Icon8888 Gossips About Stocks

(Icon) Success Transformer - Meets My Buy Criteria

Success is principally involved in manufacturing of transformers and lighting fixtures. It is a decent company with reasonable profit track record.

I bumped into it recently while scanning for undervalued stocks.

The reasons for buying :-

(a) the stock is currently trading at multi-year low;

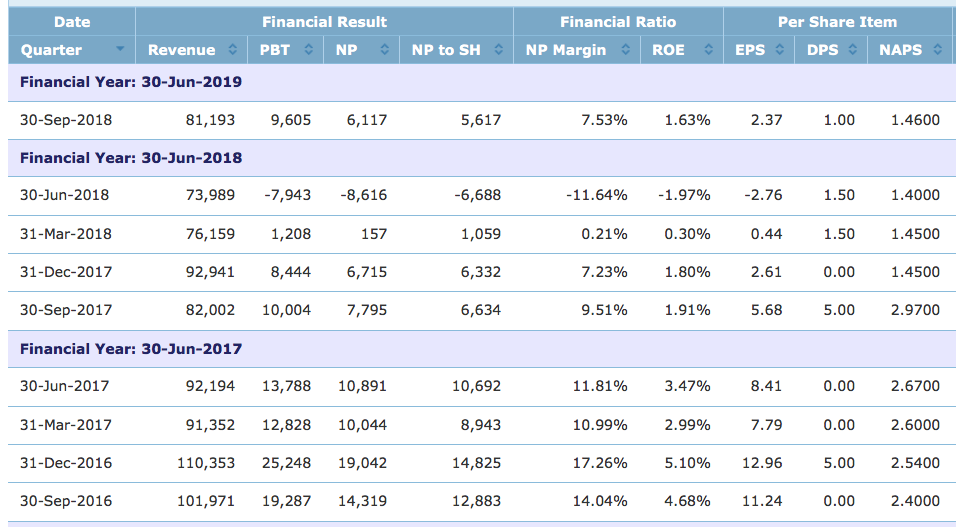

(b) reported EPS of 2.37 sen in September 2018 quarter. Based on annualised EPS of 9.5 sen and 55 sen market price, prospective PER is 5.8 times;

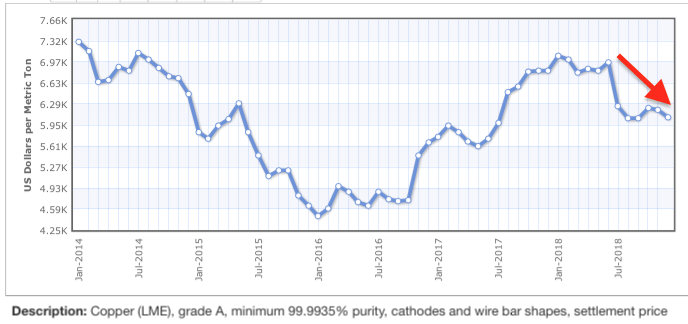

(c) copper price has declined by 15% since mid 2018. Success uses copper for its transformers;

(d) Strong balance sheets. Based on shareholders' funds of RM315 mil, borrowings of RM56 mil, cash and equivalent of RM50 mil, net borrowing and net gearing is RM6 mil and 2% respectively only.

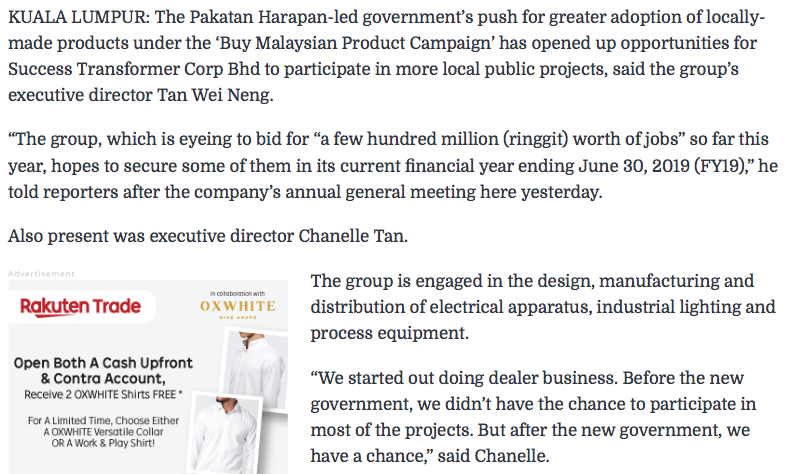

(e) Positive guidance by management recently. Please refer to article below.

Take a look. Don't worry, I won't pump and dump you.

Have a prosperous Chinese New Year !!!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Icon8888 Gossips About Stocks

(Icon) Jaks Resources - IRR Model Shows That RM300 mil Net Profit p.a. For 30% Stake Is Plausible

Created by Icon8888 | May 01, 2020

(Icon) Notion VTec - Forget About The Virus, It Is Time To Rock and Roll

Created by Icon8888 | Mar 10, 2020

(Icon) Sam Engineering - Excellent Result. Share Price Can Potentially Double Within 2 Years

Created by Icon8888 | Mar 01, 2020

(Icon) Alliance Bank - One Off Provision Affected Previous Quarter Earning. Time To Buy On Weakness

Created by Icon8888 | Nov 13, 2019

Discussions

2 people like this. Showing 45 of 45 comments

aunty where is my seaweed keropok!

Go back kitchen make, dont come market and lose your retirement money!

I'll pay RM20 for one tin!

2019-02-01 14:08

buying a share at multiple year low with hope in business recovery is a perfect contrarian stock.........

more potential rewards and makes better sense than the Insas players.........or Puncak players.....

me? The trader in me cannot find a reason to buy....the newly discovered "only the best" in me cannot invest....so its a non starter for me.....I don't have such a huge capital.

I want to focus.

2019-02-01 14:09

If the earnings come back should be ok gua. Business looks moatless, but it looks cheap enough, but im not sure its that great of an investment versus others cos now.

2.5% or less ok lah.

2019-02-01 14:13

a lot of multiple year low stocks....no wonder Icon has become a contrarian.....

good hunting ground.

each one 1% can buy 100 of these.

2019-02-01 14:17

I like their lighting business. You can say they are the equivalent of IQGROUP for infrastructure projects. However, earnings are quite volatile.

2019-02-01 14:19

soojinhou,

How does their lighting business compare versus the competitors. Any particular moat, or just another supplier in the industry?

2019-02-01 14:45

(b) reported EPS of 2.37 sen in September 2018 quarter. Based on annualised EPS of 9.5 sen and 55 sen market price, prospective PER is 5.8 times.

If based on previous annualised EPS of negative -2.76 sen, this counter worth -2.76 sen x 4 x 10PE= -1.10? You cannot just simply using latest EPS then multiply with 4, right?

2019-02-01 15:09

Yes you can count like that also. Then the conclusion is don’t buy loh

I am not trying to convince you to buy

2019-02-01 15:11

Posted by probability > Feb 1, 2019 03:09 PM | Report Abuse

have a feeling..after all the warren buffet bull shit theories...people are going to realize there is no such thing as moat in the current business world...

every technology, IP and skills (including heavy manufacturing industry)...are going to be easily replicable....and the world has to adopt free & open cross border competition...

this is the struggle between U.S & China currently...

...........................................

what is most important - constant adaptations to market expectations...flexibility...

this could be the 'hidden moat'....

======================================

this post I can 100% agree.......

2019-02-01 15:12

Thanks for remind me back this forgotten counter. Current commodity price environment-yes. Price at multiyears low-yes. Technical wise-mixed. I think the best time to buy is after coming q. From technical point of view, I prefer Fitters' chart.

2019-02-01 15:32

Brother probability,

Moat does not mean you wont die during a disruption, but harder to die, and may even thrive.

Lets say now, very simple. Retail apocalypse. Because of Amazon and online retailing, all the shopping malls and retail companies in the US dying.

SEARS from 40 dollar a share to 20 cents, now almost bankrupt.

Parkson from RM8.81 to RM0.22.

UK, Nordstrom etc all dying.

Whatever moat these companies had, was great no doubt, but it wasn't a true moat. In the end, get murder by a structural change initiated by the emergence of Amazon.

But then, not all retail companies die.

COSTCO, a wholesale grocery business, this year, profit and revenue up 4%. And it has growing like that for the last 20 years.

Share price for USD50 in 2008 to USD215 today.

Why?

Because COSTCO is a true wonderful business with a moat. Let me explain to you this co.

What is a wonderful business? How does a moat sustain for decades?

First, it needs to be the standard good business in great industries, that has a certain structural edge etc..

But the key thing for a moat is, it needs to be WONDERFUL for society. You need to tie your profitability to benefit towards society to such an extent that, the more money you make, the better off it is for society.

COSTCO is a wholesaler, can buy your nestle, coca cola, groceries there, just need to buy higher volume.

Last year, they made USD3 billion or so. Except, this consist wholly of their USD50 yearly membership card. They make ZERO, KOSONG, NOTHING from selling groceries.

Here is what they are telling their customers. Every year, we will only make USD50 dollars in profit from you, regardless of how much you buy. You spend 10 million with us? We only make 50 dollar. You spend USD20k? We make USD50 from you only.

And this company has one of the lowest cost base in the industry, and is completely focused on cutting cost.

They got no name tag. Just sticker with your name. Uniform? Bring yourself, black shirt, slacks and shoes.

When coca cola try to increase selling price by 5 cents per bottle, they completely refuse to stock coca cola, telling their customers, they feel coca cola does not provide enough value for them to sell it to their customers.

Coca cola buckled and didnt increase the price.

If this company next year makes US10 billion instead of USD3 billion. One can argue that they have tripled the benefit they contributed to american society.

That is a moat.

Look through that lens when finding companies to buy in malaysia. Got one or two such companies in bursa. :)

======

Posted by probability > Feb 1, 2019 03:09 PM | Report Abuse

have a feeling..after all the warren buffet bull shit theories...people are going to realize there is no such thing as moat in the current business world...

every technology, IP and skills (including heavy manufacturing industry)...are going to be easily replicable....and the world has to adopt free & open cross border competition...

this is the struggle between U.S & China currently...

2019-02-01 15:50

sorry they increased card prices. They increase card prices every 5 or si years.

Got 2 tier, USD60 for standard. USD120 for companies. Renewal rates is higher than 90% per annum.

2019-02-01 15:57

bear market victim.....this is one of many such bear market victims......Its wrong to think it is rare or exceptional.

2018 small cap bear market hits all of them , without exception. Smart are those who avoided huge losses in the down period......

2019-02-01 16:02

soojinhou,

How does their lighting business compare versus the competitors. Any particular moat, or just another supplier in the industry?

Their lighting is supposed to be smart, and therefore energy saving. For example, the light brightens when a car approaches and then communicate the information to the next light. It is IOT based and smart, and so it's controllable via computer. IQGROUP's Lumiqs is also based on similar concept but they are targeting industrial customers, such as those used in warehouses, rather than infrastructure like Success. As for a moat? Well, given enough money and motivation, most engineering can come out with similar solutions. But given Success is the incumbent and has established a portfolio of projects, they are harder to unseat by competitors. In the end, it's ultimately cost vs benefit. Are councils or property owners willing to pay more for smarter lighting, or just go for cheap dumb lights?

2019-02-02 09:25

Lego belum siap pasang now u want seaweed keropok???

swear to god not gonna go back to the kitchen where i pocketed my first million......

anyway wish all of u here (included my son John England) a prosperous CNY, more huat than pig head.

=============================================================

Posted by Choivo Capital > Feb 1, 2019 02:08 PM | Report Abuse

aunty where is my seaweed keropok!

Go back kitchen make, dont come market and lose your retirement money!

I'll pay RM20 for one tin!

2019-02-02 10:44

when revenue keeps dropping share price will definitely be at multi-year low.

its normal

if nothing changes 2019 revenue will drop more

2019-02-03 11:20

I also look for undervalued company to buy, thus I looked into Success' latest quarterly and annual report to find out more after reading Icon's article above.

My findings are :

- The core EPS in FY2018 (ended Jun'18) was 5.3sen. At 53.5sen per share now, Success is selling at PE = 10.1x which is not cheap nor high.

- However, if i use this Q1FY19's reported EPS of 2.37sen to annualise, i get 9.48sen/year. This translates to PE = 5.6x which is attractive.

- But, i noticed that Success's quarterly earnings is inconsistent, this means we may see much lower or higher EPS in subsequent Qs...As such, predicting next Qs' EPS using Q1FY19's reported EPS is not reliable.

2019-02-03 15:31

The main concern for Success is its Process Engineering segment which suffered losses in FY18, and management anticipates still challenging prospect for this segment in FY2019.

In addition, Success exports >50% of its product to overseas, and therefore, favours weak RM but RM is strengthening against USD now.

2019-02-03 15:32

Based on the above findings, i think i will leave Success for now and put it in KIV list.

2019-02-03 15:34

To be honest, I have bought the qps automatic voltage stabilizer ( different from capbank) from success, especially for easy Malaysia projects where the voltage sometimes fruits from 240v to 200v and 415v do to 360. It helps out alot.

However, ever since my purchasing team found alibaba, we have been taking our sales of Nikkon street lights and avs systems for refineries directly from China. Especially as these items do not require sirim or have government control requirements.

Their prices especially are more expensive than China, and unable to compete in terms of low cost assembly efficiency, and bulk raw materials costs.

For me business competitive advantage is everything. I don't see success transformer to be able to grow their products exports significantly.

The is no major tax break from mida for parents products like vitrox.

The products sold is very standardised in market and commodities.

Lighting industries are very sad. Just ask iq-group what happened to their business.

Moat is basically a word to describe why you would buy the products the company produces.

Is it the cheapest in the market? No. QTC Thailand is far cheaper. We buy from them.

Is it the best in the market? No. Megaman is. Or osram, even Phillips.

Is there a local requirement that requires qps product? No. Sirim unneeded. Many hospitals use China brand. In fact Nikkon lighting Mahal.

Is there management excellent? I leave it up to you to decide.

Is the management shareholder aligned? This at least his my criteria.

Has the revenues grown in last five years? Nope.

Has the profits grown in last five years? Nope.

Is it undervalued? Yes, dearly.

Will it do well in the future? The business has hit terminal growth. What you are getting is simply minimal growth yearly.

Is it a good buy? I guess.

>>>>>>

Moat is overrated

2019-02-03 16:06

philip...if analysts put on your thinking cap....analysts and sifus no more job already.....

the job of analysts and sifus is to convince u to take money from your pocket and put into their pocket , its also called commissions.

and ideas is the SOP and the KPI, not the customers well being....that is well known enough.

my analysts son KPI is the number of reports he churns out, not the accuracy of his reports........

2019-02-03 17:48

Yeah if you tell everyone 99% of the time stocks in bursa is rubbish, I think your son won't be able to keep his job for long. Sad but true.

2019-02-03 18:20

(S = Qr) Philip > Feb 3, 2019 06:20 PM | Report Abuse

Yeah if you tell everyone 99% of the time stocks in bursa is rubbish, I think your son won't be able to keep his job for long. Sad but true.

==========

hahahaha...sifus also at risk....

2019-02-03 18:28

Phillips overtook qqq3 in i3 rank. With substance. Qqq3 as usual without substance can retired for good

2019-02-03 18:50

icon looks like you have lost your touch after coming in at the bottom of 2018 i3 stock competition...you want play undervalued cos go ask calvintaneng.

just focus on your area of competence...finding growth stocks.

i like to see how you perform against s=qr....hahaha

2019-02-03 18:53

That one actually is introduced to me by qqq3.

It is the mathematical formula for success.

Success = q( your ability to execute )*r( the value of your idea)

Basically in stocks, how well you do depends on your ability to have a great idea, then how will you execute on your idea.

So if you had a great idea to invest in hartalega in 2009, but you only bought 10 lots, you don't get to be successful.

But if like kyy had a mediocre idea in liihen, but he sailang, he still success.

Imagine if he sailang all the way in Amazon 2009, he would have been a monster!

2019-02-03 19:37

s=qr with 403 posts made 10 times more impact to i3 than 3iii with 4930 posts.

2019-02-03 20:10

s= Q r....... that I did not copy from Philips.... u can check whose thread appears first.

2019-02-03 20:11

I am extremely grateful of 3iii's comment below. Finally somebody gives me due recognition instead of baseless accusation of pump and dump

==============

3iii So far, I have come across 3 people in this forum who have been honest with their postings with good intention for the good of all:

1. Mr 1015

2. Icon

3. KC

Another remains unnamed but not difficult to guess on.

03/02/2019 20:01

2019-02-04 11:25

Sounds easily replicated to me tbh.

Probably undervalued, can consider 1-1.5% of portfolio i guess. But with market this good, they are so many wonderful companies at similar valuations.

Making it harder to swallow.

====

Posted by soojinhou > Feb 2, 2019 09:25 AM | Report Abuse

soojinhou,

How does their lighting business compare versus the competitors. Any particular moat, or just another supplier in the industry?

Their lighting is supposed to be smart, and therefore energy saving. For example, the light brightens when a car approaches and then communicate the information to the next light. It is IOT based and smart, and so it's controllable via computer. IQGROUP's Lumiqs is also based on similar concept but they are targeting industrial customers, such as those used in warehouses, rather than infrastructure like Success. As for a moat? Well, given enough money and motivation, most engineering can come out with similar solutions. But given Success is the incumbent and has established a portfolio of projects, they are harder to unseat by competitors. In the end, it's ultimately cost vs benefit. Are councils or property owners willing to pay more for smarter lighting, or just go for cheap dumb lights?

2019-02-04 11:29

And then it reverts back to mean, going back from 0.50 cents to 0.7 cents, for a 20 cents gain. Pretty much a good buy I guess.

I just ordered another 2 sets of qps voltage stabilizers for factories to combat unstable voltage in tawau.

Congrats icon. 20 cents gain is impressive. Hopefully it can fully uptrend been to its original price of rm1 few years ago.

I wonder how many of choivo stocks returned 30% recently?

2019-03-02 22:11

,S = =Q r is the best summary in the world..... keep in mind..... best don't need to be most complicated

2019-03-02 22:53

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-03 16:50:00

ADX

10 Mins

BUY

2025-01-03 16:40:00

TURTLE SYSTEM 55

10 Mins

BUY

2025-01-03 16:40:00

TURTLE SYSTEM 55

5 Mins

BUY

2025-01-03 16:30:00

TURTLE SYSTEM 20

30 Mins

BUY

2025-01-03 16:30:00

TURTLE SYSTEM 55

30 Mins

BUY

Apps

Top Articles

1

CEO Morning Brief

2

3

Good Articles to Share

4

Good Articles to Share

Jim Cramer talks companies investors should be cautious of in 2025

5

Good Articles to Share

Jim Cramer talks being cautious with nuclear power and quantum computing stocks

6

Good Articles to Share

Newt Gingrich praises Mike Johnson for patience and calmness

7

Good Articles to Share

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Connie555

HAHAHAHAHAHAHAHA Don't don't don't simply dump things like ah jon dump his lego around the house, aunty Connie step on it also buay tahan the pain, later u dump me stock summore i buay tahan the mentally pain of my money gone.....

Aunty Connie wish u huat huat.

======================================================================

Take a look. Don't worry, I won't pump and dump you.

2019-02-01 14:02