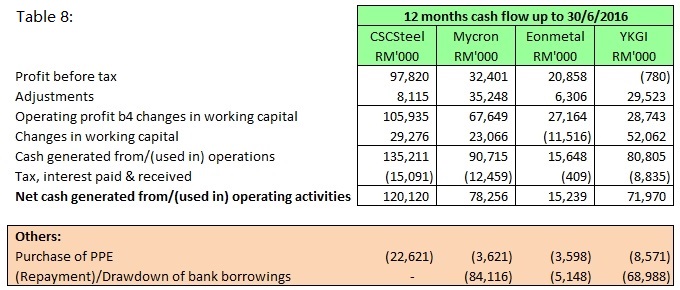

The following are cash flows statements based on last 4 quarters of the respective companies:

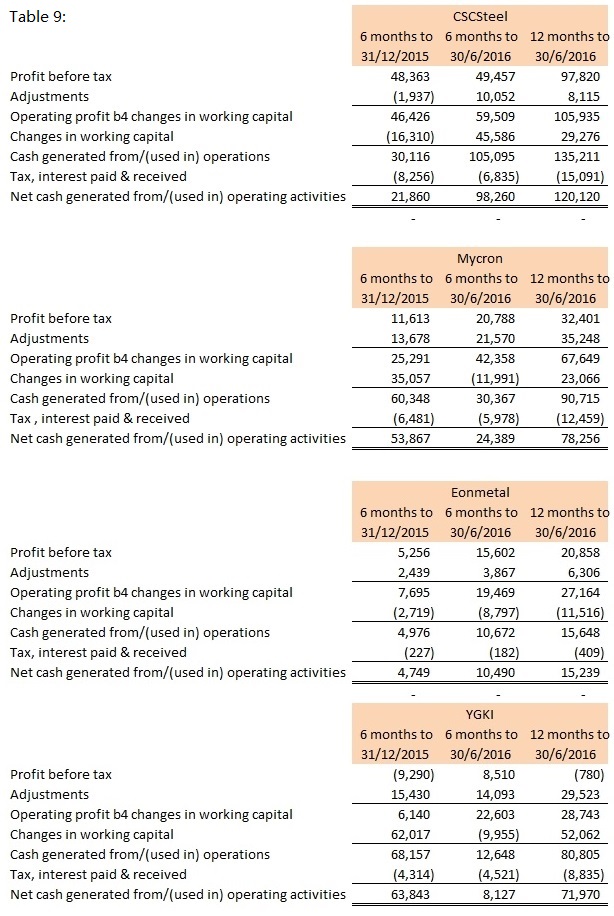

Table 9 are the workings in getting the last 4 quarters cash flows details of the respective companies:

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Wealth Creation

CAB CAKARAN: Achievable Target price = RM3.09? (Part 3) (WealthWizard)

Created by WealthWizard | Apr 06, 2017

CAB CAKARAN: Something Big Is Coming in Poultry Industry (Part 2) (WealthWizard)

Created by WealthWizard | Mar 27, 2017

CAB CAKARAN: Malaysia Broiler/Chicken Giant in Making (Part 1) (WealthWizard)

Created by WealthWizard | Mar 21, 2017

EKOVEST: The Next Big Thing & Great Upside Potential (+84%) (Part 3).

Created by WealthWizard | Oct 07, 2016

EKOVEST: Net Debt Ratio=20% & Net Cash Per Shares=RM1.01 (after 40% sale in Kesturi) (Part 2)

Created by WealthWizard | Sep 26, 2016

EKOVEST: Doing Great & Ready To Shine, Are You Ready? (Part 1)

Created by WealthWizard | Sep 23, 2016

Flying CRC Steel Producers: Fantastic Business Outlook & Insider's Look (Part 3)

Created by WealthWizard | Sep 12, 2016

Bright Future for CRC Steel Producers: CSCSteel, Mycron, Eonmetal & YKGI (Part 1)

Created by WealthWizard | Sep 05, 2016

Discussions

13 people like this. Showing 50 of 70 comments

Found this in their annual report:

The principal activities of the Group consist of manufacturing and trading of ductile iron pipes, steel and plastic pipes and fittings and waterworks related products, construction work and project management for waterworks and sewerage industry.

2016-09-07 15:18

This steel stock got potential as i got one good target price infor about this stock but i dare not enter due to it still in loss financial?

2016-09-07 15:25

from what I understand, steel price has tracked china sudden surge in demand, which is then followed by iron ore prices increase (the raw material). so would it be correct to assume that local steel producers are benefiting from higher selling prices due to increase in global steel price and enforcement of anti-dumping, while raw material cost didn't increase as much mainly because they don't need to source from megasteel anymore? or is it also possible that the recent quarter results increase in margin is because the steel players are drawing down from old inventories (purchased at last year's price, cheaper than now even if it's was from megasteel) while steel price (selling price) has increased? so the timing mismatch resulted in higher margins? and if steel price (selling price) correct down together with iron ore (raw material price), do you think local steel producers can maintain their current margins? sorry for a lot of questions, just hoping to get a better understanding of the industry dynamics since you seem to have done quite some homework. thanks

2016-09-07 15:34

It's ok, Jay, we are discussing to learn more from each others.

I will advise you to read annual reports & quarterly reports of CSCSteel & Mycron for the past 2 years, those questions were actually answered.

Chairman's statement of Mycron is the best so far if compared to others.

http://cdn1.i3investor.com/my/files/dfgs88n/2015/11/06/1483789631--639706738.pdf

2016-09-07 15:56

I have read the Mycron annual report and some other quarterly commentaries. basically most quarterly statements summarise the better performance due to better selling price and lower costs (more or less) without giving the underlying factors (except Mycron AR). that's why I wanted to confirm my 1st question based on what I understand from wealthwizard's articles.

for the 2nd question, I can't find any confirmation except from observing the HRC/CRC/steel rebar/iron ore prices. it's my speculation. if it's true, then the better margins in 2Q could last shorter than expected.

3rd question actually is a bit tricky. probably even the companies also can't have an exact answer on how they could cope with prices fluctuations but I just wanted to see what everyone thinks about it.

2016-09-07 16:16

Thanks, moneySIFU & Jay, for having good discussion over here.

I am working on Part 3 article which will dig deep into Mycron accounts, from there we may have better & true picture about CRC & HRC industry. Hope to have it completed by tomorrow.

2016-09-07 16:24

Wealthwizard, could you share the supply chain of steel? From hrc to crc to??? Who are the big buyers for cscsteel? Are they in construction segment? Tq in advance :)

2016-09-07 20:40

Hi probability, this article hit No.1 for one or 2 hours, then down to no.2 most of today.

2016-09-07 23:35

Feel great already for articles being seen by so many investors & readers. :)

2016-09-07 23:49

Hi chl1989, I can only analyze based on annual reports from those CRC companies and try to figure out the true pictures from those accounts.

Most of my findings are based on CSCSteel & Mycron, these 2 are very generous in sharing the info & details of their businesses, especially Mycron.

For Eonmetal, nothing much thing can be digged out because they are giving too little info from their reports.

See what the eonmetal management explained on increase in profits:

"This segment recorded PBT of RM0.6 million, a rise of RM1.3 million is in line with the increase in revenue." - Plant & Machinery Division

"This segment recorded PBT of RM3.8 million due to lower production costs" - Steel Division

YKGI was up & down, also not much things to be digged out.

2016-09-08 00:02

There is priority issue need to be set for respective stocks, I think Mycron should go first since there was misunderstanding by many in reading their latest QR.

2016-09-08 00:05

Also, being conservative is always good, just let the market to decide what's best should be

2016-09-08 00:06

I will try to email their IR. See if i can find out what is the biggest end-use industry which their products going into :)

2016-09-08 00:40

At price of RM0.785, the Forward PE = 3.5

The market value of Mycron is RM221.8m

Projected next year's profit = RM63.3m

Projected next year's cash inflow = RM87.7m

2016-09-10 09:26

Hi moneySIFU, WealthWizard,

May I know how Mycron "Projected Next 4Q" profit RM63,282,000 being calculated? As normal calculation, it will take latest quarter profit 9,336,000*4=37,344,000. Can you show me how to get accurate value RM63,282,000? Just wish to learn from you. Thank you.

2016-09-11 13:20

Hi LouisLim, the impairment loss may only occur in the 4th Q of the company, after receiving the valuation report done by the professional valuer, C H Williams Talhar & Wong Sdn Bhd.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5190321

Impairment loss for 2015 was RM3.46m & 2014 was RM6.35m

2016-09-11 14:02

So, when calculating Q1 to Q3 result, you need to take out impairment loss. That's how figures in the Table 5 derived.

2016-09-11 14:04

@Wealthwizard

Thanks for the sharing!

Could you please enlighten me about your estimated value in table 7(projected 12 months cash flow)?

1) Adjustments

2) Tax, interest paid and received

Appreciate your input on the above. Thank you.

2016-09-12 04:07

Flying CRC Steel Producers: Fantastic Business Outlook & Insider's Look (Part 3)

http://klse.i3investor.com/blogs/wealth123/104163.jsp

2016-09-12 16:45

It will be great if any weaknesses, incorrect calculation or basis can be pointed out for discussion rather than giving a general opinion or telling where price should go.

2016-09-12 22:24

By reviewing the figures again, it gives me confidence to continue hold, thank you for the sharing of such great works, it is fantastic!

2016-09-13 18:45

See something before many others see, know deeper before many others aware, look further when many others still look here & there, you will earn more than many others.

Try to look up to everyone that talk positive & negative, judge yourself, don't blame anyone if you don't get it.

Opportunities are always for those who are ready AND have ability to grab it.

2016-09-17 13:42

lets not forget to remind ourself the real numbers above.

it was not plucked from the sky.

2016-09-20 14:39

My new article, enjoy reading:

EKOVEST: Doing Great & Ready To Shine, Are You Ready? (Part 1)

http://klse.i3investor.com/blogs/wealth123/104926.jsp

2016-09-23 11:37

China CRC price was RMB3,480 when my first article was published on 5/9/2016, now it is recorded as RMB3,597, an increase of 3.4%.

Bright Future for CRC Steel Producers: CSCSteel, Mycron, Eonmetal & YKGI (Part 1)

Author: WealthWizard | Publish date: Mon, 5 Sep 2016, 11:02 AM

http://klse.i3investor.com/blogs/wealth123/103741.jsp

2016-10-17 16:07

I retain my target price for Mycron at RM1.12, subject to revision to higher due to increase in China CRC price & weakening RM against China Yuan

2016-10-17 16:13

only reason it failed to show spectacular earnings as WW had projected was due to USD->RM exchange and the speed the raw material price rise was way too faster than the local market could accept the CRC products rise...

But now its a completely different scenario now.

2017-05-11 23:15

The company that made the rusting steel industry shine like silver now...Mycron

2017-05-12 13:50

YKGI gross profit risen from 8.7% to 15.6%.

7% difference.

just add 7% margin on 180 Million revenue of Mycron.

2017-05-12 14:07

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

save malaysia!

3

4

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

5

Good Articles to Share

6

Good Articles to Share

7

Good Articles to Share

North Korea vows 'total destruction' of enemy on Korean War anniversary

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

i4investor

How about YLI?

2016-09-07 15:11