Choivo Capital

(CHOIVO CAPITAL) The valuation of financial institutions. And why Coldeye is wrong on MBSB

Choivo Capital

Publish date: Sun, 31 Dec 2017, 04:33 AM

Note: The pictures in this blog didnt come out right, refer to this link for the spreadsheet of the pictures, or open the pictures in a new tab.

https://docs.google.com/spreadsheets/d/1m-TarfVVci6X7GjnovZ1-J59ac2u8xnwZCmx-EcOWOE/edit?usp=sharing

Introduction

In general, most companies fall into 3 categories when it comes to valuations. They are

1. Any company other than those in the other 2 category.

2. Banks and Non Deposit Taking Financial Institutions.

3. Insurance companies.

For companies in category one, one can pretty much use the full spectrum of quantitative analytical tools. P/E, EV/EBIT, EV/EBITDA, EV/FCF, DCF. Can count until the cows come home if you want.

For banks and insurance companies however, you need different tools.

Insurance companies is easily the most complicated one. There is "Combined Ratio", "Insurance Float" and "Cost of Float". All of which you need to slowly extract one by one from the annual reports, and that's why most screeners do not show it.

Personally, i've not had the time or motivation to really look at it yet. As this article will be about the valuations of banks, i won’t be going any further on insurance companies.

I will however state that, out of all the listed insurance companies in Malaysia, only TUNEPRO and LPI actually make consistently money on the premiums. Every other company loses money on the premium, but make it back via investment income. I don't hold shares in either, but feel free to study further.

Ok, lets now start with how to value banks and non deposit taking financial institutions.

Why is bank valuations different?

1. Whats wrong with P/E

Well, you can, but banks have a very interesting relationship with P/E.

The thing about banks is that their business consist wholly of cash, their product is cash, their asset is the cash they borrow people, and their liabilities is the cash people borrow them or deposit with them.

This means that it would be incredibly foolish to pay, for example, 30 P/E for a bank. As they are all in saturated markets, making it impossible to grow quickly, unless one were to take on risky derivatives, or loan out money not caring about the borrower’s ability to repay.

It is also not possible leverage up quickly via deposits without severely affecting cost of capital, as higher deposit rates are required. Banks in Malaysia are already at the edge with something like 0.9-1.7% net interest margin.

Nor is it possible to source too much funds from the bond markets. First off, bond funding is usually more expensive than deposits, and banking is all about management of cashflow.

Bonds often have covenants that may result in instant recall, thereby really screwing over your cash flow, it is also not easy to structure your bond to fit your cashflow schedule and requirements.

What im trying to say is, banks will find it close to impossible to record the double digits growth needed to justify P/E's above 15 due to the saturated markets, they may try to rack up the leverage or risk they are willing to bear to get that higher earnings, but that is also very difficult as banks are very tightly regulated.

Even if they were not tightly regulated, the higher the risk/leverage they are willing to bear, the higher the probability of bankruptcy. Yes, you make more short term wise, but it’s easier to go bankrupt, and these 2 set off against each other valuation wise (logically, but markets are not logical).

The only exception is when kitchen sinking is being done, so there is a depression of earnings beforehand, keeping valuations down. Like MBSB. Except in MBSB’s case, where valuations are not really down either.

Funny story.

Early 2007, Warren Buffet was one of the biggest shareholders of the bank "Fannie Mae". When the CEO said that the bank were targeting for double digit growth in revenue and profit, Warren immediately started dumping the stock and was completely out by 2008.

The company, using CDO's and derivatives, as well as incresed leverage, met its target of double digit growth in 2008. It also went bankrupt during the financial crisis of 2008 and was one of the banks bought out by the government to prevent a meltdown in the financial markets.

2. How about EV/EBIT?

Also known as earnings yield, or as Joel Greenblatt likes to call it, the magic formula that beats the market (Do note it beat the market then, now that everyone knows and since markets are a dynamic environement, that stament may no longer hold true moving forward).

What is EV or Enterprise Value? EV is the real cost of the company if you were to buy outright. In essence it is:

Enterprise Value = Market Capitalization + Borrowings + Minority Interest – Cash and Cash equivalents.

Except in banks, all their liabilities is borrowings, and all their asset is cash and cash equivalents. Do the calculation and you basically get back your Equity.

How about EBIT? Also known as Earnings before Interest and Tax.

All your expense is interest expense and all your earning is interest income wor. Habis. Count so hard, get back zero. Again irrelevant.

How to Value?

Banks are incredibly complex, with multiple products and segments etc etc. It is close to impossible to do a proper detailed analysis even if you're the analyst covering it. The only time a proper one is done, is when there is a M&A going on.

However, this does not mean it is impossible. We can still do a rough, rule of thumb valaution. How?

Let’s try asking warren buffet.

“Well, a bank that earns 1.3% or 1.4% on assets is going to end up selling above tangible book value. If it's earning 0.6% or 0.5% on asset it's not going to sell. Book value is not key to valuing banks. Earnings are key to valuing banks. Now, it translates to book value to some extent because you're required to hold a certain amount of tangible equity compared to the assets you have. But you've got banks like Wells Fargo and USB that earn very high returns on assets, and they at a good price to tangible book. You've got other banks ... that are earning lower returns on tangible assets, and they're going to sell -- they're going to sell for less”

“Banks are not going to earn as good a return on equity in the future as they did five years ago. Their leverage is being restrained for good reason in many cases. So, banks earn on assets but the ratio of assets to equity, the leverage they have determines what they earn on equity.”

If you lazy to read, what he is saying here is this.

For banks the key thing is a high Return on Asset (ROA), something above 1% shows that your asset is valuable and thus worth more. It does not look like much, but since most banks are very leveraged, that 1% usually translate into a much higher Return on Equity (ROE).

Your ROA is in turn linked to your book value. The higher your ROA, the more valuable your asset, and the higher the “Price to Book” (P/B) multiple people are willing to pay.

In general, an asset with a ROA of 1% should be valued at 1 times Price to Book.

Except, that's not the end of it.

Because in investing, I’m not buying the asset, I’m buying the company. This means what I’m interested in, is the ROE not ROA.

If a bank has zero leverage, and the ROA is 1%. Using the previous rule of thumb, if I were to buy the bank at 1 times P/B, I would be buying a company with 1% ROE, and will be effectively valuing it at 100P/E, which is insane.

This means leverage is key. If the bank is leveraged 10 times instead. That 1% ROA, translates to 11% ROE. This means i'm paying a P/E of 9 times, much more reasonable.

Which gives rise to this rule of thumb. I came up with this on my own, i dont seem to read it anywhere else.

“The fair value of a bank with ROA of 1% and leverage of 10 times, is worth a multiple of 1X Book value”.

Except, it still isnt the end of it!

Because this rule of thumb does not price in the risk of bankruptcy due to leverage. And this can give rise to some pretty interesting edge cases.

One thing to note about banks is the method of recognition of liabilities and assets.

Liabilities : Marked to Cost.

What the bank owe, the bank must pay. This figure is absolutely fixed and set in stone.

Assets : Marked to Market.

Whatever asset the bank has, its value depends on what the market will pay. Ie, it fluctuates. Due to leverage, if it drops low enough, a bank can go bankrupt. Similar to margin call.

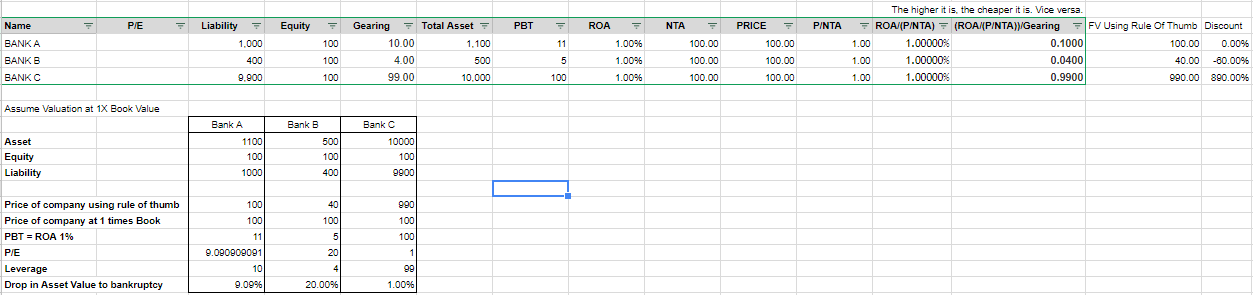

Lets Imagine Bank A, Bank B and Bank C.

Bank A

The bank has ROA of 1% and is leveraged 10 times. If an investor pays the 1X book value or RM100, he gets a company at a P/E of 9.1 and ROE of 11%. The bank is also very unlikely to go bankrupt as asset values would need to fall 10%, which is very unlikely. Pretty fair deal.

Bank B

Bank B is exactly the same as Bank A, except it is only leveraged 4 times instead of 10 times. In this case, using the rule of thumb to calculate fair value, the fair value of the bank is only RM40 despite book value being RM100, with the same exact level of quality as Bank A's.

For this bank to go bankrupt, asset values need to fall by at least 25%, a drop which was only almost achieved for some banks in the 2008 crisis.

Therefore, by being prudential and conservative, so much so that this bank would actually survive the 2008 crisis comfortably, the market punishes it by valuing its assets (which is just as valuable as Bank A's) at 0.4 times book value instead of 1X.

Bank C

Now, Bank C is in every way the same as Bank A and Bank B. Except, at this bank, the CEO has got balls like Donald Trump. His balls literally clicks when he walks.

This bank has a leverage of a whopping 99 times. Absolutely insane. A mere 1% drop in asset value, and the bank will go bankrupt.

If one were to pay the book value for this bank, ie; RM100, the P/E will be 0.9. By this metric, it is even cheaper than Hengyuan that was at RM2 during the start of the year.

Therefore, using the rule of thumb fair value, this bank should be worth RM990. IE, You should pay roughly 9.9 times book value for a company that can go bankrupt tomorrow. Insane.

Now, do you know what i mean when i say the valuation of banks is very interesting, and why M&A of banks take so long, valuation is hard.

Conclusion

There must be a balance, a bank cannot do business as if they must survive 2008, or it would be very hard to make money. On the other hand, they also cannot go crazy and leverage up to the moon.

Pre 2008, leverage in banks was in high teens, now it has dropped to roughly 10 times. Seems pretty balanced.

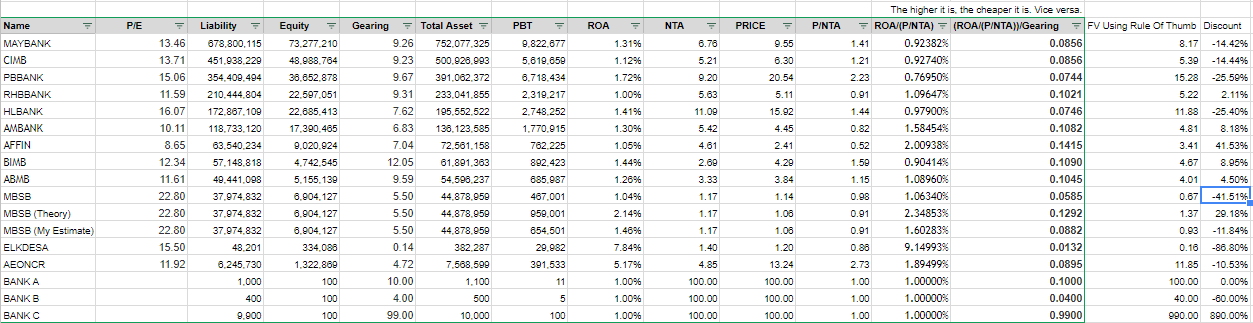

Rule of thumb table for all banks in malaysia

As it is christmas after all, i decided to give a present to I3 for all the information it has given to me this year.

Here is a valuation table i made for all banks in malaysia approximately 3-4 months ago. The data is not updated, but its a fairly decent reference. Some financial institutions are not included in this table as they are my favourite. Not going to give those away for free.

Looking at this table, we can see that Affin is the most undervalued bank and Public Bank is the most highly valued bank in malaysia. And, MBSB is by far the most overvalued one.

And for good reason, in the case of Public Bank, you are paying not just for their high quality asset (highest in malaysia at 1.72% ROA). But also for Teh Hong Piow, the fantastic management, the amazing culture and the incredible track record.

Affin on the other hand, not that great of a bank, one of the smaller ones in malaysia. Management is not great, and it shows, severely undervalued. Also leverage is not that high, which means, the potential is there somewhat. I hold a very small 2% position in Affin. I can't help buying a little as it is very cheap. If it touches around RM3 given the current fundamentals, im out.

Other salient qualititative points about banks as an investment

1) In banks, as the product is cash and everything is cash. It is very unlikely that bad allocation of capital will be done. You will not see PPE purchases that turn out to be a waste of money, or money being spent to buy assets that are not being used and just held in the books. Capital is usually used very efficiently in the markets.

2) Bank earnings are generally, more stable, and not subject to sudden upwards or downwards swings. Unless the bank loaned money to places where it shouldnt be loaned.

For example, in 2013, there was record earnings all round for banks, as the banks were loaning money left right centre to oil and gas companies.

Come 2014, 2015 and to an extent 2016, impairments left right centre. Due to the fall in oil prices, and all these oil companies being unable to pay back the loan.

Only one bank stayed out of that foolishness. The one and only Public Bank. And like clockwork, every quarter, revenue and earnings is up around 2-5%. The last time they had a red quarter (drop in earnings or revenue), was in 2008 during the peak of the financial crisis, and only once. Incredible.

Why i think Coldeye is wrong on MBSB.

For the last 1-2 years, Coldeye or "Fong Siling" have been pushing MBSB as his favourite. And he has put his money where his mouth is. Coldeye holds 13,300,000 shares in MBSB or 0.23% of the company. I have no doubt this is probably his largest position at roughly RM13.8 million.

This year, one of our veteran stockpickers ICON8888 have also chosen this stock as one of his favourite for 2018.

Allow me to (arrogantly) say why i think they are making a mistake. Feel free to correct me if you feel i have made a mistake, mispricing whatever risk or gains, or coming at it from a wrong perspective. I too like to make money, if im wrong, then im happy, cause i can buy some now.

Looking at the table above (Look at "MBSB"), at current ROA and leverage, the fair value of MBSB is actually RM0.67 compared to the RM1.04 as at 29 December 2017. This means it has about 35% more to drop before reaching fair value.

Except, it isnt so simple. According to management, the reason why earnings are so low, is due kitchen-sinking of impariment charges for the last 1-2 years to bring their provision standards in line with a typical bank in malaysia.

According to management, Impairment for the last 13 quarters total RM2.14 billion. Impairment relating to the exercise amount to RM1.6 billion.

What the management is saying here, is basically, if not for the impairment exercise, our profit will be higher. By how much then. Well taking RM1.6 billion divided by the number of quarters, that is approximately RM123 mil per quarter, or RM 492 million extra in earnings.

Now, if you think this management is 100% honest, no incentive to fry up price or make themselves look good, and like god, estimates is 100% correct.

We should then add back the RM492 million into the rolling earnings (look at "MBSB (Theory)"), the fair value now shoots up to RM1.37. This means MBSB is undervalued by RM0.33 or 24% compared to current market price. Now its definitely looking like a decent buy.

Except, what the management is also telling from that statement above, is that actual operating impairment is only RM540 million for 13 quarters, which is RM39.5 million per quarter RM158 million per year.

Given that MBSB asset size is RM44.9 billion, that transalates to an impairment rate of only 0.35%. For the record, Maybank's is roughly 0.5%.

Except, here is the kicker. Out of MBSB's RM44.9 billion net asset/loan portfolio, roughly RM22.6 billion are in the personal loan space.

As it is riskier, personal loans offer far higher effective interest rates compared to say a car loan or housing loan (Effective interest rates for personal loans are on average 20% (RCECAP and AEONCR), compared to 4-5% for a car (brand new) or housing loan). Therefore, most personal loan companies have far higher impairment rates. RCECAP for example, one of the better run personal loan companies, have an impairment rate of 1.56%.

RCECAP and MBSB are very similar companies. For both of the, loan repayments are done via salary deductions. So this should mean less non-performing loans and therefore a lower impairment rate.

With the above in mind, I think MBSB's management estimate of the impairment rate of 0.35% is far too low.

Now, using RCECAP's impairment rate of the personal loan portion of the portfolio and Maybank's for the rest.

((RM22.6bil*1.56%)+(RM22.3bil*0.5))/RM44.9bil = 1.03%

MBSB's impairment should be somewhere near 1.03%. This transalates to roughly RM462.5 million per year for impairments, compared to the management estimate of RM158 million.

Plugging that into my table (refer to "MBSB(My Estimate)" the fair value of MBSB, assuming that my estimate of the future is perfect and i am god. Fair value of MBSB is only RM0.93. Ie, overpriced.

Assumptions where i could have gone wrong.

1) For most loans, housing or motor, MBSB still takes back the money via salary deduction, so the impairment rate may very well be lower than Maybanks.

Conclusion

Fair value for a bank is roughly 10PE. But make sure you take into account leverage. 15 times is the absolute maximum for a sane investor, most banks are at 10 times. Asset quality means more than leverage when it comes to source of earnings.

====================================================================

Facebook: Choivo Capital

Website: www.choivocapital.com

Email: choivocapital@gmail.com

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Choivo Capital

(CHOIVO CAPITAL) MYNEWS (5275) – Dr CU in da house. 66% Upside

Created by Choivo Capital | Dec 09, 2020

(CHOIVO CAPITAL) WCE (3565) – When the roads align. 562% Upside.

Created by Choivo Capital | Dec 05, 2020

(CHOIVO CAPITAL) BAT (4162) - Budget 2021 (The Dark Knight Rises)

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) LIONIND (4235) - Budget 2021, Rising Steel Prices

Created by Choivo Capital | Nov 09, 2020

(CHOIVO CAPITAL) KRONO (0176) - Is it Alibaba (Alibaba Cloud)? (SUMMARY)

Created by Choivo Capital | Nov 03, 2020

Discussions

15 people like this. Showing 45 of 45 comments

Liquidity crunch was the main reason in the last financial crisis that made some banks go bust or almost bust.

With Basel III kicking in, more emphasis is placed on liquidity (refer Liquidity Coverage Ratio or LCR) and capital buffer for the banks to withstand during crisis times.

These days, central banks no longer look at the Bank's Loan to Deposit Ratio, it is the LCR.

2017-12-31 10:53

Cold eye definitely buy below myr1.00 .. not a loss for him at current price..

2017-12-31 11:05

as regulatory requires the banks to set aside additional capital requirements, the bank's ROE suffers as a consequence. though ROE is still the key metric to look at in assessing the bank's performances including the credit rating agency, return on risk weighted assets is the more accurate assessment.

valuation wise, the implied P/BV would seems higher in view of declining ROE...hence the investment community may revisit the assumptions in valuing the banks, the average P/BV of 1.2 which many used as the rule of thumb to value the acquisition of a financial institution may no longer valid

2017-12-31 11:32

Btw Jon, how do we apply the rule of thumb on other banks with different leverage ratio? Using maybank as an example, I couldnt get the valuation that you got from the spreadsheet. Would you mind showing the maths behind the calculation?

2017-12-31 11:57

@thecontrarian,

i think msbs most undervalued, followed by affin.

looking to see if i might want to grab affin at 2.

2017-12-31 15:21

Salute your sharing. Gave me new perspective. You are good. Btw, for bank, bnm compulsory bank to provide 1.5% impairment to their loan right? Ok not assets , loan only. So mbsb once become bank need to comply such. So more impairment moving forward?

2017-12-31 15:48

very good article!! btw drop in value to bankruptcy for BANK A,B,C should be 9%, 20% and 1 % respectively. Can Jon kindly elaborate the math underlying the thumb rule valuation? Please write more such articles in the future :D, thanks!

2017-12-31 16:32

Refer to the formulas in the spreadsheet. The rule of thumb, does take leverage into account. But it does not take bankruptcy risk into account.

I'm guessing you're referring to KCCHONGNZ. I definitely learned a lot from him. I actually finished all his blog post. He's a great writer and has very very varied experience and knowledge of the markets. Even OTB said that his returns was rubbish until he started to learn from KCCHONGNZ.

If i were him, i would not be talking about my current picks either, especially since his subscribers are paying him money for that. It would be unfair to the people that pay him for him to share his picks here.

"Flintstones Btw Jon, how do we apply the rule of thumb on other banks with different leverage ratio? Using maybank as an example, I couldnt get the valuation that you got from the spreadsheet. Would you mind showing the maths behind the calculation?

31/12/2017 11:57"

One of the most undervalued. There is another company, that is the best and most undervalued. I kept it out of the spreadsheet.

Affin is at a 40% discount to fv using my formula now.

"TheContrarian Affin most undervalued?

31/12/2017 12:11"

You comments on the basel 3 requirements as well LCR do hold merit. However, this is only a rough guide. I'm not a bank expert. For me, when it comes to investing, i follow this saying.

"You don't need to know the weight of a woman to know if she's fat, or the age of a man to know if he's old"

As long as its within the margin of safety, i'm fairly good with it.

On liquidity. Liquidity crunches are common and a way of life for banks. The real life equivalent would be "Tripping".

In life, when you are walking or running, you will trip over something. Sometimes you will fall, sometimes, you will be able to catch yourself. Its almost never a big deal.

Tripping becomes a problem when you're running top speed on uneven ground, while carrying 100 plates stacked to the sky. An small bump, or in this case liquidity crunch, and you will be properly fucked.

Pre-crisis. The banks using synthetic CDO's (Which in itself were leveraged) were theoretically leveraged in same cases more than 100 times. And these so called liquid instruments, were build upon very illiquid assets. This means the instruments themselves were not truly liquid to begin with.

It would be a little bit premature to say that the main reason for the crisis is due to liquidity crunch. |

Its like saying, the only reason he died was because he tripped. If you tripped while walking, no biggie. If you died, when your tripped while walking on a tightrope 500 meters in the sky. Maybe the main reason you died was because you were walking on a tightrope 500 meters in the sky in the first place.

"Fabien Extraordinaire Liquidity crunch was the main reason in the last financial crisis that made some banks go bust or almost bust.

31/12/2017 11:32"

Good catch! Updated. Thanks!

"Unlevered very good article!! btw drop in value to bankruptcy for BANK A,B,C should be 9%, 20% and 1 % respectively. Can Jon kindly elaborate the math underlying the thumb rule valuation? Please write more such articles in the future :D, thanks!

31/12/2017 16:32"

2017-12-31 17:49

No, and I'll give you a hint, its got to do with your 'rule of thumb' and the assumptions youre making

2017-12-31 18:28

Good work Jon chivo, but add one point....the roe on bank is another assessment for value

2017-12-31 18:54

"One of the most undervalued. There is another company, that is the best and most undervalued. I kept it out of the spreadsheet. "

rce?haha just guessing

2017-12-31 19:25

What do you mean?

valuelurker No, and I'll give you a hint, its got to do with your 'rule of thumb' and the assumptions youre making

31/12/2017 18:28

2017-12-31 22:49

On undervaluation of a certain bank, maybe you should find out how many of your family members, friends and associates park their money, especially the portion meant for retirement, with the bank as FD. If you find that most of them, especially if you yourself don't park the money with the bank, then you may have got the answer why the market gives it low valuation.

2018-01-01 10:05

well done Jon Choivo. I enjoy reading your articles, meticulous and quantitative. Keep up the good work bro.

And I welcome your comments on my articles, good or bad, no problem

2018-01-01 10:21

Definitely, that's one way to get real down to earth information. That's why my position is very small. =)

limml On undervaluation of a certain bank, maybe you should find out how many of your family members, friends and associates park their money, especially the portion meant for retirement, with the bank as FD. If you find that most of them, especially if you yourself don't park the money with the bank, then you may have got the answer why the market gives it low valuation.

01/01/2018 10:05

2018-01-01 15:52

I am out.

Why? In essence, not a fan of the industry (cost based, increase in earnings due to higher efficiency tend to go to customers via discounts instead of to the company).

I held it as i thought the ROIC is pretty good and i like the gigantic cash balance, however, i think but the problem is that this wonderful cash balance will all be going into their expansion into the fabric mill, which while good for the company, is much better for the customers and not so good for the investors.

Whatever cost savings from the mill, will need to be given to customers in order to undercut magni etc. Its a race to the bottom.

I have better/cheaper opportunities available. I have originally wanted to sell my PRlexus at 1.2 for this similarly undervalued opportunity, except its in a far better industry.

But my ego got in the way, i wanted this to be a gain as i was sure of my research, which included all of the above.

PRLEXUS is my biggest loss in 2017.

Moving forward, i will not be buying any stocks from cost based industries with high capex, unless it is a net net (ie choobee, which i bought at 1.75 and sold at 1.9 and 2.1).

10bagger10 choivo sifu, prlexus any opinion?

02/01/2018 12:38

2018-01-02 15:24

By my metric yes.

Does not mean it cannot go higher though. Feel free to buy it if you feel there is someone, moving forward, who will be willing to pay more.

james86 mbsb already 1.17, overvalued?

03/01/2018 14:01

2018-01-03 16:51

Boys and girls listen

Did the author, in May 2017 also said that Hengyuan is was overvalued at RM 5 saying buying Hengyuan is even more risky that Bitcoin...

2018-01-05 01:28

Jon Choivo Capital is pessimistic of MBSB. The same person who caught Sapura Kencana Crest and sold off Hengyuan at RM 6. Run away from this guy like the plague.....

2018-01-05 01:33

u have to consider the potential after getting the Islamic banking license mah.

2018-01-05 12:36

Do quote what you said of me from my old post, i've never deleted anything from my history.

Orange88 Boys and girls listen

Did the author, in May 2017 also said that Hengyuan is was overvalued at RM 5 saying buying Hengyuan is even more risky that Bitcoin...

Historical price is not indicative of intrinsic value, see Sapura Kencana, it sed to be worth RM4, then RM2, now RM0.8

james86 mbsb can go higher to 3.2 since 2013

05/01/2018 11:54

Just because get license does not mean your profit go up immediately, remember what i said about banks finding it hard to increase profit a lot due to difficulty in obtaining deposits and managing cash flow.

Also, almost every bank have that license, and even better BIMB got the word "Islam" in their name. Why not that then?

latlut u have to consider the potential after getting the Islamic banking license mah.

05/01/2018 12:36

2018-01-06 00:44

"why Coldeye is wrong on MBSB"???? With recent surge of MBSB share price, then we know investment is an ART. You no need to know too deep in those banking theory behind.

2018-01-07 00:53

Definitely, looking at EKOVEST with sadness. Really wanted to buy at 90, but bolui. Than at thursday, wanted to buy the warrants at 585, but i am the conservative type one, hate paying more. Now. Haih

godhand if i may correct u. the whole bursa is bullish.

07/01/2018 01:14

It definitely is. Its not so precise that its like physics, nor is it so abstract, that its like a painting.

But the movement in price does not mean that i am wrong. Enron and Valeant reach incredibly high prices as well.

If i'm wrong, it must come from either something i overlooked or miscalculated fundamentally.

My figures on the impairment is definitely not precise and may even be wrong =) And MBSB may very well be worth RM1.35 or whatever the bulls want to put on it.

Invest_168 "why Coldeye is wrong on MBSB"???? With recent surge of MBSB share price, then we know investment is an ART. You no need to know too deep in those banking theory behind.

07/01/2018 00:53

2018-01-08 21:54

Investment is abt future, not merely based on current data. U will nvr make big analyzing available data or figures. That’s the diff btw super investor guru and normal investor.

2018-01-30 00:10

Malaysiakini on 1st August 2018, Wednesday

(co-authored by Peh Beng Kheng Foundation)

https://www.malaysiakini.com/letters/436883

Some tips on how to manage GLCs

2018-08-04 21:32

Coldeye 13.8 millions? Not 33.8millions? Aiyoh, i always say 33.8 millions to people oh.. Haha i should get this right before i comment mah. If such simple figure i also wrong, how i convince people oh... Let alone article.. Haha LOL

2018-08-05 00:19

Guys, this post is damn old.

The essence is still there. Butt the data is likely to be outdated.

Mbsb I still think it is not that cheap, but it's definitely more interesting since Dec 2017.

I am looking at it, but I'm somewhat unconvinced. The license is not the gamechanger, but another thing, which I am not sure yet.

2018-08-05 03:09

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Apps

Top Articles

1

https://dividendguy67.blogspot.com

3

4

Good Articles to Share

Could Kamala Harris beat Donald Trump in November's presidential race?

5

Good Articles to Share

Iranian warship capsizes during repairs in port of Bandar Abbas

6

Good Articles to Share

7

Good Articles to Share

Jonathan Turley unveils exciting new book 'Free Speech in the Age of Rage'

8

Good Articles to Share

Why Impossible Foods signed hot dog-eating legend Joey Chestnut #yahoofinance #youtubeshorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Flintstones

This is a good piece of fundamental value analysis article right here. So much better than some other self proclaimed sifu who keeps on chirping the same fundamental value thing while what being written is nothing more than the historical prices of his previous picks.

2017-12-31 09:26