Icon8888 Gossips About Stocks

(Icon) Hengyuan Refining (2) - The Story Behind Shandong Hengyuan's Entry Into Shell Refining

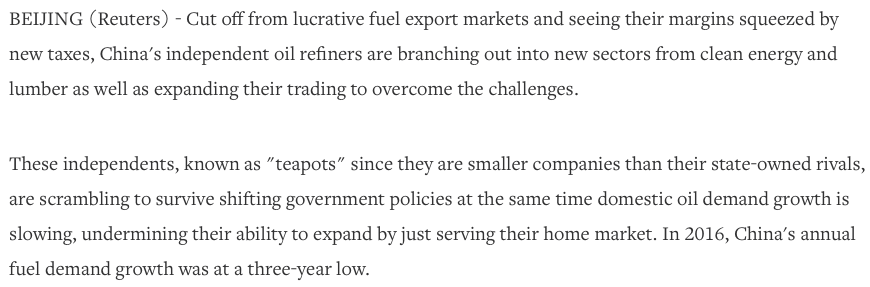

1. The Teapots

Shandong Hengyuan is an enterprise backed by Shandong's local government (some said it is privately owned. Whatever it is, I don't think the nature of ownership is important).

It is a Teapot Refinery, a term used to describe refinery with capacity as small as 20,000 to 100,000 barrels per day (bpd). Shandong Hengyuan's capacity is 70,000 bpd while the capacity of its newly acquired 51% owned subsidiary Hengyuan Refining at Port Dickson (previously Shell Refining) is 156,000 bpd, twice its size.

There are about 20 Teapots in China, 80% of which are in Shandong province. Their presence is quite significant. Collectively, they accounted for 15% of China's crude import and 20% of its refining capacity.

Teapots are more efficient and profitable than state owned big boys such as CNPC, Petrochina and Sinopec. One of the reasons is because the SOEs incurred high assets acquisition cost during the oil boom years.

The SOEs are hostile towards the Teapots and constantly lobby against them. As a result, the Central Government imposed all kind of conditions on the Teapots. Teapots were not allowed to import crude directly from overseas and have to buy from SOEs, thereby allowing SOEs to make a cut (this restriction was uplifted in 2016). The Central Government also imposed export quotas on Teapots. In short, life for Teapots is not easy.

If that is the case, why did the government allow the Teapots to mushroom in the first place ? That was actually caused by the unique dynamics between the Local and Central Government in China.

Teapots came into existence because of the policy pursued by the existing provincial governor Guo Shuqing. It was a way to generate economic growth, create employment and increase tax revenue. All these are good things, so the Central Government has no issue with it. However, when the Teapots became too successful and threatened the SOEs, the Central Government stepped in to intervene. That is how they ended up with the current mess. Welcome to China !!!

As a result of the unfriendly policies, Teapots started looking for ways to diversify. Some moved up the value chain to produce chemicals, one ventured into lumber business, one ventured into Lithium battery business, etc. And of course, diversification overseas is always an option, provided the opportunity is there.

And that opportunity came knocking on the door one day.

2. The Deal

In February 2016, Shell International announced that it was disposing 51% equity stake in Shell Refining to Shandong Hengyuan. Shell has been in Malaysia for a long time (at least since the 1960s). It has three major divisions : upstream, refinery as well as petrol stations. It is not difficult to guess why Shell wanted to exit the refining business. Oil price has collapsed since 2014. The disposal was likely part of its streamlining exercise to strengthen its financial position.

What was intriguing about the deal was the pricing. Shell disposed of its 51% stake in Shell Refining to Hengyuan at RM1.92 per share. This represented a huge 60% discount to Shell Refining's market price before announcement of the deal. The official reason given by Shell International was that Shandong Hengyuan has demonstrated ability to refinance Shell Refining's borrowings. This is actually a very credible explanation : banks lent money to Shell Refining in the past because they trusted the Shell name. But now a Teapot has emerged as the new controlling shareholder, the risk profile has changed beyond recognition. The banks wanted their money back. Whoever that can pull off a refinancing deal will be the most qualified candidate.

Still, one can't stop wondering whether Shell International has tried hard enough to find a better buyer. Shell Refining is a very valuable asset, it is really a big waste to sell at such a depressed price. Afterall, it is not like Shell is facing bankruptcy during that time. Why in a hurry ? Until today, many investors, analysts and fund managers are still scratching their head.

Maybe they can stop scratching their head now. I think I might be able to provide an explanation.

3. The Partnership

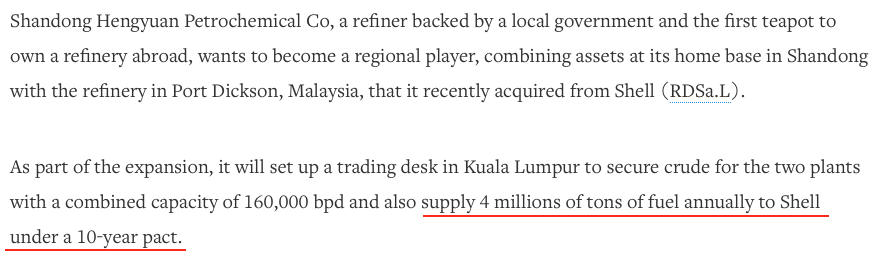

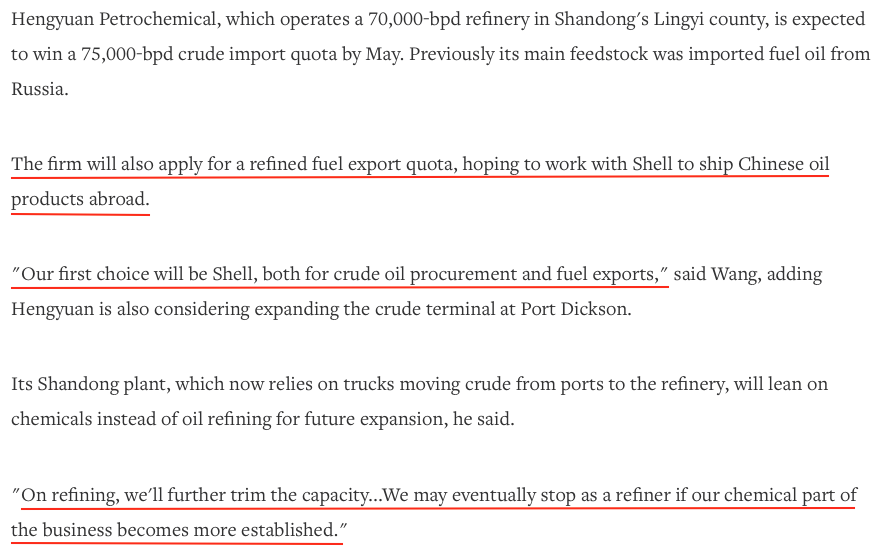

It seemed that Shell International's disposal of 51% stake is not the end of the story. Pursuant to the transaction, Shandong Hengyuan has entered into a 10 year agreement with Shell to supply it with 4 million tonnes of fuel annually.

This explains a lot of things. First of all, it explains why Shell International was willing to part with its 51% stake at such depressed price. The Shell Group can claw back some of its lost value (probably through attractive pricing of products) through the subsequent long term supply agreement.

Secondly, it explained why an ex Shell empoyee was appointed as the Managing Director of Hengyuan Refining. The objective is not to protect Shell's interest (there is nothing to protect anyway. Shell International does not own any more stake in Hengyuan Refining). I believe it is more to make sure that Hengyuan Refining can continue to meet the high standard required by Shell International for its products.

It seemed that Shandong Hengyuan's relationship with Shell is not limited to Malaysia. The Chairman elaborated on how they intend to work with Shell on various other business oppurtunities.

4. Concluding Remarks

I have fed you with a lot of information. But this is not a business school, we are here to discuss how to make money from punting Hengyuan. So, what are the conclusions ?

The conclusions are as follows :-

(a) Once again, I would like to argue that the Hengyuan Group is not the same as the other dodgy Red Chips that faked accounts and information. It has an established track record in the industry. The details that I got from various news sources allow us to have a good feel of what it does, what problems it faced, what drove its recent acquisition of Shell Refiing and what its aspiration is.

(b) The long term partnership with Shell Group is a very positive point. Even though Shell has exited the refining industry in Malaysia, it is keeping its petrol stations operation.

The petrol stations are sourcing the refined products from Hengyuan Refining. Hengyuan will need to operate professionally to ensure no disruption of supply.

The government is actually a party to this arrangement (albeit invisible). Any disruption of supply to Shell petrol stations will create turmoil and adversely affect the economy. In other words, many pairs of eyes are watching the Hengyuan Group. Do you really think they will do stupid things like cooking their books ?

For more detals, please refer to the following articles :-

http://www.hellenicshippingnews.com/chinese-teapots-the-game-changer-in-chinas-oil-industry/

http://www.chinadaily.com.cn/business/2016-12/28/content_27795122.htm

https://www.ft.com/content/7fc95106-fc71-11e5-b5f5-070dca6d0a0d

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

6 people like this. Showing 39 of 39 comments

"What was intriguing about the deal was the pricing. Shell disposed of its 51% stake in Shell Refining to Hengyuan at RM1.92 per share. This represented a huge 60% discount to Shell Refining's market price before announcement of the deal. The official reason given by Shell International was that Shandong Hengyuan has demonstrated ability to refinance Shell Refining's borrowings. This is actually a very credible explanation : banks lent money to Shell Refining in the past because they trusted the Shell name. But now a Teapot has emerged as the new controlling shareholder, the risk profile has changed beyond recognition. The banks wanted their money back. Whoever that can pull off a refinancing deal will be the most qualified candidate."

Very interesting explanation which i never thought of. This is exactly due to the difference in way of thinking between engineers and accountants in Bank....

You cannot use technical explanations to convince Bank to provide you the fund...he he..

AND precisely the reason why market still unable to realize how cheap HRC is now.

2017-07-13 14:05

good point probability.

Anyone highlight risks of investing then?

Electronic cars, hybrid will be the future, all public transport and even airplane going hybrid or electronic very soon. Volvo 2019, London taxi very soon, Singapore alredi started automation of cars via electric.

2017-07-13 14:07

Paper...that is very very long way to go...

even it happens very fast dramatically... the supply and demand will cushion it. The moment demand comes down...shale oil will be the first to be killed...and it will have balancing effect on supply. The price will be retained.

These are energy...it price can come down...but will it ever lose its value? There is definitely a threshold price where fuel will be cheaper than these alternatives (solar, nuclear, wind etc).

meaning the price can come down...but the demand will always be there - simply because it is ENERGY.

everything you do in life...even bionic robots in future will need this.

2017-07-13 14:13

most reports I read signal 2020 is the tipping point. 2020 onward will see drastic changes in energy. The REVOLUTION after Internet of Things.

2017-07-13 14:15

actually if you want to talk about future...even humanity existence (at least the population growth) is under a big question mark?

all gdp will be shrinking then... Japan now would be the glimpse of the future to come for developing countries..

2017-07-13 14:21

Raider think...very unlikely...even with partnership...people will be willing to part their stake that cheap mah....!!

So the explaination can come from either that shell damn stupid or there are some payoff out of records.. as a reward for the cheap depress price loh....!!

In fact, raider think a combination of both loh...!!

This multinational treat shell refinery as peanuts pocket change mah..!!

So unlikely to raise too much hue & cry for the cheap disposal loh..!!

Same has happen to esso, a few years early...when it was sold for a song loh..!!

So the explaination can come from either that esso damn stupid or there are some payoff out of records as a reward for the cheap depress price loh....!!

Then u look at alcom again dispose at a depress price of Rm 0.64...today it is rm 1.73 plus rm 0.225 div loh...!!

Why within a few mths after the disposal alcom has gone up so much leh ?

So the explaination can come from either that Alcan damn stupid or there are some payoff out of records as a reward for the cheap depress price loh....!!

Having discuss.. the anomaly above the strategy is not whim on any self pity, it is how value investors can take advantage from the stupid transactions and how to tackle the false mkt perception loh...!!

If u have bought bcos of the stupid transaction price, raider says u can profit at least 100% loh...!!

For example EPF is so stupid to dispose shell at Rm 2.00 to rm 2,40 loh...!!

Reason there do not know how to value stock and overcome by Mr mkt loh..!!

2017-07-13 14:42

Posted by probability > Jul 13, 2017 02:21 PM | Report Abuse

actually if you want to talk about future...even humanity existence (at least the population growth) is under a big question mark?

all gdp will be shrinking then... Japan now would be the glimpse of the future to come for developing countries..

Thts why most fund managers invest in ASIA now. Emerging Markets as well. Population in Europe, US getting older after baby boomer time. same to HK, Taiwan, SG now as well.

China see much far than us. Africa is next growing places.

2017-07-13 15:18

For example EPF is so stupid to dispose shell at Rm 2.00 to rm 2,40 loh...!!

Reason there do not know how to value stock and overcome by Mr mkt loh..!!

They have no choice I guess. They have stop loss mechanism. they trade without emotion, only execute according to rules

2017-07-13 15:26

IF U WANT TO TALK FUTURE IS ALWAYS UP LOH....!!

FUTURE ALWAYS MORE PEOPLE LOH...!1

FUTURE PEOPLE ALWAYS BECOME RICHER BCOS OF COMPOUNDING AND INFLATION LOH....!!

FUTURE THERE WILL BE MORE CARS, MORE HOUSES, MORE MCDONALDS STALLS...MORE CONSUMPTION ETC...ETC LOH...!!

BE POSITIVE ...FUTURE MEANS MORE & MORE MAH...!1

FUTURE MEANS SHARE PRICE UP & UP LOH....!!

GENERALLY FUTURE MEANS MORE N MORE AND UP N UP LOH...!!

2017-07-13 15:27

Icon if you are planning to come up with a next article with quantitative valuations, suggest to explain on the USD Debt effects, how would the strengthening RM affects the qtr results. My accounting knowledge at kindergarten level..

2017-07-13 15:47

Risk takers all jumped into longkang.

I help Icon finish his title:

(Icon) Ekovest - Gigantic Money Machine Likely Intact. Time For Risk Takers To Jump In.... longkang

http://klse.i3investor.com/servlets/forum/600125959.jsp

2017-07-13 16:45

whether HY is a crook or not a crook is second important , most important it must convince us that it is capable like petronm to generate more FCF and reduce debt.

if not..... it is still better to keep it as girl friend and keep in the car not at home....

but beware of the fact that, girl friend is always more exciting than wife, never upgrade her to your wife and hope she will perform better than your wife if she still need to rely on heavy debt to live well......

2017-07-13 18:20

yeah just dont let the wife know...

obviously we can see the 'in & out' is more with gf..

once she is pregnant, u have to give her same status whether u like it or not...official or not...

2017-07-13 19:39

probability sifu,

based on your calculation, she should get pregnant fast, if not , this lady is too difficult to understand .......

2017-07-13 19:49

period just over...now fertile week (dont give up this limited chance)...next month already deliver...

after that she is as good as ur wife lor..

2017-07-13 19:53

I ready in out this lady a few times lah.....

in then enjoy the beauty with the sound of silence

out then come here to sing song loh.....

but never give up, the beauty is still there

2017-07-13 19:58

keep singing...but ensure nobody sings better than you...

u never know when she'll say bye bye to u..

now a lot of big shots with BMW eyeing her...

they are writing poems to describe her beauty in i3

2017-07-13 20:07

It is getting much attraction than the past. no regret to buy. Huge potential. Low price. Before it become very popular, better own it first. See like aseng said..in out many time...i guess many is watching closely to get in if they are not buy yet

2017-07-13 21:19

For those who haven't bought, please read this first. This is a fair piece of information, 自己保重,呵呵!

http://finance.ifeng.com/a/20160124/14186027_0.shtml

2017-07-14 00:45

The original intention was to sell the excess Chinese products through Malaysia, but failed because there is no quota.

http://f.sdnews.com.cn/sdcj/201705/t20170526_2246145.htm

2017-07-14 00:55

This is in 2014, the general manager said business was very difficult.

http://finance.sina.com.cn/chanjing/cyxw/20141122/001920888604.shtml

2017-07-14 01:00

Worst of all, ChongJiauJau aka the "banana salesman" was very cocky before but he has since deleted all comments and his personal cocky comments. I found out also the loser named "probability" also deleted all his cocky comments entirely wiped clean!!!! WTF? so probability and ChongJiauJau is actually same dude. Both accounts erased/deleted clean all their bragging cocky comments. Now I see what kind of loser this probability is! cowardly deleted all his cocky comments...I wouldn't caught him red-handed if he didn't delete those his bragging comments!

2017-07-14 07:49

Change of credible board members not a red flag ?

Just FYI, for those that doesnt read details. The 'successful refinancing' has resulted in the borrowing rates going up from LIBOR + 0.6% to 0.7% to LIBOR + 3.5%!

i.e. which means its a terrible financing terms and to give you an idea of the change in the risk profile for the Bank from vendor to new buyer.

Someone mentioned Shell wasnt doing well so they wanted to cash out now this business is suddenly so profitable ? No one asking the right questions seriously. What has changed and what did Heng Yuan bring to the table ?

Im no O&G expert, but i will just say this. Someone else mentioned that refining margins are fixed and they dont really have to 'worry' about prevailing oil price levels. Unless they are the only refinery around, market supply demand on refinery margins will apply. And if this was really true. why did an oil company like Shell sell at a super discount ?

What i believe is dont fight nature / gravity. O&G and Property sectors are downtrend and will continue to be but you can always try and argue they are gems still in the sector and justify just about anything.

2017-07-14 22:51

simple explanation:

see the figures from early 2016: convert to dotted graph to 'Area' graph for better visualization...

Gasoline:

http://www.cmegroup.com/apps/cmegroup/widgets/productLibs/esignal-charts.html?code=D1N&title=JUL_2017_Singapore_Mogas_92_Unleaded_%28Platts%29_Brent_Crack_Spread_&type=p&venue=0&monthYear=N7&year=2017&exchangeCode=XNYM

Fuel Oil:

http://www.cmegroup.com/apps/cmegroup/widgets/productLibs/esignal-charts.html?code=STS&title=JUL_2017_Singapore_Fuel_Oil_180_cst_%28Platts%29_6.35_Dubai_%28Platts%29_Crack_Spread_&type=p&venue=1&monthYear=N7&year=2017&exchangeCode=XNYM

2017-07-14 23:01

Post a Comment

Featured Posts

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-04 09:00:00

TURTLE SYSTEM 20

Hourly

SELL

2024-07-04 09:00:00

TURTLE SYSTEM 20

30 Mins

SELL

2024-07-04 09:00:00

TURTLE SYSTEM 55

30 Mins

SELL

Apps

Top Articles

1

TA Sector Research

2

3

AmInvest Research Reports

4

save malaysia!

5

6

7

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

probability

Even the precise mechanism of the Refinery Margin to be used for selling to Shell is mentioned in their Annual Report 2016 transparently.

This gives more certainty that HRC Earnings will reflect the local / regional (Singapore based) margins without hidden special discounts for Shell retails.

2017-07-13 13:53