Choivo Capital

(CHOIVO CAPITAL) Demystifying the under-performance of the KLSE versus other markets (NASDAQ, S&P, SGX, NIKKEI etc)

Choivo Capital

Publish date: Sun, 21 Jan 2018, 04:53 AM

I still remember quite clearly a month or 2 ago. When Ooi Teik Bee said in a post to I3, that he was very disappointed in the low stock market performance in the KLSE, despite being one of the markets that received the most foreign inflows.

Back then, his fantastic 70% return for 2017, dropped to a slightly less fantastic 50%.

We also had so many post in I3 by members saying that they have given up on the KLSE, and that it’s the worst market in the world etc.

I had an idea of why the KLSE was rising so slowly, and I decided to study it and flesh out my thinking properly. This post is the essence of my current understanding.

If you want the short answer.

It is due to comparatively higher interest rates. Malaysia still have very logical interest rates in contrast to the rest of the world which have gone mad with low to negative interest rates.

Let’s see what everyone's favourite investor to quote, Warren Buffet, says,

“Interest rates act on financial valuations the way gravity acts on matter: The higher the rate, the greater the downward pull. That's because the rates of return that investors need from any kind of investment are directly tied to the risk-free rate that they can earn from government securities. So if the government rate rises, the prices of all other investments must adjust downward, to a level that brings their expected rates of return into line. Conversely, if government interest rates fall, the move pushes the prices of all other investments upward.”

Now, let’s begin with the detailed analysis.

2008 to 2017

An overview.

We all know what happened in 2008. The most severe financial crisis since the great depression happened. Some would argue that it is actually worse than that. Except unlike the great depression which took 20 years to recover. This one took less than 2 years.

What happened?

Well, it was at that moment, that every single major central bank in the world opened the reserves and started printing money in order to bail everyone out.

The big 4, European Central Bank (ECB), Bank of Japan (BOJ), Federal Reserve (FR) and the Bank of China (BOC) well and truly opened the taps.

They first purchased the toxic assets and illiquid assets from the banks and insurance companies in order to save them. Effectively giving the banks free money to loan out more and kick-start the economy again.

Then, the governments in the Big 4 (US, Japan, China, Europe), started issuing bonds like crazy, with the central banks in the world buying them up by the tens of billions every week.

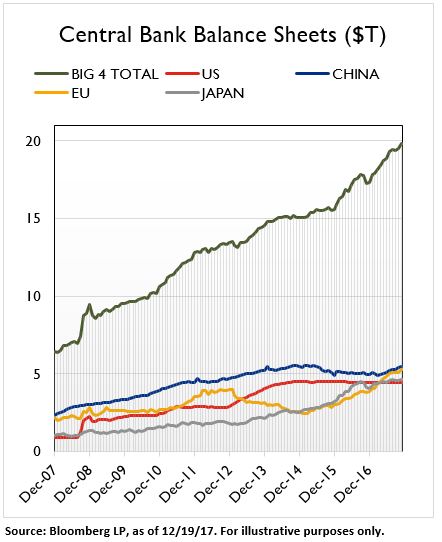

All in all, the central banks of the Big 4 bought USD 13 trillion worth of bonds and other assets in less than 10 years using printed money.

They also lowered interest rates to record lows. With Japan and Europe having the ignominy of being the first to charge negative interest rates.

What does negative interest rate mean? It means, that if you keep money in the bank or buy bonds from the government, they will actually charge you money!! Not kidding.

The Effects

What this resulted, is that the pricing of risk is now completely wrong in these markets.

As Bill Gross and Howard Marks would say, extremely low to negative interest rates are a threat to the very fabric of capitalism itself.

As we said earlier, in the years from end of 2007 to 2017, quantitative easing by the central banks of the Big 4 added USD 13 trillion to their already bloated balance sheets. Ending up with a total USD 20 trillion and rising.

The thing about central bank balance sheets is that they are supposed to rise in tandem or slightly slower than the growth in the economy.

Instead, it tripled in just 10 years. I doubt the world economy have tripled in size from the highs of 2007.

This resulted in a complete mispricing of investment, whether in terms of quality or risk.

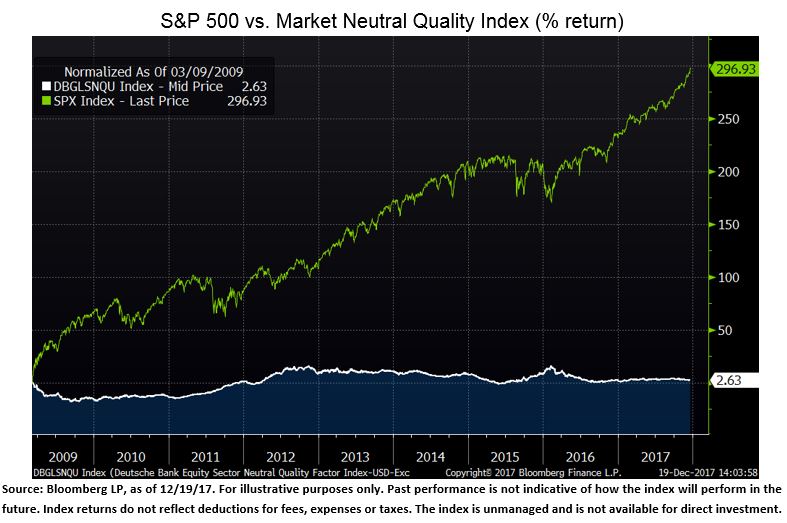

Looking at the picture above, The green line shown in the picture above is the S&P 500 index, and, the white line below is a “Quality Index” sponsored by Deutsche Bank.

What is the "Quality Index"

They take the 1,000 global large cap companies and evaluate them for return on equity, return on invested capital, and accounting accruals, and other quantifiable proxies for the most common ways that investors think about quality (Because the goal is to isolate out the investments with quality).

This “Quality index” is long in equal amounts the top 20% of measured companies and it shorts the bottom 20% (so market neutral), and has equal amounts invested long and short in the component sectors of the market (so sector neutral).

The chart begins on March 9, 2009, when the US Federal Reserve launched its first Quantitative Easing (QE) program.

What this picture says is, over the past eight and a half years, the quality of your investment have been completely irrelvent.

By holding only investments of quality, you’ve made a grand total of not quite 2.6% compounding on your investment, while the S&P 500 is up almost 300%.

Have the value of the quality stocks in world gone up over the past eight and a half years? Yes, but its not because it was of quality, but because ALL stocks have gone up ever since the start of quantitative easing.

The balance sheets of Big 4 central banks, started exerting its massive gravity on everything BUT Quality. That’s not an accident, by the way. These central banks don’t care about rewarding “good” companies. In fact, if they care about anything on this dimension, they care about keeping “bad” companies from going under.

And its not just stocks that are affected.

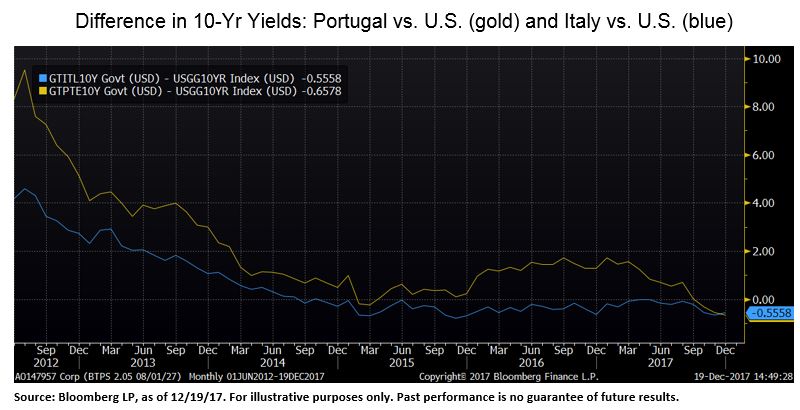

Looking at the chart above, the gold line is the spread (difference) between Portugal’s 10-year bond yield and the U.S. 10-year bond yield, and the blue line is the spread between Italy’s 10-year note yield and the U.S. equivalent.

In “normal” times, a country with a weaker set of macroeconomic characteristics (high levels of national debt, say, or maybe low productivity) will have to offer investors a higher rate of interest to borrow their money than a country with a stronger set of macroeconomic characteristics.

So in the summer of 2012, when Portugal and Italy were both looking like deadbeat countries, they had to pay investors a much higher rate of interest than the U.S. did to attract the investment … about 9% more for Portugal and 4% more for Italy. Those are enormous spreads in the world of sovereign debt!

This chart begins in the summer of 2012, when the ECB announced its intentions to prop up the European sovereign debt market directly. Since that announcement — even though both Portugal and Italy have higher debt-to-GDP ratios today than in 2012 — the spread versus U.S. interest rates has done nothing but decline. Driven by the commitment of the ECB to “do whatever it takes” and to be not only a last-resort buyer but also a first-in-line buyer of Portuguese and Italian debt, it now costs LESS for these countries to borrow money for 10 years than the U.S.

This is utterly insane.

But, its an understandable insanity, when you consider that the German 10-year bond yield is currently about 30 basis points, and was actually negative (meaning that you had to pay the German government for the privilege of lending them money for the next 10 years) for about six months in 2016. Meaning that at least with Italian and Portuguese debt you’re being paid something (a little less than 2% per year). It’s an understandable nuts when you consider that the Swiss 10-year bond still sports a negative interest rate and has been negative for the past two and a half years.

The Bank of Japan in January 2017 surprised markets by adopting negative rates. The European Central Bank in 2014 was the first major central bank to push the rate on deposits parked with it overnight to below zero. Central banks in Sweden, Denmark and Switzerland also have implemented negative rates.

As of 2018, more than USD 10 trillion worth of government bonds around the world held yields below zero, according to Bloomberg. Something that is IMPOSSIBLE under a (good country => good bond) concept. No country is so good that you pay them to borrow money from you!!

But it’s entirely possible under the immense gravitational force of massive central bank asset purchases.

Here’s the kicker. Above is the chart that shows the spread between Greek 10-year sovereign bonds and U.S. 10-year notes. In 2012 you were paid 24% more to lend money to Greece. Per year!

Today you are paid less than 2% more to lend money to Greece rather than the United States. For ten years. To Greece. A country that has defaulted 5 times in modern times, and spent 50% of its time as an independent country in default.

Wow. Just wow.

How does this relate to Malaysia.

Malaysia on the other hand, we have a goddess in the previous Bank Negara Governor, Zeti.

Instead of capitulating to that insanity, she kept interest rates at a sane level. In 2008, she only dropped the interest rate from 7.05% to 5.8%. It is currently at 6.6. However, we should also note that, unlike in the Big 4, banks in Malaysia do not actually rely on Bank Negara for financing.

Instead they go for deposits and bond issues. Which is something like 4%-4.3% these days. This would be a more relevant risk free rate of return for Malaysia.

In comparison, the Federal Reserve rate in US fell from 5% to 0.25% and stayed there from 2009 to 2016, before now rising to 1.5%.

As interest rates have a direct proportion to the level of money flowing into the stock markets and therefore its performance. It would appear the subsequent performance is also roughly proportional.

In 2017, the KLSE index returned 9.53% while the S&P index returned 20.37%.

Edit: As Fabian explained, the better rate to refer to is the Overnight Policy Rate (OPR). This one is currently at 3%, which is double that of the US.

Why is the Malaysian risk free rate so high?

One of the main reasons risk free rate or deposit interest rates are so high now, is due to this lovely new accounting standard called MFRS 9.

Unlike in previous standards, now every single one of your financial assets must be impaired based on percentage of default. With a minimum of 1% or something.

This means, assets like federal treasuries, or Malaysian bonds which were previously not impaired at all, must now be impaired.

As these impairments will affect the Common Equity Tier 1 ratio of the banks in Malaysia (This ratio is tightly regulated by BNM). Malaysian banks are now fighting very hard for new deposits to buffer up these ratios.

The fixed deposit rate of Alliance bank of 4.3% is higher than the interest rate of a housing loan from Hong Leong of 4.15%.

Yes, I’m not kidding.

In addition, effective interest rates/returns of 15-25% can be obtained from P2P platforms. Which is fantastic returns with relatively low volatility and risk (if you do your homework properly, historical impairment is also less than 2%).

Psychological Effects of low interest rates.

There was a study done where 2 groups of people were given these scenarios.

Group A: They were given a choice of a 1% risk free deposit, or a riskier investment that gave with a 6%. With marginal increase of 5% for the risk taken.

Group B: They were given a choice of a 5% risk free deposit, or a riskier investment (exactly as group A) that gave with a 10%. With marginal increase of 5% for the risk taken.

What researchers noticed was that 5 times as many people in Group A took the riskier option than Group B. Despite the marginal increase in reward for the same amount of risk being exactly the same.

This means that people psychologically expect a certain minimum return, and they will take whatever risk necessary to get that return.

As markets are dynamic, this means that the stock markets of countries where risk free rates are low, will become very overvalued as people are much more willing to take on the additional risk and invest in stock markets to get their minimum expected return.

This is especially compounded in Japan and Europe, where interest rates are negative.

“In a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return”

Warren Buffet.

Future effects of this scenario

“You can read Adam Smith, you can read John Maynard Keynes, you can read anybody and you can’t find a word to my knowledge on prolonged zero interest rates—that is a phenomenon nobody dreamed would ever happen

That doesn’t mean I think it’s the end of the world when it ends, but I don’t think anybody knows exactly what the full implications of negative rates will be. I hope to live long enough to find out.”

Warren Buffet.

Lets try and understand the future.

One thing is for certain, extremely low to negative interest rates and money printing cannot last forever. Banks around the world now are taking steps to slow down or unwind their federal balance sheets, and increasing interest rates.

Why do they need to do that?

Well, if they don’t, imagine if a recession happens when interest rate is negative and money is being printed. What other tools do a government have to arrest this spiral then? Basically none. The effects will be utterly catastrophic.

As interest rates rise around the world, the flow of money to equities will slow and possibly reverse, resulting in a drop in equity prices, unless companies somehow manage to still increase earnings year on year. Ie, increase in productivity per dollar.

A recession is likely to come, and the piper must be paid.

Countries like Japan, Europe and US will be greatly affected. China less so, as the government is taking very decisive steps now to slow it down and pare back debt as it is.

Malaysia will also be affected, as when recession happens, correlation of everything goes to 1. However, it should not affect us as much as the stock market here is not that overvalued yet.

However, the outflow of foreign funds as interest rates rise is likely to make things very interesting in Malaysia.

Neoh Soon Kean may very well say that the biggest sale in stocks is happening again in the future! The last time he said that was in 1999 during the Asian Financial Crisis, when the market crashed more than 70%.

Cheers.

====================================================================

Facebook: Choivo Capital

Website: www.choivocapital.com

Email: choivocapital@gmail.com

More articles on Choivo Capital

(CHOIVO CAPITAL) MYNEWS (5275) – Dr CU in da house. 66% Upside

Created by Choivo Capital | Dec 09, 2020

(CHOIVO CAPITAL) WCE (3565) – When the roads align. 562% Upside.

Created by Choivo Capital | Dec 05, 2020

(CHOIVO CAPITAL) BAT (4162) - Budget 2021 (The Dark Knight Rises)

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) LIONIND (4235) - Budget 2021, Rising Steel Prices

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) KRONO (0176) - Is it Alibaba (Alibaba Cloud)? (SUMMARY)

Created by Choivo Capital | Nov 03, 2020

Discussions

5 people like this. Showing 14 of 14 comments

Fabien Extr. That was what I thought that the OPR is 3% and not 6%. BTW, do you see Malaysia OPR going up this year and if so to what level. Thank you in advance.

2018-01-21 11:40

Market is pricing in 25bps hike, prob in Jan or March. At most, consensus view is 2 rate hikes max this year to 3.5%.

2018-01-21 12:18

@Fabien

You are probably right. I have not audited banks before. So my understanding is mostly from some brief reading.

Thanks for the comments!

2018-01-21 13:45

https://omightycap.wordpress.com/market-data/

Malaysia, PE:18.60 Price/Book:1.70 DY:3.00

Singapore, PE:11.00 Price/Book:1.20 DY:3.10

And yet the interest rate in Singapore is much lower than Malaysia.

2018-01-21 16:35

How about comparing with other ASEAN countries like Philipines, Vietnam etc? Their interest rates are not low like US or Japan, but their stock performance in 2017 were much better than Bursa.

Thus, I think the relatively lower stock performance in Bursa is not solely due to our interest rate.

2018-01-21 20:08

Value88, true. It's one of the factors, but I consider it the main one.

For asean countries, if I have to venture a guess, it's because their countries are far less developed and so double digit growth on companies is more common.

Also their stock markets are alot newer than ours. When the Malaysian stock market first started, people were truly gambling in the market and frying everything up to the sky. MUIIND was worth more than RM20. While it's only 20 sen now.

Cambodia's stock market got less than 20 companies. I imagine Vietnam's is not that much bigger.

2018-01-21 22:11

No worries, Jon. Just sharing for the benefit of everyone in i3.

I'm ex auditor too but have been working in the banking industry for close to 10 years now.

2018-01-21 23:04

Thanks Jon.

Another factor causing Bursa's under-performance in 2H 2017 was probably due to coming election which raises the uncertainty level.

Market does not like uncertainty.

2018-01-22 17:46

The GREECE stock market index

(1) 1999 Index peaked at 6500

(2) 2003 Index bottomed at 1500

(3) 2008 Index peaked at 5400

(4) Today, 2018, the Index is at 727 (a drop of 86% from its peak)!!!

2018-08-23 21:40

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

YTL Power Shares Extend Decline After MACC Query Over Subsidiary

2

AmInvest Research Reports

3

Good Articles to Share

4

Good Articles to Share

5

Good Articles to Share

6

Good Articles to Share

Pope In Asia: The Complex Relationship of Catholicism in Timor-Leste and Indonesia | Insight

7

Good Articles to Share

ImpactX Sports Group CEO Xavier Gutierrez on the economic impact of Latino fandom in sports

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Fabien Extraordinaire

Current OPR is at 3%. With major central banks around the world embarking on synchronized normalisation of interest rates given the synchronized growth in global economy, our local bank has to hike to maintain the interest differential.

MFRS 9 is not the main factor why banks are competing so aggresively for deposits. It is the LCR and NSFR that they need to comply with, to maintain the regulatory expectations in regards to liquidity and funding structure. Moreover, there will be added capital buffer requirements in the form of capital conservation and countercylical capital buffer that the banks need to provide in their capital ratios.

2018-01-21 10:39