Choivo Capital

(CHOIVO CAPITAL) An estimate on the real refinery earnings of (HENGYUAN)

Choivo Capital

Publish date: Fri, 16 Mar 2018, 01:45 AM

Well, what is there left to be said about this company? Every kind of valuation has been done, with FV from RM4 to RM42.

Quarters have been predicted and failed (and succeeded once). By now, I bet quite a few members have read enough to be armchair experts in refinery types, crack spreads, oil prices, derivatives, and forex.

Well, I think there is one thing left to be said. I don’t think anyone really asked this question.

Just how good is the refinery of Hengyuan? and, What is the earnings flowing from the refinery alone?

They are a few factors that affect the profits of refineries.

- Derivative Gains/Losses (Due to oil price movements).

- Stockholding Gains/Losses (Due to oil price movements).

- Stock write down or write backs (A small factor usually).

- Impairment/Writedown on property (Small factor most of the time, but a HY got a RM461mil hit in 2014).

- Forex Gain/Loss (Can be a big deal).

- Crack Spreads (Duh)

But from what we can see the last couple months, its general futile to try and short term quarters or estimate long term earning power by trying to predict crack spreads, oil prices and forex movements.

Why is it important to estimate the long term earning power instead of the next quarter?

Well? What is the purchase of equities other than potential earnings/cashflow of companies paid today?

Why would I say it’s futile? Let’s see the following predictions.

Oil Price will go up.

This means,

Stockholding gains.

Derivative losses, as they hedge against increase in oil prices.

Compression of crack spread as there is a time lag.

Oil Price will go down.

This means,

Stockholding losses

Derivative gains, as they hedge against increase in oil prices.

Expansion of crack spread as there is a time lag.

All of these net off against each other. So often, you don’t see that much of a change.

Or if you're the kind to try and use crack spreads to predict profits.

If it goes up, everyone delays down maintenance, increasing supply and resulting in spreads to go down. As we clearly just saw.

If it goes down, everyone go do maintenance, and spread go up.

At the end of the day, you only need to know this. On average there will always be a positive spread between the net price of petrochemicals sold and the price of oil per barrel. It’s impossible for the total price of refined goods to be less than zero.

So what is the eternal constant? What can you try and understand that is of worth? What is the truth of refinery business that will not change from day to day? What can we try and find out that will still be useful next year?

Its simple.

Just how good is your damn refinery?

How efficient is it at refining stuff?

Can it refine at a profit if crack spreads are thin? Who cares if spreads are fat, during that time, everyone also can make money. A rising tide lifts all boat.

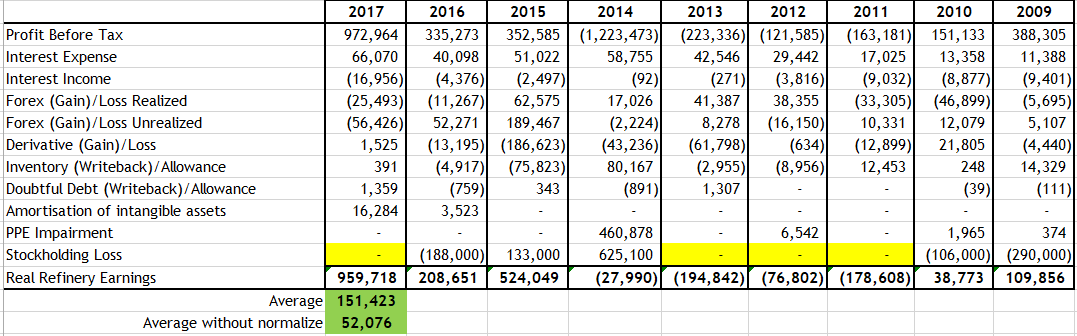

The real refinery earnings of Hengyuan.

Here is a table I created to try and to estimate the real refinery earnings of Hengyuan over 9 years. Why not 10, because I got lazy at 9. And it seems a decent enough spread between high and low oil prices etc.

I normalized the refinery earnings by removing a few items such as,

- Interest Expense

- Interest Income

- Forex (Gain)/Loss Realized

- Forex (Gain)/Loss Unrealized

- Derivative (Gain)/Loss

- Inventory (Writeback)/Allowance

- Doubtful Debt (Writeback)/Allowance

- Amortisation of intangible assets

- PPE Impairment

- Stockholding (Gain)/Loss

Which should give me a rough estimate of how capable and efficient this refinery/ refinery business is.

For the record, the PWC auditors seems to be retarded. So many figures in the cash flow seem to change from year to year. And I can’t seem to tie the unrealized forex to the "Profit/Loss Before Tax" note. Which is just weird.

So I’m probably off by a few hundred thousand to a few million each year. But if an investment needs me to be accurate to the dollar to determine its value. I probably shouldn’t be investing in it.

You don’t need to know the weight of a women to know if she’s fat, or the age of a man to know if he’s old. The value of an investment should be obvious.

I think there is a decent mix, we have 2009 to 2012 when oil prices were high, and the 2013 to 2014, during the big drop, 2015 to 2016 when there was a sustained low price, and in 2017 when oil prices shot up to 50-60 or so.

A few things to note. The main item, stockholding losses, I was unable to find that amount for a couple of years. It wasn’t disclosed. But I think it evens out, as even if it was a loss from 2011 to 2013, the gain from 2017’s should be large enough to cover it.

If 2011 to 2013 was a gain, it’s for the better anyway. It’s better to err on the side of caution. But I suspect it wasnt disclosed then as i wasnt that material then as oil prices were relatively stable.

Assuming we use the equalized earnings at RM150 mil per year, Hengyuan is the trading at 19 times earnings. Do note its worse for the unequalised one as that is only RM52 mil per year.

But that’s not the complete story

Other salient points.

- The refinery made losses last time as they had to sell to Shell at a low price.

For some reason, everyone keeps saying this, but for the life of me, I can’t find it anywhere in any of the annual reports. Nowhere does it say that Hengyuan used to sell petrochemicals to shell at a discount.

I think this is just one of those things that appeared in an OTB newsletter and everyone just took it as the truth.

In addition, even if it were true, you cannot price it too low. There’s something called transfer pricing documents, which ensure that you cannot move profits to a lower corporate tax company too much. Basically you need to sell at arms length price.

But if this is really true and materia. We can expect some resilience in the earnings moving forward. But nobody says they cannot sell to the new mother company at a discount too. But would not make sense as Corporate tax rate in China is 25%, Malaysia’s is 24%.

- You cannot make your earnings pretty without additional cost.

If a company tries to make their earnings beautiful, by hedging their spreads, forex, and oil prices. They will probably incur significant cost. Options are not free. Covering your downside cost you money.

I have no idea why PETCHEM earnings are so beautiful though. Tell me if you know why!

- RM750mil upgrade will increase production by 20%.

Do you know how many time they bought PPE worth more than 500m in the last 10 years. Quite often. And as we can see they can actually make refinery losses. This could mean your losses increase by 20%.

- Plan to venture into petrochemicals trading.

Don’t forget, can make money, can also make losses. Is this their core capability. Trading and running a business is a completey different game. You want to fight with VITOL? One of the many companies that focus on trading energy commodities. They do this for a living, you're doing this on the side.

How good is VITOL? They are one of the biggest despite being privately held. No need outside money. Thats how much money they make and how good they are.

- IMO 2020.

No comment, too far into the future. If everyone sees this a threat, won’t everyone upgrade their refineries? In which case, wouldn’t your advantage hilang d?

Conclusion.

I'll probably just hold my 2% position. It was at 3% when i rebuy in at RM14.3 after selling everything at RM17. I think its a decent punt.

But as an investment, i dont think i know enough about it, nor is the value so obvious that its a no brainer.

Good luck everyone.

Also let me know if i missed out on anything, or am wrong about something.

No point having an ego in the market. If im wrong, let me know, so that i can buy more and make money too!

====================================================================

Facebook: Choivo Capital

Website: www.choivocapital.com

Email: choivocapital@gmail.com

More articles on Choivo Capital

(CHOIVO CAPITAL) MYNEWS (5275) – Dr CU in da house. 66% Upside

Created by Choivo Capital | Dec 09, 2020

(CHOIVO CAPITAL) WCE (3565) – When the roads align. 562% Upside.

Created by Choivo Capital | Dec 05, 2020

(CHOIVO CAPITAL) BAT (4162) - Budget 2021 (The Dark Knight Rises)

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) LIONIND (4235) - Budget 2021, Rising Steel Prices

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) KRONO (0176) - Is it Alibaba (Alibaba Cloud)? (SUMMARY)

Created by Choivo Capital | Nov 03, 2020

Discussions

3 people like this. Showing 43 of 43 comments

we are talking about a company with $ 12 billion turnover a year......and only 300 million shares. ...the fluctuations translated into the PL and eps is going to be wild....both + and -................are you ready for the rides?

2018-03-16 03:09

with such turnover, such high risk of stock losses, fluctuations in currencies, crude prices, engineering risks and financial risks and huge capital requirements......nobody will do this business unless they think they can do $ 100 million pre tax profits per quarter. ...or say $ 1 EPS per annum........that is the minimum required profit target......so, what is the fair price....until things change or plant obsolete and cannot use.

2018-03-16 05:28

the fair price is probably around current levelsubject to short term fluctuations.....and until things get clearer with the shareholders' plan and with Rapids., .....

in the longer term, this company will be involved in transfer pricing between China and Malaysia and no more transparency.

2018-03-16 05:34

Like what Tom always said there are so many dream makers on i3. It is up to readers to filter what is good analysis or trash

2018-03-16 07:47

In a research paper in Facts Global Energy, it was posited that global refinery utilization will remain tight above 86% up to 2025. As we know, utilization at that rate is considered fully utilized. Your analysis fail to address the causes that result in significant improvement in crack spread at the present moment compared to previous years. Due to poor profitability in the past, oil majors have underinvested in refineries. Look, a shutdown caused by Hurricane Harvey caused mayhem across the entire refinery sphere, to the point HY is able to book massive profits halfway across the globe. What does that tell you? It indicates that at the present moment, there is a shortage of refining capacity globally with very little spare capacity, where utilisation rate is at 83%. Yesterday's news revealed that US gasoline inventory is low, while crude inventory remains high, a condition that's very favorable to refineries. Even though crack spread has softened somewhat since January, most of the fact point to a tight market in the refinery business which will keep crack spread buoyant in the near term, at the very least.

2018-03-16 09:26

soo...assuming this refinery makes a lot of money.....what is the track record of this holding company in respect of the rights of Malaysian minority shareholders in sharing a portion of the profits?

truth be told.....all the buying and selling in this share in recent months is done by retailers such as you, very few by fund companies except for the selling by old shareholders.......

2018-03-16 09:42

But really, my concern now is if i missed out on something.

"The refinery made losses last time as they had to sell to Shell at a low price."

Specifically this. Anyone have any idea where i can find it in the Annual Report or?

2018-03-16 10:01

@soujinhou

Good point. Now the question is, how quickly can previously closed refineries be reopened? And how hard is it to upgrade current refineries. How much time will it take?

A lot of things can happen in 6 months to a year.

The analysis of this company is a little too hard for me. They don't have a retail division to make earnings a little more stable. The Refinery business is not top class i think.

Phillips 66, a refinery in the US never made a loss for the last 8 years. At worst, in 2010, earnings dropped to less than a billion USD.

2018-03-16 10:12

btw @jon,

ur analysis is unbiased, unlike the jokers in hy.

seldom see any good analysis in this forum.

2018-03-16 10:23

I estimate they will make 40 sen net EPS March quarter...whether share price up or down up to you.

2018-03-16 10:40

For Dec 2017 quarter, I estimated they will make 50 sen net EPS, they reported 61 sen net EPS.

So I was quite accurate for Dec quarter.

2018-03-16 10:48

@jon and @sou,

the higher than usual crack spread is only localized in us refineries.

the reason is becos of supply and demand.

2018-03-16 11:06

I think to an extent spreads are global as oil and its products can be shipped very efficiently even in an embargo.

VITOL have very clearly shown that when they shipped oil from iran despite the US embargo.

2018-03-16 11:10

ah, thats where most ppl r mistaken between physical and futures.

the crack spread calculated by most here r based on nymex prices but the actual traded physical prices r different.

as a result, the refining margins of us refineries and non-us refineries r different from what most here calculated.

thats why there is the arbitraging trades between different geographic regions.

2018-03-16 11:23

@jon

May I know why interest expenses and income are excluded to calculate real earnings? I thought interest expenses were part of cost of doing business.

2018-03-16 23:52

if one wants to know how efficient a manufacturing plant is operationally, interest expenses/incomes r excluded.

2018-03-17 00:07

HY says themselves they benefited from the hurricane damage in Sept and Dec quarters......expected the March results to be lower.

2018-03-17 00:15

accountants are accountants but can accountants think beyond accounting and get into investing?

2018-03-17 00:43

Limpeh is a chartered accountant.

Its not about your paper qualifications, its about your mind and how you think.

qqq3 accountants are accountants but can accountants think beyond accounting and get into investing?

17/03/2018 00:43

2018-03-23 13:54

choivo capital

so now you are in private equity and asset management?

asset management very tough job. Every client have different risk appetite.

2018-03-23 14:25

last 12 months, the big caps and the conservative managers did well.

the cowboy ones have their cowboy methods exposed and found wanting.

2018-03-23 14:28

KLCI big caps are very overvalued, that's why our KLCI index performance over 20-30 year less than FD.

Conservative managers who only buy big caps are not conservative. SAPRNG is a big cap.

You are only conservative if your conservative when it comes to valuation, and that can come from any stock or asset class imho.

Posted by qqq3 > Mar 23, 2018 02:28 PM | Report Abuse

last 12 months, the big caps and the conservative managers did well.

the cowboy ones have their cowboy methods exposed and found wanting.

2018-03-23 14:37

I am still in audit, the fund is something i do on the side.

It is, if you want every cent and every investor.

I don't. I want only the investors who understand my philosophy perfectly (its pro's and con's), willing to give long term money (3-5 year lock)

But its still stressful, knowing that people are relying on your. And this is their savings built over a long time. Other than their family, this is probably the second most important thing to them.

I have to say, for the last 2 months, i did consider just paying everyone back with interest and just invest on my own. Its easy for me to just take on the paper loss, because i know its not real, i know what my stuff is worth.

But it my not be so easy for others. However, they have my word that principle and profit is guaranteed. And they know i am unleveraged and have enough cash in hand to pay them all now if they want.

I guess we'll see in 5 years (at least) if im possibly any good as an investor, or just good at talking. Bu we'll know for certain in 20. I hope i last that long.

Posted by qqq3 > Mar 23, 2018 02:25 PM | Report Abuse

choivo capital

so now you are in private equity and asset management?

asset management very tough job. Every client have different risk appetite.

2018-03-23 14:43

You are only conservative if your conservative when it comes to valuation, and that can come from any stock or asset class imho.

================================================================

Sapura...only $ 3 billion market cap.....not really a big cap.

There are good reasons why big caps and monopolies and GICs have premium valuations........

there are more to valuations than meets the eye.

returns per beta is also very important.

example.....two stocks both go from $ 10 to $ 20.

Stock A slow and steady go from $ 10 to $20.

Stock B wild fluctuations, up and down go from $ 10 to $20.

any genuine investor would prefer stock A.

2018-03-23 14:50

Haha qqq3,

Different strokes for different folks.

You place more care on volatility of price. And you consider it risk.

For me, price volatility is not a risk to me. Risk for me is permanent loss of capital.

If i buy an overvalued company, in my mind, i just made an instant loss, because if i were to buy a private company, i would never touch it at that valuation.

Now, if i could predict prices with a high accuracy and have an edge in it, i would be a trader. But i can't.

The only thing i know i can do well in, is being somewhat accurate in determining a range of intrinsic value for a company.

So my only criteria is, discount to intrinsic value.

Now, i definitely do feel a little inclined and have opinions on the market, and where the price may move according to the charts. But this does not determine my investment. But i may lean a little here and there. :)

2018-03-23 14:57

jon

actually it is the other way round.....there is less certainty about intrinsic value and more certainty about what is a good company/ good share.

2018-03-23 15:22

How do you mean, care to elaborate?

qqq3 jon

actually it is the other way round.....there is less certainty about intrinsic value and more certainty about what is a good company/ good share.

23/03/2018 15:22

2018-03-23 15:25

jon

actually it is the other way round.....there is less certainty about intrinsic value and more certainty about what is a good company/ good share.

my definition of good includes things like....predictability, responsible organisation, minority rights, size, industry, and of course most important...is History.....unless it is a start up then of course no history and have to be evaluated on growth prospects.

2018-03-23 15:31

Ahh,

I see. I do focus on that as well. but i also have a belief i abide by.

There is no company so good, that a high enough price will not turn it into a bad investment. And there is no company so bad, that a low enough price will not turn it into a good investment.

My favorite companies are of course, good companies at fantastic prices. But they are hard to get. But if this market continues, it will be come alot easier!

2018-03-23 15:34

intrinsic value then becomes the last step.....not the first step.

and is the most uncertain step in the process.

2018-03-23 15:35

jon...

the reality is...the range of possible value or acceptable value for a truly great company is much wider than you think.

2018-03-23 15:37

maths and valuations may sound objective and scientific....

but actually maths and valuations is the one that has the biggest acceptable range.

2018-03-23 15:39

actually who is more interested in prices?

traders and speculators like me....I don't intend to hold for long so both entry and exit are the most important factor.

traders and speculators have completely different set of parameters from investors.......

https://klse.i3investor.com/blogs/qqq3/151380.jsp

2018-03-23 16:02

Haha, i dont think i know OTB beyond knowing who he is on i3.

Yeah, i think we are coming from completely different perspective.

https://klse.i3investor.com/blogs/PilosopoCapital/150345.jsp

I wrote something similar.

2018-03-23 17:21

I stand by it.

As i said, things will obviously be very different moving forward if HY was really selling refined products to Shell at below market price. But i cannot find anything in the reports that say that.

Also HYSD is a good refiner, So could be a positive. They may actually run it well.

Which is why im holding my 2-3% position.

2018-04-13 14:02

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

https://dividendguy67.blogspot.com

3

4

Good Articles to Share

Could Kamala Harris beat Donald Trump in November's presidential race?

5

Good Articles to Share

Iranian warship capsizes during repairs in port of Bandar Abbas

6

Good Articles to Share

7

Good Articles to Share

Jonathan Turley unveils exciting new book 'Free Speech in the Age of Rage'

8

Good Articles to Share

Why Impossible Foods signed hot dog-eating legend Joey Chestnut #yahoofinance #youtubeshorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

qqq3

the risks to a minority shareholder....

- how are minority rights protected? what is the track record of the holding company? How financially sound is the holding company? Hengyuan ,Shangdong is known as a teapot, because it is competing against the state owned giants ...lots of problems/ issues they have.

- what are their plans in acquiring this plant in Malaysia?

- what are the merits of the eps from this very old plant with minimum depreciation? and therefore inflated profits and eps.

-the plant has a cost of $ 3 billion , NBV of $ 800 milllion and annual depreciation of $ 150 million.

a similar plant today will cost $ 6 billion to $ 10 billion...but the more important question is...how long can this plant be economically viable?

-what is the scenario when Rapids is ready in 2020?

-Shell is already supplying Euro 5 diesel to East Malaysia ( you can see that from advertisements)...surely not from this plant.

I mean, you can make the calculations look very complicated and impressive...but, is it on the right track?

There are 3 parties....Shell who thinks it is worth scrap , Hengyuan, Shangdong who is willing to take it over.....and as minority shareholders, are your rights protected?

As a portfolio manager...your priorities are good management, good business, your rights are protected, the company has good and strong parents, you can get your share of the future earnings, the earnings are stable and predictable...and preferably growing.

How much are you willing to pay? To gamble?

me...I think Hengyuan came to Malaysia not to benefit the minority shareholders in Malaysia, but to secure a refinery outside China.....they are obvious advantages to them in this strategy.

me...unlike Pteron who has to deal with the Malaysian public because they have petrol stations and retail customers......this Hengyuan do not even need to deal with the Malaysian public as long as they don't break the laws of the country...and it is not their practise to meet analysts or journalists to discuss their plans.

2018-03-16 02:59