M+ Online Research Articles

Market Chat - 3Q23 Outlook & Strategy - Stay defensive under the challenging environment

MalaccaSecurities

Publish date: Tue, 04 Jul 2023, 09:23 AM

MalaccaSecurities

0 3,599

An official blog in I3investor to publish research reports provided by Malacca Securities research team.

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

All materials published here are prepared by Malacca Securities. For latest offers on Malacca Securities trading products and news, please refer to: https://www.mplusonline.com.my

Malacca Securities Sdn Bhd

Hotline: 1300 22 1233 / 06-336 5178 (office hours: 8.30am - 5.30pm)

Tel : +606 - 337 1533 (General)

Fax : +606 - 337 1577

Email: support@mplusonline.com.my

- We think the short term concerns such as the banking crisis, inflationary pressure and elevated interest rate environment are priced in, thus the downside could be limited over the near term in the global markets.

- Domestic front, we believe growth is still resilient, coupled with China’s recovery theme play under manageable inflation environment. However, the 6 states elections outcome may provide increased volatility in the markets.

- We favour stocks with defensive nature such as high net cash, growing earnings and solid dividend yield for 3Q23.

- For this setup, we favour selected stocks under these sectors, namely the (i) Construction, (ii) Building Material, (iii) Utilities, (iv) Property, (v) O&G and (vi) Consumer, and (vii) Finance.

Global catalysts

- Banking crisis in the US and Europe. Potentially, we have averted further crisis in the banking sector after efforts from the Fed and the US Treasury. However, we may revisit this issue down the road as the Bank Term Funding Program is a 1-year program and the media may be covering this by March 2024.

- Inflation is normalising… The elevated inflationary pressure remains a concern for the Fed, while the ultimate inflation target is 2% (May-23: 4.1%). The CPI, in our view, is on a declining path and likely heading towards the target of 2%.

- …but the Fed’s narrative is still hawkish. However, the narrative remains hawkish and hinting at 2 more rate hikes in 2H2023. We think these 2 rounds of rate hike have been priced in and the market is speculating the rate cut to come in by 2024.

- Recession fear still persists. According to Bloomberg consensus, the recession probability remains at 65% as of Jun-23 as compared to 10% in 3QCY21.

- Inverted yield curve. We understand that the US2Y-US10Y spread has been in the negative territory for the past 1 year; likely the US economy may dip into a recession in the next 1-2 years (based on previous statistics).

- China reopened early this year. Since Jan-2023, China has reopened its business activities and its country borders for international tourists, which we believe may translate to higher tourist receipts following a higher number of travellers.

- Emergence of Artificial Intelligence theme. Since early this year, the lookout for AI generated content has surged and it may contribute to stronger demand for AI chips, where it will benefit especially Nvidia, while other related chipmakers and AIrelated stocks may benefit. We think it will contribute to resilient demand for the whole technology value chain from memory, storage, hardware, software, high-end CPU chips and network infrastructure in the near to mid-term.

Malaysia catalysts

- Still growing in economic activities. With the business environment returning to normalcy, Malaysia’s GDP grew at 8.7% in 2022 and we expect the GDP will continue to expand at a 4-5% rate in 2023 premised on the reopening of China borders since January. Also, we believe the pent-up demand in the local services and consumer spending which will be able to support the above mentioned growth.

- International tourists are growing. Since Apr-22, international arrivals are increasing, almost back to the pre-Covid level around 1.8-2.0m per month. Hence, with the reopening of China borders starting 2023, it is likely to boost the overall tourists’ arrival in 2023. Besides, healthcare tourism is expecting a surge following Covid-19 pandemic and could see stronger numbers for hospitals as well.

Economic review and outlook

- Based on Bloomberg consensus, the World GDP is likely to grow at a gradual pace of 2.6-3.3% over 2023-2025. Meanwhile, the US is expected to advance by 0.7-1.9% over 2023-2025.

- Brent oil price maintained above USD72. Consensus is expecting the market to tighten in the second half, the oil price may maintain above USD72 with the anticipation of supply cuts by OPEC+ for July. However, if the Fed’s tone continues to stay hawkish, it may slow the economic growth, thus reducing oil demand.

- Dollar index still supported above 101-102. Despite the decline in CPI data, the Fed remains hawkish for the near term as Jerome Powell mentioned another 2 rounds of hike in 2H2023 that should provide support for DXY above 101-102 in the near term.

Market performances and review

- MSCI World and S&P500 are fairly valued, trading at the PE multiples of 18.8x and 21.3x vs. 10Y avg PE of 19.2x and 20.4x, respectively.

- The FBM KLCI is trading at a discount of 15.0x PE vs. the 10Y avg PE of 17.5x.

- Trading activities are slowing down. In 2Q23, we observed that the YTD ADTV has declined to RM1.78bn vs. RM2.14bn in 1Q23. Meanwhile, foreign funds are net sellers, valued at –RM4.2bn for on the YTD basis.

- More incline to the downside. In 2Q23, 3 of the major indices, namely the FBM KLCI, FBM Small Cap and FBM ACE were down by 3.2%, 2.7% and 3.1%, respectively. Sectoral wise, Industrial products (-8.3%), Energy (-7.5%) and Healthcare (-6.2%) were amongst the losing sectors, while the Utilities (+8.1%), Construction (+1.4%) and Transportation (+0.8%) gained momentum for 2Q23.

3Q23 Strategy

- Fluid political environment… After the GE15, currently we are heading into the state elections that will be held within the next 60 days. We believe it may dampen the sentiment on the local front, while the upside of the FBM KLCI may be capped for the near term.

- …but may flourish after the state elections. In Mar-23, Malaysia and China may have signed several MOUs valued at RM170bn investments to enhance trade and economic cooperation. Besides, we believe more construction projects could emerge as things stabilised after the state elections.

- Benefit the building material segment. Higher development expenditure in the Budget 2023, potential RM170bn investments from China and rolling out of construction projects going forward could benefit the construction sector. In the meantime, building materials companies such as the metal and cement sectors should benefit under these scenarios.

- Year of the AI and renewables. Under our Budget 2023, we believe the developments within solar and EVs to emerge as the government focuses on green initiatives. Also, we opine that higher automation, AI content and digital technology will benefit these sectors such as semiconductor, automotive and solar related.

- Cash will be an important factor. We anticipate that the high interest rate environment will be a norm in the future, and we think investors should opt for companies with high net cash, low gearing or stable dividend track record to weather through the challenging environment.

ADVCON – Slow and Steady

- Leading construction company with more than 25 years of experience in civil engineering and infrastructure works and has since diversified into quarry operations and solar renewable energy.

- Outstanding orderbook of approximately RM525.8m, which represents an orderbook-to-cover ratio of 1.3x against FY22 revenue of RM422.4m to provide sustained revenue visibility over the next 18 months.

- Leveraging on higher Budget allocation in Sarawak as approximately 20.0% of ADVCON’s existing orderbook comprises of Sarawak-related projects.

CARIMIN – Tagging the steady oil price

- Completed projects valued more than RM1.00bn since its inception for notable portfolio of clients include oil & gas giants such as PETRONAS Carigali, Shell, Murphy Oil, Repsol, Exxon Mobil, New Field, Petrofac, HESS and Nippon Oil.

- To adopt a lower-carbon future by exploring new technologies and renewable energy opportunities that may include new businesses beyond their oil and gas portfolio.

- Crude oil prices have been stable in recent months and OPEC & allies to curb production may continue to support prices.

ECOWLD – Property recovery to be seen

- ECOWLD operates as a real estate development company. The Company develops townships, integrated commercial properties, high-rise apartments, and business parks. Eco World Development Group serves clients worldwide.

- Sales target of RM3.5bn in FY23. Likely to achieve as ECOWLD has booked RM2.4bn in property sales for the 7MFY23. Meanwhile, unbilled sales stood at RM4.23bn (~1.5x of revenue).

- Growing net profit and attractive dividend yield. We believe the earnings visibility and growth will be seen going forward, while the prospective dividend yield is at 6%.

MCEMENT – Bearing fruits in the building material segment

- Largest cement manufacturing company in Malaysia with a total production capacity stood at 25.1m MT, making up to approximately 65.0% of market share in Malaysia’s cement production capacity.

- Leverage on the reactivation of the National Affordable Housing Council to coordinate the construction of 500k affordable homes under the 12MP by 2025.

- Higher cement prices bode well whereby the average price of cement (ordinary Portland) rose 1.4% MoM to RM22.81/50kg in May 2023.

OSK – Mini conglomerate with steady growing business

- Well diversified mini conglomerate with 5 core business in the financial services, property development, construction, industries and hospitality business.

- Property development segment to anchor growth from unbilled sales of approximately RM1.02bn as at end-1Q23 will sustain earnings visibility over the next 18-24 months.

- Loan portfolio stood at RM1.32bn with minimal non-performing loan ratio and backed by adequate security cover.

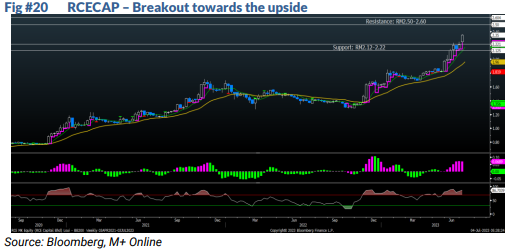

RCECAP – Solid prospects in the financing space

- RCECAP is engaged in provisioning of personal financing to government employees in Malaysia through its wholly owned subsidiary RCE Marketing Sdn Bhd.

- Increasing dividend payout. In tandem with its recent result, RCECAP will adopt a new dividend policy that will payout 60-80% of its consolidated PAT from 31-Mar2024 as compared to 20-40% in the past; this may translate to ~7% prospective DY.

- Despite the cost of funds in the upward trend, it managed to pass this through via higher profit rates for new loans; should the government servants get the salary increments and adjustments, it should bode well for RCECAP.

SCICOM – Domestic and global BPO player

- SCICOM is primarily involved in the business process outsourcing (BPO) industry and integrated digital solutions, which serves MNCs globally. It offers innovative digital services in the areas of customer lifecycle management, digital, and govtech.

- Decent track record of dividends. It has been rewarding shareholders over the past 10 years with a 10Y dividend CAGR of 12.3%, while prospective DY is at 6.2%.

- Solid balance sheet. SCICOM has a healthy balance sheet with a net cash position of RM43.8m or RM0.12 net cash per share as at 2QFY23.

SFPTECH – Automated equipment solution provider

- One-stop automated equipment solution provider that offers conceptualising, designing, assembling, and commissioning of automated equipment and production line systems for factory manufacturing lines.

- To expand production capacity through the construction of Plant 3 and addition of 41 new numerical control milling machines and over the next 3 years.

- Undertaking 2-for-1 bonus issue exercise to reward existing shareholders for their loyalty and continuous support and improve trading liquidity.

TEOSENG – Normalising cost may boost earnings

- TEOSENG is principally involved in poultry farming. Also, it is involved in the manufacture and marketing of paper egg trays and animal feeds, along with the distribution of animal health products.

- Strong growth in earnings over the past 2 quarters. TEOSENG’s earnings have been growing to RM19.7m in 1Q23 vs RM13m in 4Q22 on the back of higher egg prices, decent demand as well as normalising feed costs.

- Rationalisation of subsidies. Going forward, we expect the government aims to lift price controls for chicken and eggs, which is part of the subsidies rationalisation programme; thus it may lift the earnings for poultry stocks.

UCHITEC – Well executed company

- UCHITEC designs, researches, develops, and manufactures miniature data terminals, fuzzy logic controllers, and control modules. Besides, it assembles electrical components onto printed circuit boards and trades complete electric modules and saturated paper of PCB lamination.

- Prospective dividend yield of 5.5%. Over the years, UCHITEC managed to pay out decent dividends of 10 sen p.a. to currently 30 sen p.a; 10Y CAGR of 11.6%.

- Solid ratios. Past 5 years, UCHITEC’s average net income margin and ROIC stood at 48.9% and 33.0%, respectively, while the net cash on hand stands at 47.2 sen.

WASCO – O&G infrastructure player

- WASCO operates as an energy infrastructure company, specializing in pipe coating and corrosion protection services, fabrication and rental of gas compressors and process equipment, servicing the international O&G sector.

- Orderbook of RM3.5bn and tenderbook of RM5bn. Mainly, WASCO’s order book concentrates on projects from gas and renewable, while its RM5bn tenderbook involves its pipe coating and engineering segments, which may be awarded in 2H23.

- WASCO plans to divest its non-core assets to streamline its operations and focus on the energy segment, which will lead to improvement in overall performance.

WCEHB – Beginning of a new journey for WCE

- Involved in the construction of Malaysia’s 3rd longest expressway in Peninsular Malaysia; namely West Coast Expressway (WCE) that costs approximately RM5.04bn and spans across 233km which is expected to see full completion by end 2024 or early 2025.

- Completion of WCE may boost long term recurring income and subsequently ease cash crunch from toll collection and is supported by the expectations of additions of 650,000 new units of total industry volume in 2023.

- Disposal of entire 40.0% equity interest in Radiant Pillar Sdn Bhd (RPSB) to IJM Properties Sdn Bhd, for RM494.0m cash to give rise to pro forma gain of RM245.7m may free up cash flow and reduce the cost of interest expenses in the concession segment.

YTLPOWR – Defensive under elevated inflation environment

- YTLPOWR is engaged in providing power generation, electricity transmission, water supply, and communications services.

- PowerSeraya to be the main focus over the next 2-3 years given no new supply of power plants in Singapore for next 3 years and low fuel cost structure.

- YTL Green Data Center Park in Johor is completing in 1QCY24. The group sees this as a new revenue source given the strong demand of tech companies from China to set up their server in Southeast Asia.

Source: Mplus Research - 4 Jul 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-08-25

YTLPOWR2024-08-24

OSK2024-08-24

UCHITEC2024-08-24

WCEHB2024-08-23

TEOSENG2024-08-23

UCHITEC2024-08-23

WASCO2024-08-23

WASCO2024-08-22

CARIMIN2024-08-22

MCEMENT2024-08-22

MCEMENT2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-22

YTLPOWR2024-08-21

MCEMENT2024-08-21

OSK2024-08-21

YTLPOWR2024-08-21

YTLPOWR2024-08-20

TEOSENG2024-08-20

TEOSENG2024-08-20

WASCO2024-08-20

WASCO2024-08-20

YTLPOWR2024-08-19

RCECAP2024-08-19

SFPTECH2024-08-19

SFPTECH2024-08-19

SFPTECH2024-08-17

RCECAP2024-08-16

RCECAP2024-08-16

SFPTECH2024-08-16

WASCO2024-08-16

WASCO2024-08-16

WASCO2024-08-16

WASCO2024-08-15

YTLPOWR2024-08-14

YTLPOWRMore articles on M+ Online Research Articles

OSK Holdings Bhd - Firing Up In All The Business Segments

Created by MalaccaSecurities | Aug 21, 2024

99 Holdings Berhad (99SMART) - Amplifying The “Near n’ Save” Concept

Created by MalaccaSecurities | Aug 19, 2024

Featured Posts

Latest Videos

.png)

Apps

Top Articles

1

Mercury Securities Research

2

save malaysia!

3

4

The Alpha Trader

7

8

THE INVESTMENT APPROACH OF CALVIN TAN

JCY (5161) Posted a 2nd Qtr of Good Profits: Showing a Clear Sign of A Turnaround, Calvin Tan

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....