Icon8888 Gossips About Stocks

(Icon) Lion Industries - Interesting Deal. I Keep My Mind Open

Last night, many Lion Industries shareholders could not sleep well (not me, I have zero exposure). Lion Industries just announced in the evening that it is paying RM537 mil to acquire the assets of Megasteel. Many panicked this morning and ran for the exit. Is the deal really that bad ?

Due to lack of industry information, it is difficult for me to ascertain the prospects of Megasteel and its impact on Lion Industries post acquisition. However, I picked up some interesting points from the announcement :

(a) the entire purchase consideration will be used to settle debts owing by Megasteel to its creditors. Not a single sen will go to William Cheng. It is obvious that this is not a bail out exercise. It is more like a forced selling by Creditors (meaning Lion Industries is there to pick up the assets at a bargain). In this regard, I give a PASS for corporate governance.

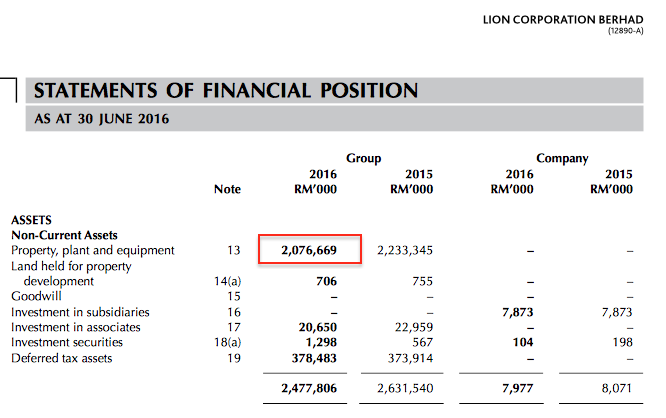

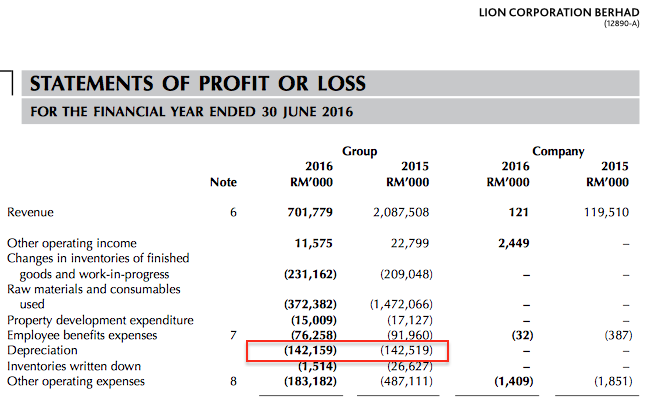

(b) The net book value ("NBV") of the assets is RM1.84 billion. Lion Industries is buying them for RM537 mil. A huge discount of RM1.3 billion. From P&L point of view, the reduction in NBV should lead to lower depreciation charges (Accountants please chip in here, as I am not an expert in this field). The following is extracted from Lion Corp's FY2016 annual report :

Its annual depreciation charges was approximately RM142 mil.

Based on RM2.1 bil and RM142 mil, it seemed that the assets had expected remaining lifespan of 14 years (being 2,100 / 142).

Now that Lion Industries' NBV of the assets is RM537 mil, annual depreciation charges would be RM38 mil only. A reduction of RM104 mil per annum compared to the original Megasteel.

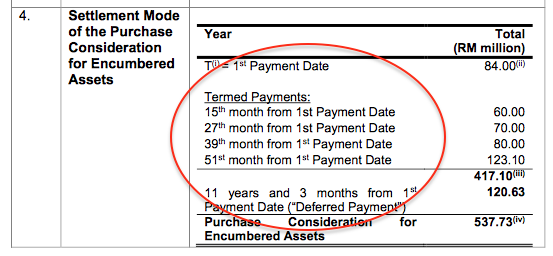

(c) Lion Industries is not paying the RM537 mil in one lump sum. The purchase consideration will be settled via several tranches as follows :-

Plesse note that the immediate payment would be RM84 mil + RM60 mil = RM144 mil only, to be paid within 15 months after acquisition. The rest will be paid over the next several years, with one dragging as far as 11 years.

In other words, Lion Industries is gaining access to RM1.84 billion assets by coming up with upfront payment of RM144 mil only (post 15 months, the Megasteel assets if profitable, should be able to stand on own feet and service the rest of the payment). Not a bad deal !!!

The payment structure is favorable to P&L as Lion Industries does not need to incur huge interest expenses.

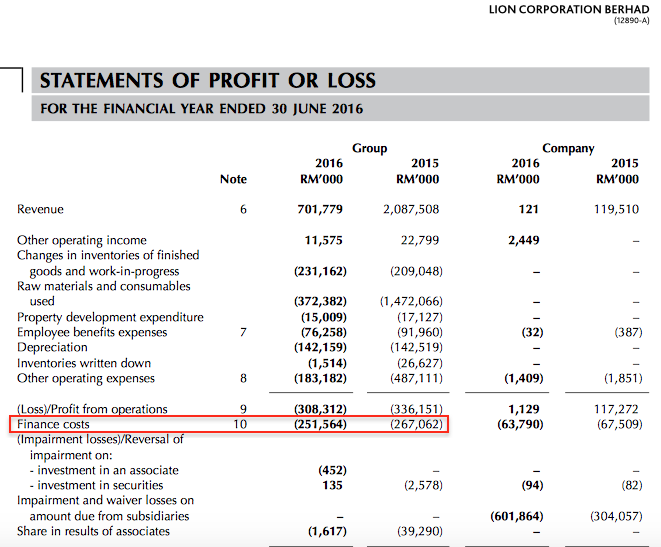

(d) As Lion Industries is acquiring the assets only, it will not have Lion Corp's burden of sevicing huge interest expenses amounted to more than RM250 mil per annum.

Concluding Remarks

In my opinion, the deal is structured quite favorably for Lion Industries. Compared to Lion Corp, Lion Industries will enjoy annual cost saving amounting to as much as RM354 mil due to reduction of depreciation charges by RM104 mil (my estimate / assumption) as well as absence of interest charges amounting to RM250 mil.

Notwithstanding the lower cost structure, there is another hurdle to cross - whether Lion Industries can make use of the assets to generate profit. That will depend on the prospects of the Malaysian flat steel industry. Due to lack of information, we can only find out when Megasteel started contributing (either positively or negatively) to Lion Industries bottomline in the future.

I am am not asking you to bet big big. But buy a bit to keep is no harm lah. No risk no gain.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

3 people like this. Showing 50 of 82 comments

Search for 'Lion group Midrex experience' pdf document in google:

(i could not paste the link here)

HDRI & HBI Production Capability at LION

The new Direct Reduced Iron Plant was built at the Megasteel

Facility in Banting, Selangor, Malaysia as shown in Figure 1. The

LION plant is based on the well-proven MEGAMOD® Shaft Furnace

with a 6.65 meter inside diameter and a proprietary MIDREX®

Reformer. All production is based on the use of imported iron

oxide.

The existing site has the capability of importing 2.5 Mpy

of iron oxide and transporting the HDRI and HBI products within

the Megasteel facility

Key Benefits

The increased supply of DRI will help to reduce the dependence

on scrap as a raw material for steel making by the Group’s various

steel mills and enable the production of high quality steel.

On site use of HDRI at high discharge temperature reduces

utility and maintenance costs (e.g., electrode and refractory costs)

and thus steel production costs. As an example, for a typical case,

hot charging at 600° C lowers operating costs $5-10/t liquid steel

and enables a 20 percent productivity increase. Figure 2 shows a

hot transport vessel.

Production of HBI allows continuous operation of the MIDREX

PLANT while other site operations might not be capable of

consuming HDRI as it is produced. Also, the HBI may be exported

safely, thus adding additional flexibility to the plant operation.

2018-07-04 19:30

http://www.theedgemarkets.com/article/megasteel-has-been-suffering-losses-due-excessive-dumping-steel-products

Lion Diversified said its wholly-owned subsidiary Lion DRI Sdn Bhd had also been similarly affected as Lion DRI supplies the "ENTIRE PRODUCTION" of hot direct reduced iron (DRI) to Megasteel as feedstock for the production of HRC.

2018-07-04 20:43

This is true. OTB's research was done well for his purpose.

======================================================================

Posted by Ooi Teik Bee > Jul 4, 2018 03:01 PM | Report Abuse

I do not think that I selected Lionind wrongly based on quarter result and net earning.

There is still strong growth in this stock.

To be fair to me, I do not know the buying of Megasteel assets without any insider information.

Blaming me to select this stock wrongly is not fair.

I also do my research, I talk facts and figures from Lionind financial report.

I cannot be right all the times, I expect to lose some.

I do not mind to lose some if I had done my homework thoroughly.

Thank you.

Ooi

2018-07-04 20:46

https://www.metalbulletin.com/Article/2213805/Lion-cuts-DRI-prices-to-Megasteel-by-19.html

June 01, 2009

Lion cuts DRI prices to Megasteel by $19

Malaysia's Lion Diversified has cut its direct reduction iron (DRI) prices by $19 per tonne as its sole off-take customer Megasteel has cut production.

Lion Diversified subsidiary Megasteel has been operating at "a reduced capacity" since November due to the "severe global economic downturn", said Lion. Lion's wholly owned subsidiary Lion DRI, which has a capacity of 1.54 million tpy, agreed in 2007 to sell all production of DRI and hot briquetted iron...

.......................................

Imagine if Megasteel, without any China dumping now could just save this 20 USD/ton now....

That itself translates to RM 80 / ton x 1.5 M tonnes HRC (say at half capacity) :

= 160 Million profit/ annum

That itself already pay back in 3 years...

Buying at PE 3 without any existing Net Margin assumption (zero) is considered cheap ma...

2018-07-04 20:51

I tell u what i think...

Megasteel will be able to payback in 12 months.

I think it will be able to export its HRC

2018-07-04 21:09

probability

over analyse, over think

share market not necessary to be like that....

share market is actually a much simpler game.

2018-07-04 21:14

If China can export HRC to U.S and Canada using Scrap based raw material.......

What so difficult for Megasteel using DRI as raw material and now with an edge over China to export to Canada?

2018-07-04 21:15

I can even grant you William C may have ambitions....

but none of his long term investors are satisfied customers.

2018-07-04 21:16

2008 - 2017 was the tsunami of China dumping....

I trust that WC could not have predicted such seismic activity.

2018-07-04 21:25

even this restructuring is a scam...paying 2 sen to a $1 for unsecured creditors.

and the assets land up in William C again.....and this is the best deal the bankers can get.

William C is a scammer....and share market no need to go to bed with scammers....it does not pay to go to bed with scammers.

2018-07-04 21:25

https://www.thestar.com.my/business/business-news/2016/04/15/megasteel-cleared-of-competition-act-infringement/

Megasteel had been operating under difficult environment due to the rampant importation of steel products into the country at dumping prices.

....................................................

China cannot afford to dump HRC price here in Malaysia anymore....as their raw material costs is too high - as they need to rely 100% on Scrap Steel which are highly priced in China.

They cannot source alternative raw material for their HRC making such as DRI made by DRI plants nor Pig Iron produced by Blast Firnace as subsititutes - as both these plants (DRI and Blast Furnace) have very high pollutant emissions.

All these boils down to China blue sky policy.

2018-07-04 23:25

probability

if you want to speculate on the future...and future businesses, I can off the fingers named a dozen or so better speculations than this william C and his stuffs which no self respecting fund manager will be interested.

2018-07-04 23:33

you can also copy this down...this low PE stock will soon be a high pe stock ( without the price going up) after next quarters results are published...and this new venture will take time to be profitable, if at all.

2018-07-04 23:39

The future of steel industry is not bright.....be careful...

KUALA LUMPUR (July 4): The Malaysian Iron and Steel Industry Federation (Misif) claims the industry would face an additional cost of RM100 million a year following the latest adjustment to the imbalance cost pass through (ICPT) announced by the Energy Commission last week.

The adjustment for the July to December period sees the removal of a 1.52 sen/kWh tariff rebate for all users in Peninsular Malaysia and a 1.20 sen/kWh tariff rebate for users in Sabah and Labuan.

....

http://www.theedgemarkets.com/article/steel-industry-faces-rm100m-additional-cost-following-icpt-adjustment-says-misif

2018-07-04 23:48

China steel might come pouring to Malaysia if Europe also implement tariff against China.....

Thyssenkrupp CEO tells Europe's lawmakers to protect the steel industry from China

Published 7:43 AM ET Mon, 2 July 2018

The CEO of a German industrial giant wants European lawmakers to help protect the steel industry.

Thyssenkrupp and India's Tata Steel signed a final agreement on Saturday to establish a steel joint venture.

Shares of both firms have struggled in 2018, given investor concern about steel oversupply.

The boss of German industrial giant Thyssenkrupp said lawmakers in Brussels need to protect Europe from an influx of cheap steel from Asian countries.

On June 1, 2018, the Trump administration imposed a 25 percent tariff on steel imports, and a 10 percent tariff on aluminum, from the European Union, Canada, and Mexico. This Friday, U.S. tariffs are to be imposed on $50 billion of Chinese goods.

.....

https://www.cnbc.com/2018/07/02/thyssenkrupp-hiesinger-tells-eu-to-protect-steel-industry-from-china.html

2018-07-04 23:54

The electricity tariff is going up..... This will impact Steel and Iron industry greatly...... The future for Lion Ind is not that bright.... This explain why Lion Ind stock price is dropping so much lately....

Misif: Electricity tariff hike will hamper industry recovery

Posted on 4 July 2018 - 08:59pm

PETALING JAYA: The Malaysian Iron and Steel Industry Federation (Misif) is calling for the government to consider maintaining the rebate and abolish the surcharge for the imbalance cost pass through mechanism, as the additional energy costs will hamper the industry’s recovery, which is just emerging from the doldrums.

It is also hoping the government will maintain the special industrial tariff for the industry over the next three years.

Misif said in a statement today that the net impact of the recent adjustment amounts to an increase of 2.87sen/KWhr or a drastic 8%-16% increase for industrial users.

.....

Refer to the link below for more details.

http://www.thesundaily.my/news/2018/07/04/misif-electricity-tariff-hike-will-hamper-industry-recovery

2018-07-05 00:00

Lion Ind future is not that bright..... seeing the making of HengYuan for Lion Ind... Donot trust the people who keep promoting the Lion Ind.... They want to leave now.... Be careful....

2018-07-05 00:12

Can India cross 1 mnt in DRI exports?

By 360 Editor - July 4, 2018

https://www.steel-360.com/stories/iron-ore/can-india-cross-1-mnt-in-dr...

In the light of fresh Induction furnace capacity expansions in neighbouring Nations and a considerable rise in ferrous scrap prices, exports of DRI also known as Sponge Iron from India has witnessed phenomenal rise over the last year,

rising by almost 85 % in 2017.

...............................

If current market trends are to be brought into consideration, there is a strong possibility that supply of DRI from India may well hit the 1 mnt mark over the next couple of years.

One of the key propelling factors for rise in overseas sales was the Bangladesh government’s decision to impose hefty import duty on billets. This compelled Bangladesh’s steel producers to maximize capacity utilization of the operating induction furnaces and to further augment capacity. This created a spike in demand for both scrap as well as DRI to feed growing Induction Furnaces.

The rise occurred in proportion with increase in global scrap prices and has since then remained more or less on the higher side. According to the current demand-supply dynamics there is a limited possibility of scrap prices declining in the next few years thus clearly indicating a strong market for DRI.

Global ferrous scrap deficit

...............................

With China maintaining its 40% duty on scrap export and strengthening efforts to consume domestically generated scrap through new EAF capacities the availability of Scrap in Asia has been constrained. To make matters worse, the recently imposed tariff on steel imports by the United States of America will push US steel generation, thus leading to higher scrap consumption.

This is expected to reduce scrap exports from the USA which has been one of key Global suppliers. These factors together may possibly create a significant deficit in demand and supply of scrap.

2018-07-05 00:59

I bet the Labuan plant is now operating at least:

at 90% of its rated capacity 850,000 MT/yr at 765,000 MT.

In 2017 it was only operating at half the capacity (quite easy to find this out)

2018 margin expanded by 80 USD/ton compared to 2017.

2018-07-05 01:05

I concentrate more on earnings, i still think going forward lionind can earn around at least 40-50million per quarter thou.

2018-07-05 09:37

Lion industries had fully impaired the entire RM699.1 million trade receivables and RM358.6 million other receivables from related parties in the previous financial year and as such would not have any further material impairment in the next financial year.

Based on reported on page 119 of the Annual Report 2017, the Group has trade receivables due from the following two major related parties, Megasteel and Lion DRI which have been fully impaired in the previous year. The amount due is approximately RM700 million in the book.

Megasteel is currently structuring a scheme of arrangement (“Scheme”) with its creditors to settle its outstanding debts. The outcome would only be known upon the implementation of the Scheme by Megasteel. The ability of Lion DRI to generate sufficient cash flows to repay its debts to

the Group is highly dependent on the Scheme of Megasteel.

Now, Lion Industries have proposed to acquire Megasteel assets and pay off its debts for total RM 638m. Such arrangement will allow Megasteel to raise cash through assets disposal at to Lionind. These scheme arrangement is important step for megasteel to monetize its assest, raise up cash and payback debt to lion industries.

In short, whatever lionind pay now cash RM 638m to megasteel to acquire its assets will eventually return back to lion industries as part of debt settlements. It will resulted significant writ-back GAIN reversal from earlier impairment provision, recover back amount owe by megasteel to lionind

2018-07-05 11:41

The Lion King is Blur Blur now!!!

Owing to the dusty n misty amosphere Here!

When will the dust settle?

wait till the trade war n mega mega steel project get clearer!!!

2018-07-05 11:46

The King of jungle will not b able to go far now!!!

These poachers r making too much damages here.

Talk east, talk west

talk right talk left

talk seven, then eight.

Real fuckers, get down to hell

2018-07-05 11:48

current hike electricity will affect steel company more, pls dont buy all steel company yet, until you see next quarter result how much the tariff hike affect them. my 2 cents

2018-07-05 13:54

Dear Mr

We refer to your appended email and wish to inform that the Proposals by LICB Group are purely for the purchase of the Flat Steel Assets without assuming any debts or liabilities of Megasteel. This will widen the LICB Group’s steel product base to include flat steel products that will strengthen its presence in the steel industry in Malaysia at a comparatively low investment cost.

LICB Group would like to reiterate that the Proposals are arm's length transactions negotiated by LICB. The Purchase Consideration for Encumbered Assets is RM537.73 million as compared to the net book value of the said assets of the vendor as at 30 June 2017 and 30 April 2018 of RM1,947.86 million (audited) and RM1,839.14 million (unaudited) respectively.

LICB believes that the Proposals are expected to contribute positively to the future earnings of the LICB Group.

Further, as stated in the announcement, Mercury Securities Sdn Bhd has been appointed to advise the non-interested shareholders by setting out their views on the Proposals in an Independent Advice Circular to be despatched to shareholders in due course pursuant to an Extraordinary General Meeting to be convened.

Thank you.

Yours Sincerely

for LION INDUSTRIES CORPORATION BERHAD

2018-07-05 17:19

http://www.adcommission.gov.au/cases/documents/069-VerificationReport-Exporter-MegaSteelSdnBhd.pdf

7.4 Arms length transactions

In respect of Megasteel’s domestic sales of HRC, we found no evidence that:

• there is any consideration payable for or in respect of the goods other than

their price; or

• the price is influenced by a commercial or other relationship between the

buyer, or an associate of the buyer, and the seller, or an associate of the

seller.

We therefore consider Megasteel’s domestic sales during the investigation period

were arms length transactions.

7.5 Volume and suitability of sales

Domestic sales cannot be used to establish normal values if the volume of domestic

sales is less than 5 per cent of the volume of comparable goods exported to

Australia. We compared the volume of Megasteel’s export sales of each type and

thickness category with comparable domestic sales over the investigation period.

The volume of domestic sales is more than 5 per cent of the volume of comparable

goods exported to Australia

7.6 Ordinary course of trade

We compared the unit invoice price paid for each domestic sale with the fully

absorbed CTMS those models for the corresponding month. We then compared the

selling prices of the loss making sales with the weighted average CTMS for the

investigation period to test whether some of those sales may be taken to be

recoverable within a reasonable period of time. We found that greater than XXX per

cent of Megasteel’s domestic sales of each type and thickness category were not

profitable and not recoverable over the investigation period. We therefore used only

the recoverable domestic sales of like goods to establish normal values.

7.7 Domestic sales – summary

We found a sufficient volume of sales in the domestic market that were arms length

and sold at prices that were in the ordinary course of trade. The price paid for the

goods in those domestic sales was established satisfactorily. Based on the

information provided by Megasteel, and the verification processes conducted on site,

we consider that prices paid in respect of domestic sales are suitable for assessing

normal value under s. 269TAC(1).

2018-07-06 00:16

11 DUMPING MARGIN

In calculating the dumping margin we used the date of sale/contract to compare each

export transaction with the corresponding normal value for the corresponding grade

of HRC. For three months there were no domestic sales in the ordinary course of

trade. In two of these instances we used the normal value from the following month

and made an adjustment based on the difference in the CTMS between these

months. For the third instance, we did not make an adjustment as the difference was

less than XXX per cent. These adjustment calculations can be found in the ‘Cost

Summary’ tab of Confidential Appendix 2.

We calculated a weight average product dumping margin of 15.45 per cent.

.......................................................................

2018-07-06 00:17

6.3.1 Raw materials

Megasteel’s cost of production spreadsheet shows the amount of scrap and HDRI

used in the production of molten steel. The categories of scrap and HDRI used in

the production are as follows:

Type Details

Hot dried reduction iron (HDRI) Sourced from related company Lion DRI Sdn Bhd

(Lion DRI). The Lion DRI plant is co-located with

Megasteel at the Banting site. It uses iron pellets

imported from Brazil as the main raw material for

the manufacture of HDRI.

Hot Briquetted Iron (HBI) HBI is a material produced when HDRI is cooled.

Megasteel sources HBI from Lion DRI and Antara

Steel Mill, both related companies.

Pig iron Pig iron is produced by blast furnace operations.

It is imported, mainly from the United Kingdom

and India.

Scrap Scrap is purchased in various forms such as

Heavy Melting Scrap (HMS), shredded scrap,

bundled scrap and bushelled scrap.

The various forms of scrap are added to the process in quantities determined by the

desired steel product in terms of tensile strength. Approximately XXX percent of

Megasteel’s molten steel requirements in the investigation period was provided by

the related company Amsteel. The average cost of the purchased molten steel in

the investigation period was XXXXX per MT compared to Megasteel’s own

production costs of XXXXX per MT over the same period.

Megasteel provided its scrap stock movement report for the selected month of May

2011 (confidential attachment COSTS 4). The report shows the volume and value

of the following for each type of scrap:

• Opening balance;

• Purchases during the month;

• Consumption during the month;

• Consumption for the month;

• Oxidisation losses; and

• Closing balance.

We selected two high usage forms of scrap (HRDI sourced from Lion DRI and HMS

sourced from independent suppliers) for further verification. Megasteel provided a

purchase voucher, receiving scrap reports, delivery reports and all invoices for the purchase of HDRI and HBI from Lion DRI in May 2011 (confidential attachment

COSTS 5).

The volumes and values on all documents match the May purchase

amounts in the scrap stock movement report. Both the HDRI and HBI were priced at

approximately XXXXX per MT in May 2011. Vouchers evidencing the payment to

Lion DRI for purchases of HDRI and HBI in May 2011 are at confidential

attachment COSTS 6. Megasteel’s accounts payable ledger for Lion DRI showing

the value of purchases and payments made by Megasteel (including for the

purchases made in May 2011) is at confidential attachment COSTS 7.

Megasteel advised that HDRI and HBI are purchased from Lion DRI at a price

XXXXXXXXXXXX per MT. We asked Megasteel to demonstrate that this price was a

reasonable market price.

Megasteel advised that Lion DRI and Megasteel are subsidiaries of separate public companies. Megasteel’s ultimate holding company is Lion Corporation Bhd and Lion DRI is a subsidiary of Lion Diversified Holding Bhd.

Megasteel advised that this dictated that all dealings between the entities was

required to be at arms length and on fully commercial terms.

Megasteel presented an off-take agreement it has with Lion DRI concerning the supply of raw materials. We copied the title page and the pricing formula confirming the purchase arrangements between Megasteel and Lion DRI

2018-07-06 00:21

https://www.thestar.com.my/business/business-news/2016/01/11/megasteels-serious-injury-cannot-be-linked-to-hrc-imports/

https://themalaysianreserve.com/2017/03/31/megasteel-to-benefit-from-anti-dumping-move-by-govt/

120 days was definitely not enough to allow Megasteel to show its true power...inventories of HRC consumers can last at least 40 days + deals would have been done earlier from their suppliers.

I certainly believe its ''prudent decision'' to buy these assets of Megasteel' i.e the HRC making plants by Lionind (as Hng33 correctly worded, they are not buying Megasteel)

Its impossible for China to dump here at current & future Scrap steel price.....

PH is here only for Malaysians.

2018-07-06 00:49

probability

for portfolio managers and stock market players....it is not smart to invest in companies whose survival depends on tariffs.....

portfolio managers and stock market players have more options than WC.

2018-07-06 01:16

This also means they can maximize Labuan, HBI production which has a rated capacity of 0.9 Million MT/yr

as we can see the Megasteel plant had been consuming it from the above article

2018-07-06 01:19

And now there are follow-on effects from the steel tariffs - https://www.reuters.com/article/us-usa-trade-eu-malmstrom/eu-says-first-steel-safeguard-measures-could-come-in-july-idUSKCN1J01Z6

2018-07-06 10:24

walao eh...didnt know there is Electrode plant in Banting!

https://themalaysianreserve.com/2017/03/31/sgls-banting-plant-to-be-electrodes-cathodes-asian-hub/

“The facility will act as our hub for graphite electrodes and cathodes and we will supply local and Asian customers from this facility.” SGL mainly sells electrodes in Malaysia in the region to clients from the steel making industry such as Lion Group, Perwaja Steel Sdn Bhd and Southern Steel Bhd that take up about 50% of the production capacity.

What more can u ask...

2018-07-06 16:52

Megasteel is not making money even with protected policy. Furthermore, Megasteel has huge debts to serve which will burn a lot of Lionind cash & future profits. What can Lionind do to make them back + profit?

2018-07-07 12:03

Posted by jakeT > Aug 21, 2018 05:24 PM | Report Abuse

Hi qqq3, just curious, when u mentioned fund managers would not even look at this stock, in your opinion, what would change their mind then? surely there must be some positive side for this company isn't it?

==========

its only my opinion.....u go find me an IB report on this William Cheng counter.......

2018-08-21 17:26

Parkson, I will dare to write, not so complex as this LionInd....

just curious....would any fund manager dare to touch this LionInd with all its complexity and uncertainties? and William cheng track record?

2018-08-21 17:38

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-26 15:15:00

ADX

5 Mins

BUY

2024-07-26 11:25:00

EMA 5

5 Mins

SELL

2024-07-26 11:20:00

OBV

10 Mins

SELL

2024-07-26 11:20:00

ADX

5 Mins

SELL

2024-07-26 11:05:00

EMA 5

5 Mins

BUY

Apps

Top Articles

1

2

BFM Podcast

3

MQ Market Updates

4

TA Sector Research

5

BFM Podcast

6

BFM Podcast

7

PublicInvest Research

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Ooi Teik Bee

Post removed.Why?

2018-07-04 18:23